Veteran bank analyst Jon Mott warns a $250 billion wave of mortgage delinquencies could sweep Australia if ANZ’s, Westpac’s and the financial market’s 3% official cash rate (OCR) forecasts come true.

Mott notes that the build-up in mortgage debt over the prior two years “is the second-biggest jump seen since lending data was first captured during the 1970s, and only beaten by the 131.5% rise in the lead-up to the 1988-89 housing downturn”.

And it is this cohort of borrowers that have overextended themselves and risk defaulting on their mortgages:

While he concedes the analysis is rough, he estimates that, in total, borrowers who have somewhere between $200 billion and $250 billion in mortgages will face severe stress if the cash rate hits 3 per cent later this year, as expected.

“If interest rates continue to rise sharply, and stay around these levels, there will be a ‘fat tail’ of borrowers who will simply not be able to afford to meet their repayments,” Mott says.

“For the first time in several decades, we are likely to see a wave of fully employed borrowers falling into delinquency as they simply can’t make ends meet.”

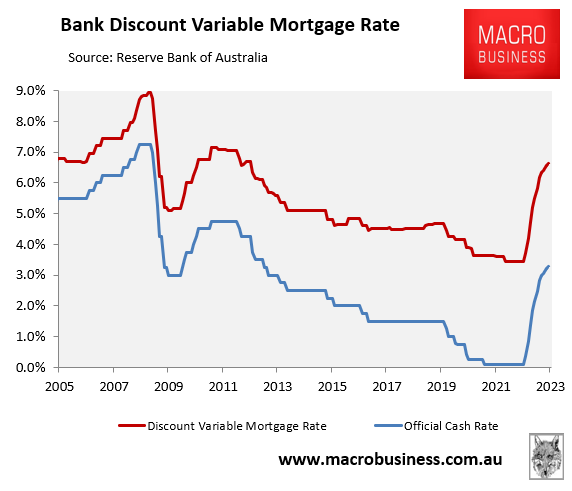

Mott’s analysis might seem alarmist. However, the latest ANZ, Westpac and futures market forecasts tip the OCR will peak at around 3.25% early next year, which would take the average discount variable mortgage rate to 6.60%, up from 3.45% in April before the RBA commenced its tightening cycle:

Mortgage rates to rise to 2012 levels.

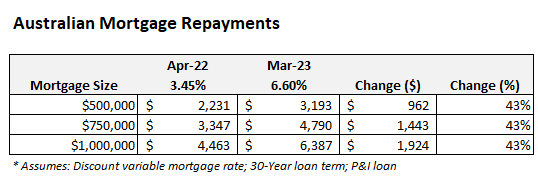

This would represent the highest mortgage rate since 2012. It would also lift principal and interest mortgage repayments by 43% against their level in April:

In dollar terms, a household with a $500,000 mortgage would see their monthly repayments rise by $962, whereas a household with a $1 million mortgage would see their monthly repayments soar by $1,924.

This presents a poison pill for households that borrowed to the max over the pandemic at ultra low rates to get into the market. These borrowers would face extreme financial strain at the same time as their house values collapse, especially across Sydney and Melbourne.

Many would be thrown into negative equity and some would default.

Ultimately, the ball is in the RBA’s court. Will it continue hiking aggressively, as tipped by ANZ, Westpac and the financial markets? Or will it follows CBA’s projection, stop-out early and then cut?

Only time will tell.