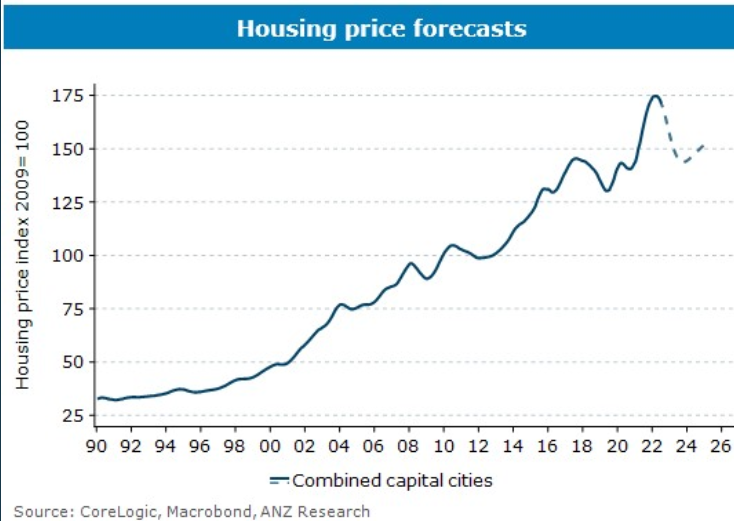

ANZ Bank has released a revised outlook for the residential property market, forecasting that house prices in the nation’s capital cities will fall by 8% by the end of 2022 and by 18% between now and the end of 2023.

Felicity Emmett from the ANZ Bank says the prospect of further interest rates hikes in coming months will weigh on the housing market. The bank expects the official cash rate (OCR) to be 3.35% at the end of the year, which equates to variable mortgage rate above 6%.

ANZ tips sharp house price correction.

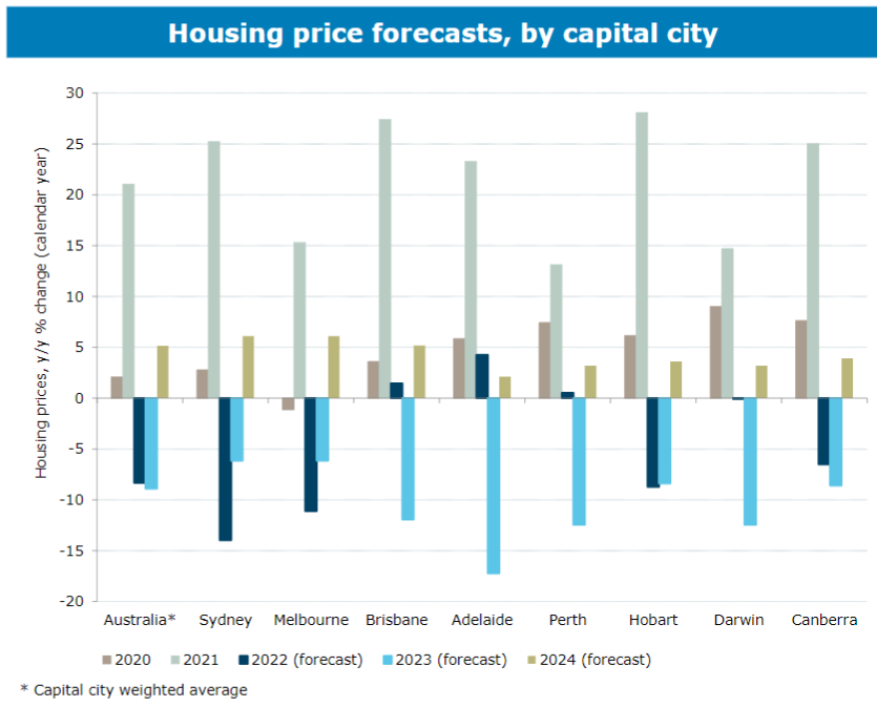

Accordingly, dwelling prices in Sydney are forecast to fall by 14% in 2022, and an additional 6% in 2023, while prices in Melbourne are tipped to dive 11% per cent in 2022 and 6% per cent in 2023:

Advertisement

Sydney and Melbourne to lead house price falls.

