By Stephen Wu, Economist at CBA:

Key Points:

- There is a strong correlation between consumer sentiment and consumption growth.

- Recently a gap has opened up, with sentiment much weaker than spending – although a large portion can be explained by economic factors.

- But consumer sentiment is still weak – even after accounting for other economic variables – and that raises the risk that spending growth will slow more materially from here.

Overview

Consumer sentiment correlates well with consumption growth. But recently there has been a widening gap between the two measures. On one hand, we have seen consumer sentiment decline to very low levels that are consistent with major economic disruptions. But on the other hand, consumption growth was robust in Q1 22 and looks to have been fairly solid in the June quarter.

In this note we investigate the relationship between consumer sentiment and consumption. We find a statistically significant relationship between the two, and some evidence that consumer sentiment leads consumption growth. That suggests spending will ease from here and may contract.

We also turn the question around and ask why consumer sentiment is so weak. To do this we explore the key drivers of consumer sentiment. We find that a large portion of the volatility in consumer sentiment can be explained by variables like home prices, equities, inflation, wages growth and uncertainty. But consumer sentiment remains weak even after accounting for these factors. We think this suggests a downside risk to spending momentum from here.

Consumer sentiment correlates with consumption growth

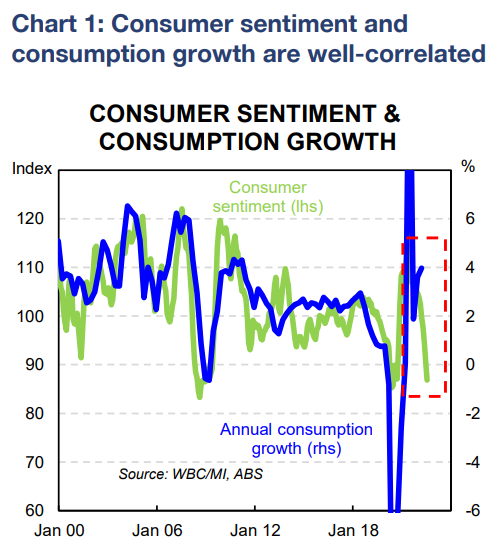

It has been well documented that there is a good positive correlation between the WBC/Melbourne Institute consumer sentiment survey and consumption growth (chart 1; consumption is volumes as measured in the national accounts and we also test discretionary and durable goods consumption too). As a result, consumer sentiment has generally been useful in gauging the strength of the consumer, especially as the national accounts measure of household consumption is released with a fairly long lag.

The headline consumer sentiment index gets the most attention by market participants and the media. However, some of the components that make up the headline index are actually better correlated to measures of consumption growth.

The ‘family finances vs a year ago’ index and the ‘current condition’ index (which is not part of the headline index but a separate derived index; see appendix for more details) is better correlated to consumption.

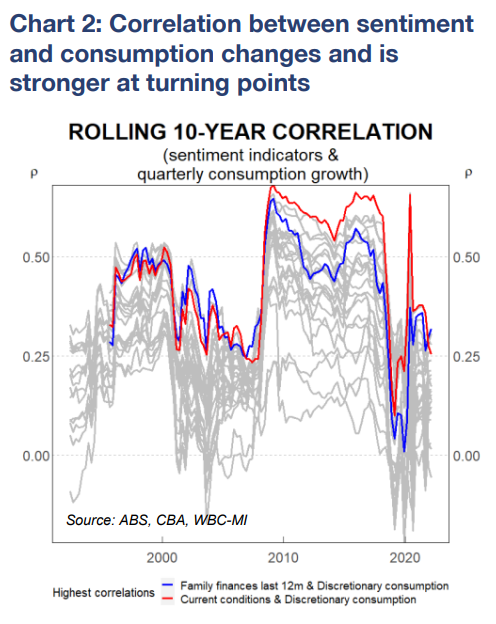

However, the correlations between consumer sentiment (and the various subindexes) and consumption growth are not steady over time. Using a rolling 10-year window shows there can be fairly large variations in the strength of the correlation (chart 2). Correlation also appears to be stronger when the economy is at a turning point, something already noted in a 2015 RBA article.

