Finally, after ten years of making the problem worse, the ACCC has been fully macrobated on the gas cartel:

- it is a gas cartel that threatens national energy security

- it makes money at $5Gj

- the local shortfall will get much worse

- it is destroying manufacturing and driving a power shock

- we need much stronger domestic reservation that should apply to all gas exporters

- the domestic economy is the priority over export customers

That the cartel has been forming joint-marketing ventures for local sales is so astonishingly greedy and arrogant that it is surely a case study in monopoly overreach. There is a great PhD thesis in this describing the universal forces at work in the rise and fall of monopoly power.

Amusingly, said blood-sucking cartel has already loosened its grip in the past week with the local gas price halving to $19Gj in Victoria today even as the global price has skyrocketed.

That probably tells us all we need to know. Australia is about to cut the gas Gordian Knot. Over the you Chicken Chalmers!

Here is yours truly keeping the heat on at both the ABC News and Sky News over the weekend.

This is the July 2022 interim report of the Australian Competition and Consumer Commission’s (ACCC’s) inquiry into gas supply in Australia (the Inquiry).

This report sets out our usual reporting on the supply outlook, the domestic price outlook, commercial & industrial (C&I) user experience, transportation and storage, as well as Stage 2 of our in depth examination of upstream competition and the timeliness of supply.

This report also addresses the Treasurer’s request in his letter of 6 June 2022, in which he asked us to ensure the factors influencing prices in gas markets (domestic and export) are made fully transparent and to bring to the Government’s attention any need for regulatory change to ensure electricity and gas markets function properly for the benefit of all Australians.

Australia is a country with relatively abundant gas resources. Gas produced in the east coast is supplied to both domestic users in the east coast gas market – C&I users, gas powered generators (who also retail gas), and retail and small business customers – and overseas buyers in Asia through sales of LNG.

Much of the gas produced in the east coast is produced by the LNG exporters. On an aggregate basis, the LNG exporters and their associates had influence over close to 90% of the 2P reserves in the east coast in 2021, through a combination of their direct interests in 2P reserves, joint venture and exclusivity arrangements. This may increase the risk of coordinated conduct and increase the market power of the LNG exporters.

As part of our regular 6 monthly reporting in the Gas Inquiry 2017-2025, we report on the expected supply-demand balance for the following year, using the Australian Energy Market Operator’s (AEMO’s) demand estimates from its Gas Statement of Opportunities, issued in March each year.

For our supply side reporting, we use compulsory information gathering powers under Part VIIA of the Competition and Consumer Act 2010 (CCA) to collect information from domestic gas producers, LNG exporters and gas retailers/generators.

We collected information from these market participants up to mid-February 2022 on their forecast gas production and sales and price offers for 2023. Gas production and sales volumes estimates were also confirmed and updated with gas producers and retailers in May 2022.

We spoke to C&I users between March and June 2022 about their experiences seeking gas supply for 2023, as well as current pricing in the domestic spot markets in May/June 2022. C&I users have expressed great concern about the impact of recent price rises, if they continue. Some users noted closure of operations was becoming a very real possibility in the short term and more significant demand destruction was likely over the longer term. In June 2022, Advance Bricks announced it was closing its manufacturing operations employing over 20 people due to gas price rises and Australian Textile company Flickers is also reported to be facing closure.

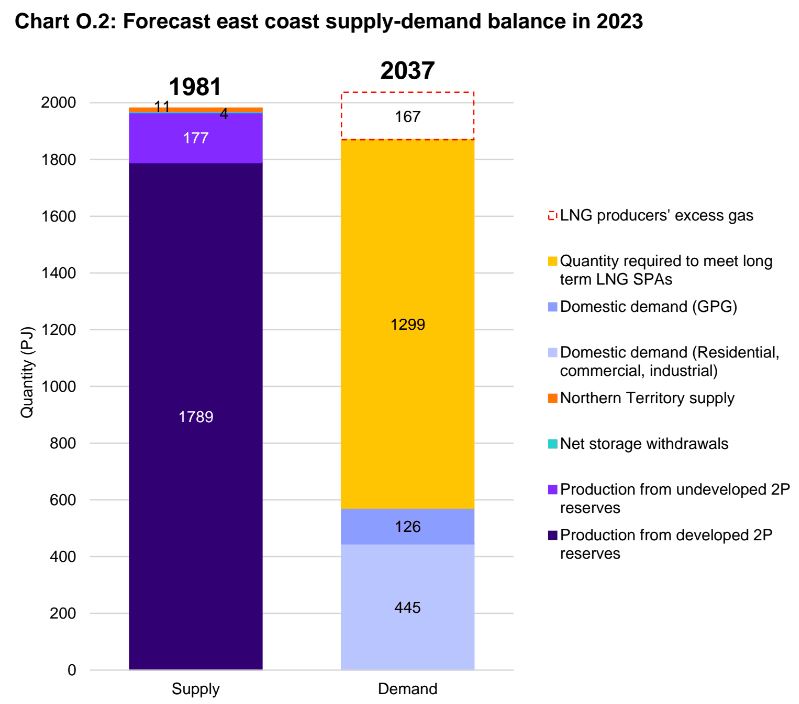

As shown in chart O.2 below, the east coast of Australia is forecast to produce 1981 PJ of natural gas in 2023. Much of this gas will be exported to overseas markets in Asia under long term contracts. In 2023, 1299 PJ of gas is forecast to be exported under long term contracts with overseas buyers (Sale and Purchase Agreements, SPAs). The remaining ‘excess’ gas2 LNG exporters in Queensland expect to produce, above their contractually committed volumes, can be supplied either to the domestic market or to overseas markets. Since 2018, we have observed that LNG exporters have exported at least half – and more frequently, around 70% – of their excess gas to overseas spot markets.

