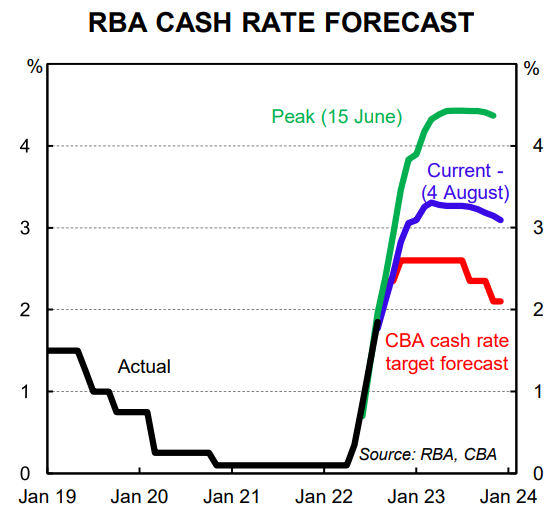

CBA’s head of Australian economics, Gareth Aird, has released a note explaining why he believes that the market’s projected official cash rate (OCR) for Australia – currently tipped to peak at 3.35% in March 2023 – remains too bullish.

Instead, Aird tips that the OCR will peak at 2.6% – a level that he considers is contractionary – before being cut by 0.5% from mid next year:

We expect the cash rate target to peak at 2.60% by the end of 2022 (a level which we consider to be contractionary)…

Financial conditions will continue to tighten over 2023 with no change in the cash rate given the big fixed rate home loan expiry schedule and we have 50bp of rate cuts in our profile for the cash rate for H2 2023…

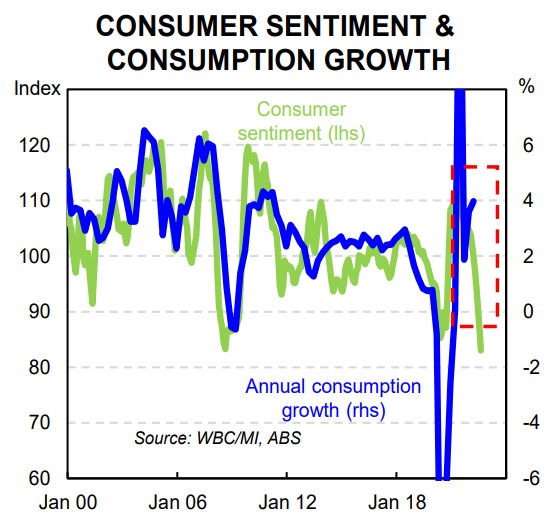

The RBA was the archetypical two handed economist [in its SoMP] with respect to the outlook for consumer spending. On the one hand they noted that, “household incomes are being sustained by strong labour demand, which is feeding into strong growth in employment and hours worked, and will ultimately lead to stronger wages growth. Also household balance sheets are in generally good shape, underpinned by a high level of savings.”

But on the other hand the RBA stated that, “high inflation and rising interest rates are raising the cost of living and will weigh on households’ spending. Household consumption could also be dampened by wealth effects as housing and other asset prices decline”.

We agree with both these statements so the RBA are not the only two-handed economists right now! However, we believe that high inflation coupled with aggressive rate hikes and falling home prices will be the more dominant force on household consumption from here. As such, we do not expect the RBA to take the cash rate above 2.6%. And it is also why our central scenario sees the RBA cut the cash rate in 2023 (we have two rate cuts pencilled in for H2 2022).

As we noted on Tuesday, there is a significant dichotomy in the domestic economic data at present and this will continue over coming months. Backward looking labour market data will remain robust, wages growth will accelerate and inflation will remain elevated. But forward looking data has deteriorated and further weakness is expected (this includes consumer sentiment, home prices, housing lending and building approvals).

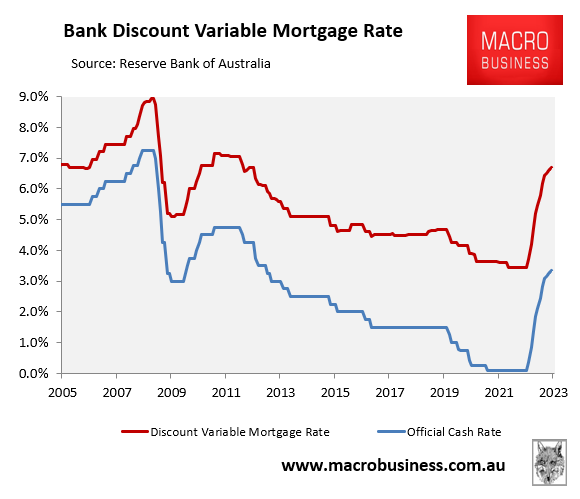

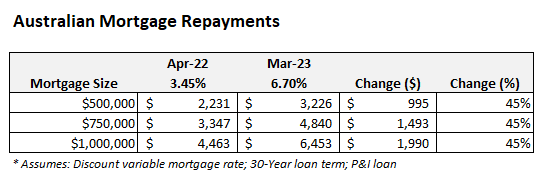

If the OCR was to rise to 3.35% by March 2023, as projected by the futures market, then Australia’s average discount variable mortgage rate would soar to 6.7% – it’s highest level since April 2012:

Advertisement

Mortgage rates to soar.

In turn, average monthly mortgage repayments would surge by 45% versus what they were in April 2022 immediately prior to the RBA’s first rate hike when the average discount variable mortgage rate was 3.45%:

Mortgage shock coming for Australia.

Advertisement

Such an sharp increase in repayments would decimate household finances, crunch consumption, hammer house prices, and risks driving the Australian economy into an unnecessary recession.

For these reasons, the CBA’s 2.6% projected peak in the RBA cash rate followed by sharp rate cuts seems far more realistic.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.