A statistically significant relationship between sentiment and spending

To more robustly test this relationship, we run regression models of quarterly consumption growth against its own lagged values, augmented by the various consumer sentiment indexes (updating a similar exercise done by the RBA).

We find that in general the sentiment indexes are statistically significant and in some cases lead actual consumption growth. That is, an increase (decrease) in sentiment in the previous quarter is associated with an increase (decrease) in consumption growth in the current quarter.

We also find that changes in the sentiment indexes are associated with larger changes in discretionary and durable goods consumption than for total consumption. The larger sensitivities make sense given the non-discretionary (or essential) portion of consumption is almost by definition less volatile.

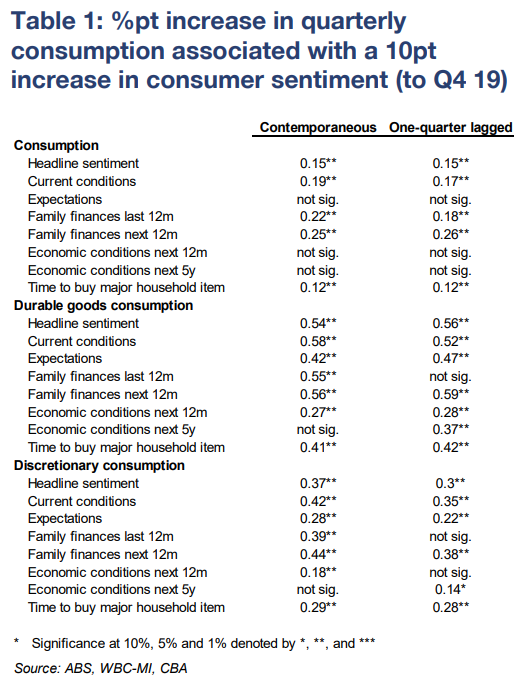

Table 1 details the coefficients and their significance.

Given that consumer sentiment has roughly declined by 10pts between Q1 22 and Q2 22, the coefficients suggest a 0.2-0.6%pt fall in quarterly consumption growth. A larger fall is likely in our view over H2 22, however, as the sensitivity between consumer sentiment and spending has increased during the pandemic.

The puzzling gap between sentiment and consumption

The puzzle at the moment is the wide and growing gap between consumption growth and consumer sentiment (as seen in chart 1). Consumer sentiment has been broadly declining since hitting its peak in April 2021, more than a year ago. There has been an almost 30% decline since those peak levels.

However, consumption growth has been resilient. Notwithstanding the Delta lockdown period of Q3 21, quarterly consumption growth has been above trend levels. And other spending indicators like retail trade have also been strong.

To investigate the cause of the perceived weakness in consumer sentiment relative to the strength in spending we model consumer sentiment as a function of other available economic variables. This tells us where consumer sentiment should be based on the other economic data released so far. We then compare this modelled estimate of consumer sentiment to the actual index.

