DXY is back and it’s bad. EUR is sick:

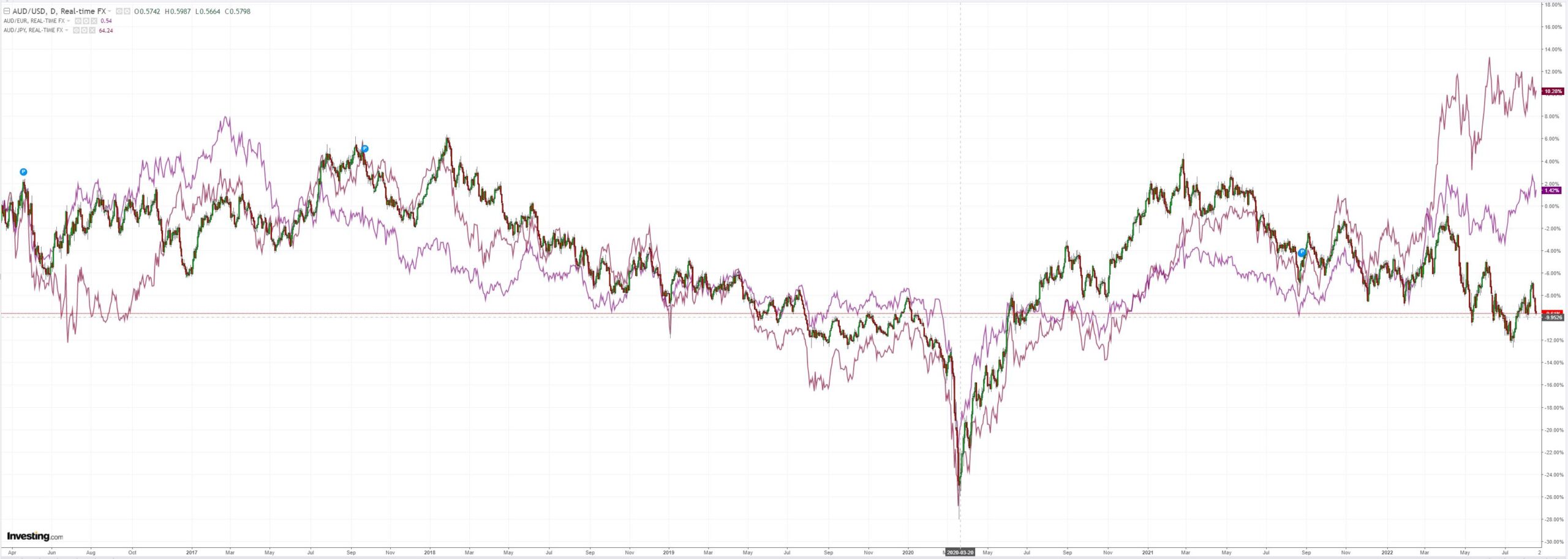

AUD is too:

Oil bounced:

But metals are rolling:

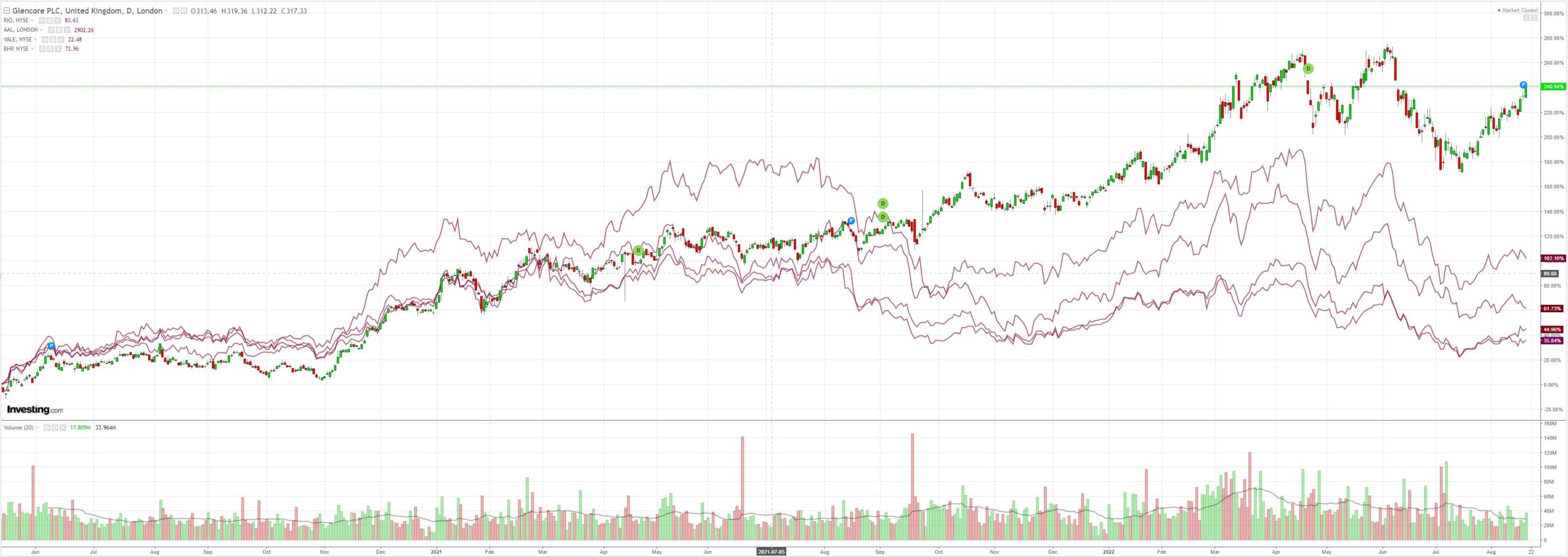

As miners smoke crack:

EM stocks look toppy:

Junk has rolled as well:

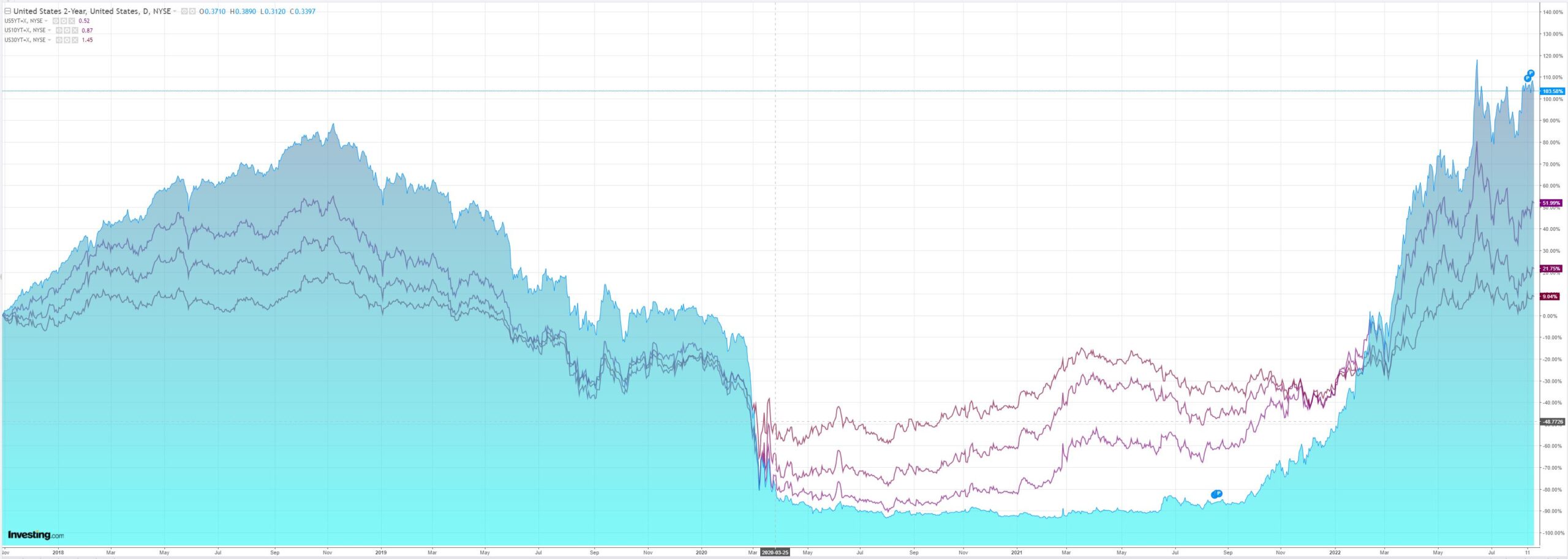

The US curve steepened a touch:

Stocks only go up:

Westpac has the wrap:

Event Wrap

US existing home sales in July fell for a sixth consecutive month to 4.81m (est. 4.85m, prior 5.11m). The Leading Index in July fell 0.4%m/m (est. -0.5%m/m, prior revised to -0.7%m/m from -0.8%m/m). Weekly initial jobless claims and continuous claims were lower, suggesting that weakness has yet to appear in the labour market. Initial claims of 250k beat estimates of 264k, with continuing claims of 1.437m (est. 1.455m).

The Philadelphia Fed business survey rebounded to 6.2 (prior -12.3, est. -5). Although the survey cited steady activity, the majority of indicators improved and price indicators eased from elevated levels. Employment rose to 24.1 from 19.4, new orders -5.1 from -24.9, prices pad to 43.6 from 52.2, and prices received to 23.3 from 30.3. The future expectations index rose from -18.6 to -10.6.

FOMC member Bullard said he is leaning toward another 75bp increase, and a year-end rate of 3.75% to 4%. He added that it is premature to start thinking about easings. George said she has yet to determine the size of a hike. Kashkari said the Fed still has a long way to go, and is not sure the FOMC can avoid pushing the economy into recession. Daly maintained the Fed’s mantra of maintaining rates at higher levels next year (“raise and hold strategy”), but remains open on a 50bp or 75bp hike in September. She advocates a rate of “a little bit above 3.0% this year and a little bit more above 3% next year”.

Eurozone CPI in July was in line with the initial release of +0.1%m/m and 8.9%y/y and a core rate of 4.0%y/y.

Norway’s central bank raised its policy rate 50bp to 1.75%, as widely expected, accompanied by a hawkish statement. It signalled further hikes, as it fights persistently high inflation, needing to dampen the economy to bring inflation back towards target.

Event Outlook

NZ: The trade deficit is expected to widen in July given the seasonal slowdown in agricultural exports and still elevated oil prices (Westpac f/c: -$1250mn).

Japan: Ongoing weakness in underlying consumer price pressures is anticipated in July (market f/c: 2.6%yr).

UK: Inflation and pessimism around the growth outlook will continue to weigh heavily on GfK consumer sentiment in August (market f/c: -42). Ongoing pressure on households’ spending capacity should result in another negative print for July’s retail sales (market f/c: -0.2%).

The Fed is much more hawkish than the market which renews the DXY bid and creates it own ends:

- commodities will fall;

- EM assets will fall;

- junk bonds will fall, and, eventually,

- equities will fall.

Such a steep DXY climb is also sending the distinct message that tail risks are not done with.

AUD down.