The short squeeze party is in full swing but don’t mistake that for a bull market, says the excellent Michael Hartnett at BofA:

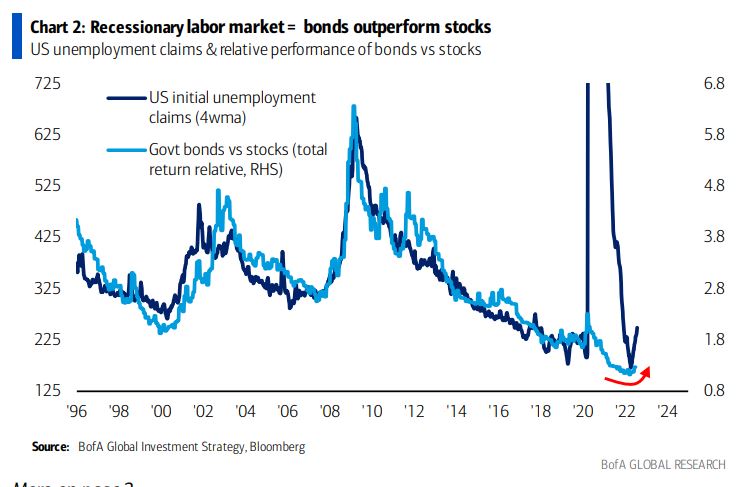

The Biggest Picture: inflation shock H2’21…rates shock H1’22…recession shock H2’22; once labor market turns recessionary (claims are up) bonds outperform stocks (Chart 2).

Tale of the Tape: Aug 4th 2020 marked lowest 10-year US Treasury yield (0.5%) in history of republic; past 2 years yield jumped 300bps to peak at 3.5% June 14th; regime change in 2020s = higher inflation, higher yields, lower returns, but “recession shock” has allowed 10-year yield to drop to 2.7% (Chart 3) = oxygen for bear market rally.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.