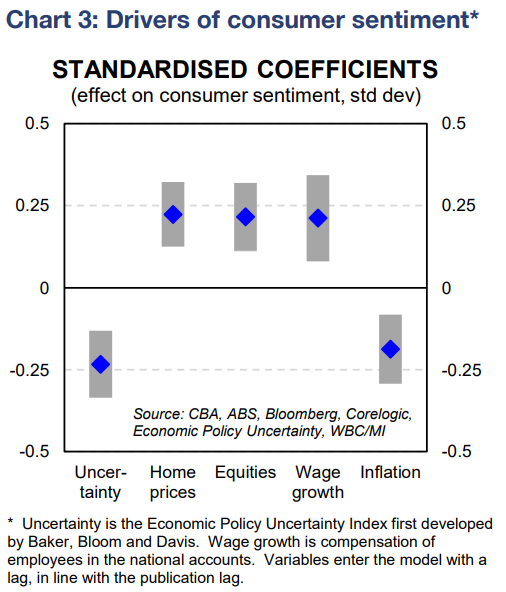

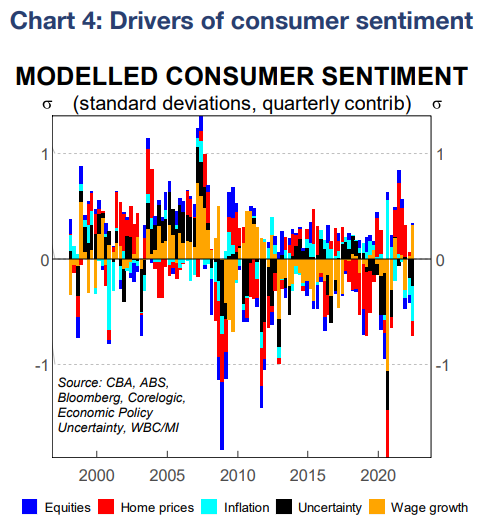

We find the key drivers are changes in home prices, equity prices, inflation, wages growth and economic uncertainty (charts 3 and 4). The signs of the coefficients are as expected: rising home and equity prices are positively associated with consumer sentiment. That is consistent with the idea of a wealth effect, where spending rises when household wealth increases. Higher wage growth is also associated with rising consumer sentiment.

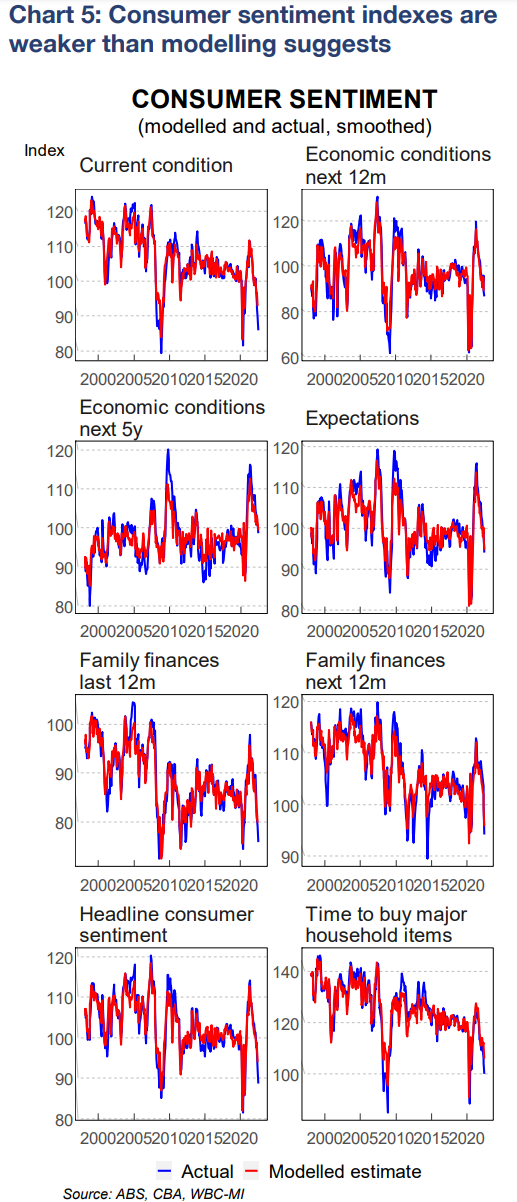

In contrast and as expected, rising uncertainty and inflation is associated with lower consumer sentiment. Other variables, such as petrol prices and labour market variables, were considered but they were generally not significant. The modelled estimates are a decent fit, and explain roughly 40% of the variation across the consumer sentiment indexes (chart 5).

Given weakness in a number of these variables in recent months, the softness in consumer sentiment is less puzzling: home price growth began easing in early 2021 and prices are now falling, with price falls having accelerated in large part because of RBA interest rate hikes; there had been a correction in equity markets since the start of the year, notwithstanding a recent lift; inflation began accelerating last year; and both domestic and global uncertainty rose sharply earlier this year.