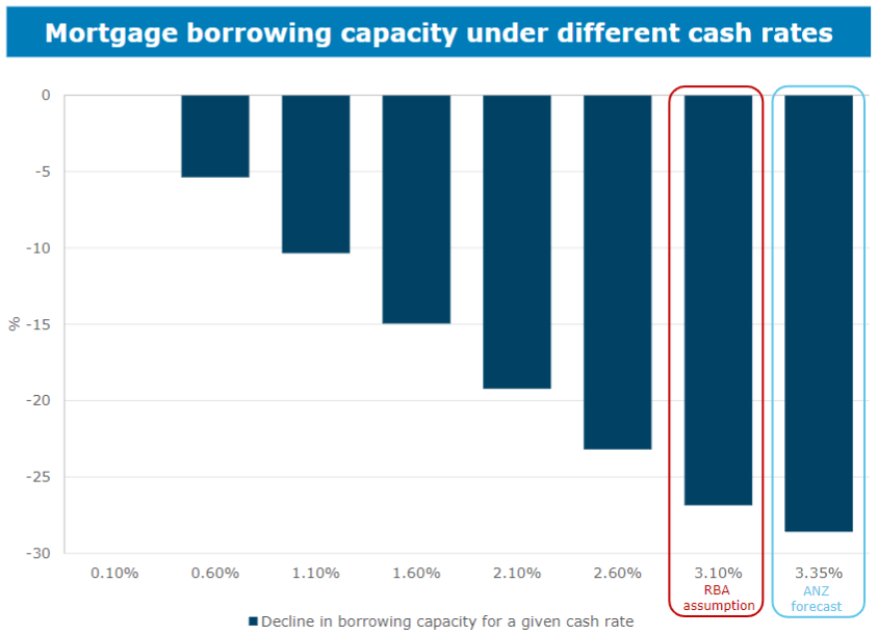

The reduced borrowing capacity from the Reserve Bank of Australia’s (RBA) aggressive interest rate hikes is the key driver of the projected sharp decline in house prices. As illustrated in the next chart, borrowing capacity will be reduced by nearly 30% if the RBA lifts the OCR to 3.35%:

“The biggest factor driving prices lower is reduced borrowing capacity”.

“Our forecast for the cash rate to reach 3.35 per cent equates to a reduction in borrowing capacity of nearly 30 per cent”.

“This reduced ability to pay up will drive prices lower over coming months. Already housing finance data show that average new mortgage sizes are beginning to fall.”

Advertisement

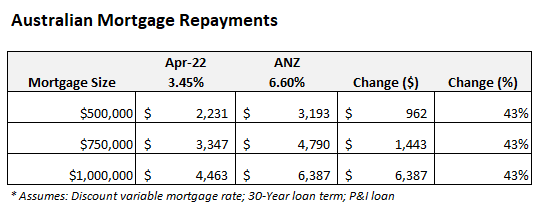

The reduced borrowing capacity can also be illustrated using a mortgage calculator.

Before the RBA began its monetary tightening cycle in early May, Australia’s OCR was just 0.1% and the average discount variable mortgage rate was 3.45%.

If the ANZ’s 3.25% OCR forecast comes to fruition, it would see the average discount variable mortgage rate climb to 6.60%, assuming increases in the OCR are fully passed on.

Advertisement

This implies a 43% increase in average mortgage repayments versus their level in April before the first rate rise:

Borrowing capacity falls as interest rates rise.

The above data shows why mortgage rates are the biggest short-term driver of house prices, and why the RBA’s aggressive monetary tightening will necessarily drive house prices sharply lower.

Advertisement

Increases in interest rates raise the cost of debt, lower borrowing capacity and, therefore, stymie buyer demand. No other factor comes close in driving house price growth.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.