US homebuilder confidence (NAHB) fell to 49 (est. 54, prior 55) – the lowest since May 2020. The report noted builder confidence continues to be affected by the FOMC’s rate hikes and persistently higher building costs.

The NY Fed manufacturing survey plunged to -31.3 (est. +5.0, prior +11.1) – the second largest fall in history (since 2001), and is the fifth weakest reading of all time. There were declines in every component apart from prices received, with the largest fall in new orders and shipments. The prices paid component is down from the record peak in April, while prices nudged higher.

Event Outlook

Aust: The RBA’s August meeting minutes will provide colour around the third consecutive 50bp hike and risks to the outlook. Overseas arrivals and departures should continue to forge ahead in July.

Eur/UK: The ZEW survey of expectations should continue to reflect the weakness in European confidence in August. The European trade deficit is also set to remain wide in June given the strength of energy-related goods imports (market f/c: -€22bn). Meanwhile, the UK’s ILO unemployment rate is expected to remain at its pre-pandemic level in June (market f/c: 3.8%).

US: A decline in housing starts and building permits is anticipated in July as tightening financial conditions weigh on demand and input constraints limit supply capabilities (market f/c: -1.9% and -2.7% respectively). Supply issues remain an ongoing headwind to industrial production in July (market f/c: 0.3%).

What matters is covered by JPM:

Advertisement

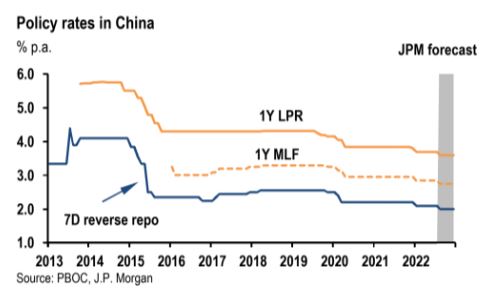

China: The PBOC surprisingly cut MLF rate by10bpStay long 5y CGBs as PBoC’s over-delivery opens up downside in rates; Stay bearish CNY on reinforced cyclical pessimism

The PBOC cut its policy rate (1-year MLF interest rate) by 10bp to 2.75%. The rate cut is a surprise move for the market (consensus: unchanged), and the last rate cut happened in January from 2.95% to 2.85%. Meanwhile,the amount of MLF operation is 400 billion yuan (in line with market expectations), implying a net liquidity withdrawal of 200 billion yuan this month (with 600 billion MLF expired).

We have argued that it is desirable for the PBOC to cut policy rates, against the backdrop of below-trend growth, weak labor market condition and low core CPI inflation. Nonetheless, the concerns about rising headline CPI inflation (to 2.7%oya in July and will most likely exceed 3% in the next few months), acceleratedpace of rate hikes by most other central banks and capital outflow pressure have made the PBOC reluctant to cutpolicy rate. Indeed, the PBOC Monetary Policy Operations Report released last week did not hint on policy rate reduction.

A likely trigger for the unexpected policy move is weak credit report in July(released last Friday), with TSFgrowth edging down to 10.7%oya.Also, July activity data released today is broadly weaker than expected, with IP increasing 3.8%oya (consensus: 4.3%), retail sales rising 2.7%oya (consensus: 4.9%) and FAI growing5.7%oya ytd (consensus: 6.2%). These jointly point at soft domestic demand.

How effective is the policy rate reduction? It is a desirable move, but the policy impact will depend on whether the government is able to mitigate the uncertainty associated with zero-COVID policy and Omicron outlook (a predominant factor behind weak incentive for investment and consumption), whether prompt actions can be taken to address the housing market weakness and an anticipated fiscal funding gap into 4Q. To that extent,monetary policy is an important component, but perhaps of secondary importance in the current environment.

Readers will know I was expecting more PBOC easing but not so soon after the COVID reopening. China is in very poor shape and this will next to nothing to improve it. Expect much MOAR.

JPM is right to expect CNY weakness but this will not end well for global markets which hate it as it drives up DXY, sinks the EUR, and delivers a double-shock to EM current accounts.

In short, the AUD rally just topped out and most everything else will probably follow in due course.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.