But actual headline consumer sentiment in recent months has been weaker than implied by the models. Notably weak has been some of the other subindexes; the ‘current condition’, ‘family finances next 12 months’, and ‘time to buy a major household item’ indexes have residuals around two standard deviations below zero. In other words, modelled estimates are substantially below the actual figures.

One possibility is that there are non-linear relationships between the economic variables. Put another way, the confluence of high uncertainty and inflation as well as falling home and equity prices together could be exerting more downward pressure on consumer sentiment than the individual impacts.

Notwithstanding, even accounting for the softness in the economic data, consumer sentiment currently still remains weak. That leads to the question: is there any economic signal from the residuals, which by construction are not explained by any other economic variable?

We test this by augmenting a basic model of retail trade with these residuals. The baseline model simply uses our internal CBA credit & debit card spending data. We find that both the residuals from the ‘current condition’ index as well as the ‘time to buy a major household item’ index are statistically significant.

This means consumer sentiment provides an economic signal over and above what is captured from the other economic indicators. But some of the subindexes of consumer sentiment are better indicators than the headline figure. That suggests to us downside risks to spending momentum ahead.

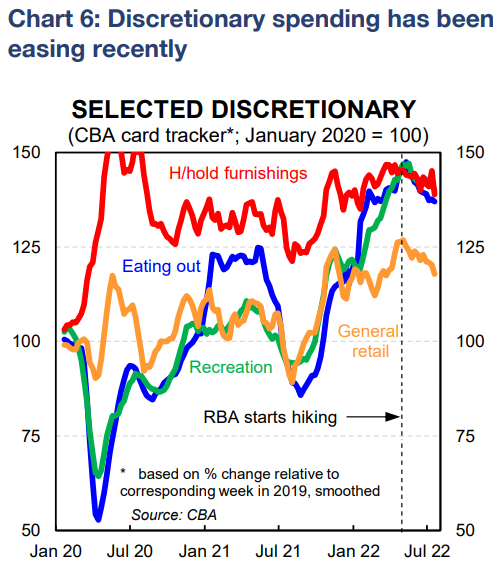

This finding is consistent with the signals from our internal CBA data, which is timelier than the official ABS statistics and covers spending through to 29 July (chart 6).

The data clearly show a moderation in spending growth. Notably, spending growth has eased most for discretionary goods and services. That is consistent with households’ budgets feeling the pinch; essential goods and services spending has held up because by definition they are harder to cut back on.

To be clear, spending is still high in level terms. Retail trade, for instance, is just under 15% higher than its pre-pandemic trend. But moderating nominal spending in an environment of rising inflation indicates that spending volumes are easing by more. We saw evidence of that in the Q2 22 retail trade volumes.

Conclusion

The monthly consumer sentiment figures are well-correlated to actual consumption growth. But some of the other subindexes within the monthly survey are a better gauge of spending in the economy than the headline index.

Consumer sentiment has declined significantly over the past year or so. Some of the weakness reflects economic developments, with home and equity prices falling and rising inflation and uncertainty. Still, consumer sentiment remains substantially weaker than what these economic indicators would suggest. And this weakness– over and above what can be explained by other economic indicators – actually contains economic signal.

We do expect the combination of materially higher mortgage rates, lower home prices, and rising cost of living pressures to put downward pressure on real consumer spending. These results suggest a real risk that spending growth could slow more materially from here. We anticipate softer spending will drive below-trend economic growth over 2023. And we expect the RBA to ease monetary policy in H2 23 (our base case has two 25bp cuts in H2 23).

Appendix: About the monthly consumer sentiment survey

The headline consumer sentiment index is a simple average of its five components. These are:

- Family finances vs last 12 months;

- Family finances next 12 months;

- Economic conditions next 12 months;

- Economic conditions next 5 years; and

- Time to buy a major household item.

Two additional indexes – the current condition index and the consumer expectations index – are constructed using these responses but are not included in the headline sentiment index.