In my ten years of observing the hideous Australian macro sausage factory in action on this blog, I have never seen a more stupid and harmful series of policy blunders than what we have today on both the monetary and fiscal sides of the equation. The two are gutting Australian living standards when they should be skyrocketing from unprecedented commodity windfalls. Worse, households are wearing the vast majority of the pain inequitably as vested interests make out like bandits.

On the one side, we have the Lunatic RBA chasing wage inflation that does not exist, owing to the same serial blunders it made in the last cycle. CBA:

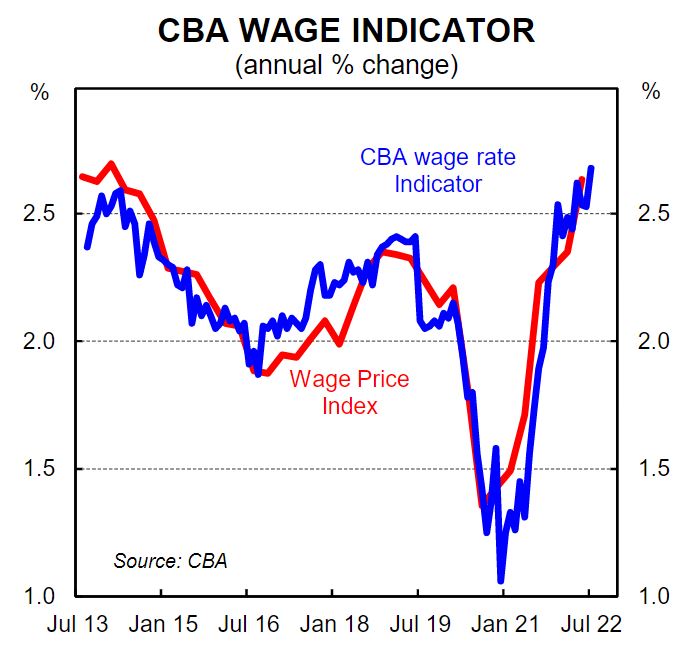

The 0.7%/qtr increase in the WPI over Q2 22 was a touch lower than our pick and the consensus call of 0.8% today (we flagged the risk was 0.7% and not 0.9% -see here). The annual rate stepped up from 2.4% in Q1 22 to 2.6%. The annual pace of wages growth is very modest considering the tightness in the labour market.

Despite the slight miss, the print today was broadly in line with our internal data which very accurately maps the WPI. It indicates wages pressures in the economy have taken time to emerge. Indeed our data more accurately captures what is happening in the economy than business surveys and business liaison as it is measures actual dollars paid into a matched sample of ~275k CBA bank accounts (see facing chart, latest data to July).

We are able to track wages inflation because we apply a strict criteria to the accounts we include in our sample each month to account for people moving jobs, receiving a bonus or modifying hours worked in any material sense. We also take into account changes in tax rates or levies. The upshot is that whilst wages growth across the economy is moving higher and some people are receiving large pay rises, there has not been broad-based wages pressures. Indeed real wages growth (as measures by headline inflation deflated by the wage price index) is deeply negative.

As we have stated previously, the RBA is not facing a wage-price spiral like is being observed in some other jurisdictions. Put another way, the RBA does not have to run hard against wages growth by aggressively hiking the cash rate. However, the RBA hasbeen tightening at an incredible pace despite the official wages data, and our own, indicatingwe simply do not have strong broad-based wages growth.

As the RBA keeps tightening it is going to snuff out the 3.5% wage growth that it needs to sustain inflation over the cycle. Its business liaison is gaming it.

Advertisement

More to the point, the RBA will stop households from catching up to the astonishing theft of income being endorsed by the fiscal side. Albo is about to drop a nuclear bomb on wages growth by speedily processing half a million temporary visa slaves and restoring mass immigration to its highest ever level.

Just as bad, Albo is still doing nothing about the paralytic energy shock that it can stop with the stroke of a pen by installing gas and coal domestic reservation, without which we will see an additional 6% inflation over the next year.

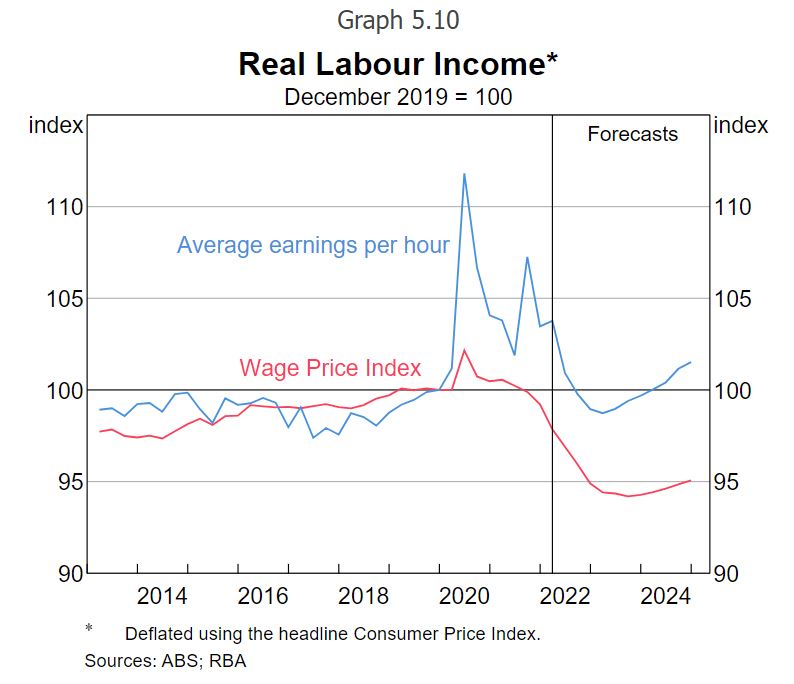

The combined impact of these fiscal and monetary blunders is to obliterate Australian real incomes at an astounding pace:

Advertisement

The data is not available so I can’t be sure but it appears this will be the largest single period of falling living standards since the Great Depression. When we add indebtedness, mortgage repayments, and crashing wealth, the step lower in living standards is almost certainly worse than the 1980s:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.