The domestic east coast gas market uses a relatively small proportion of the total east coast gas production each year. For 2023, AEMO forecasts that domestic east coast gas demand will be around 571 PJ, requiring approximately 29% of all the gas expected to be produced for the year.

However, if all the excess gas of LNG exporters is sold in overseas markets then the domestic east coast gas market is likely to be 56 PJ short of gas needed to meet forecast demand for 2023. This is a worse situation than that which occurred in 2017, when both the ACCC and AEMO predicted a shortfall of gas for the following year, and which led to the Australian Government at that time:

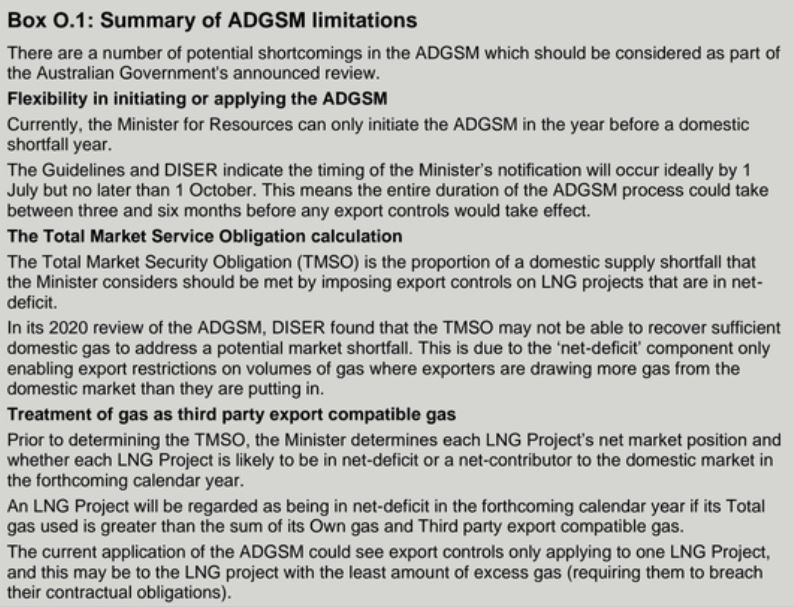

• commencing the Australian Domestic Gas Security Mechanism (ADGSM) process for determining whether 2018 would be a shortfall year

• ultimately entering into a Heads of Agreement (HoA) with LNG exporters, under which LNG exporters agreed to make excess gas available to the domestic market prior to exporting it.

The ADGSM is an export control mechanism, which allows the Minister for Resources to determine if the following calendar year is likely to be a shortfall year in the domestic market and, if it is, apply export controls on the LNG exporters to limit the amount of gas they can export as LNG.

The HoA has been replaced twice since 2017. A well-functioning HoA should ensure that LNG exporters make gas broadly and transparently available to all domestic C&I users (and gas retailers) at demonstrably competitive prices, in volumes and for periods suitable to buyers’ needs, and with sufficient notice.

In its current form, LNG exporters have committed to offer uncontracted gas to the domestic market on ‘competitive market terms’ and ‘with reasonable notice’ before offering it to the international market, and to have regard to prices they could reasonably expect to receive for uncontracted gas in overseas markets and domestic spot markets.

Since 2017 and following the signing of the first HoA, there has largely been sufficient gas forecast to be supplied into the east coast gas market to avoid a shortfall. However, our estimates have forecast an increasingly tight supply outlook and we have observed that LNG exporters have:

• exported the majority of their excess gas into LNG spot markets overseas

• forecast to withdraw increasing amounts of gas out of the domestic market since 2021 (having previously supplied more gas into the market than they withdrew through gas supply contracts with domestic producers).

In the current environment of high international energy prices (including gas and LNG), tight LNG markets, broader supply chain problems, geopolitical instability, inflation and uncertain demand for GPG domestically, we support the Australian Government placing greater focus on energy security.

Both the HoA and the ADGSM are due to expire on 1 January 2023.

Given this, the current domestic and international energy environment and the forecast supply outlook we support the recent announcement by the Minister for Resources that the Australian Government will renegotiate the HoA and renew the ADGSM beyond 1 January 2023. We consider that the ongoing operation of these arrangements will be needed to ensure sufficient gas is supplied into the domestic market to meet demand.

We also recommend that the Australian Government strengthen both arrangements and welcome the Minister for Resources’ announcement that the Australian Government will also review the ADGSM. Additionally, The ACCC welcomes the Minister’s recent announcement to extend the ADGSM to 2030.3

A summary of some of the key limitations in the current ADGSM are set out in box O.1 below.

As already noted, supply conditions in the east coast market are expected to deteriorate significantly in 2023, with a shortfall of 56 PJ now expected. This is equivalent to around 10% of domestic demand and is the largest projected supply shortfall we have forecast since the Inquiry commenced in 2017. LNG exporters are expected to contribute to the shortfall in 2023 by withdrawing 58 PJ more gas from the domestic market than they expect to supply Gas Inquiry 2017–2025 9 into the market. They also expect to export the vast majority of their 167 PJ of ‘excess gas’. In total, the LNG exporters expect to export 1,441 PJ of gas in 2023, which is significantly more than what they have exported in previous years.

Our supply outlook also shows it is highly likely that a significant proportion of the LNG exporters’ excess gas will be needed in the domestic market to avoid a shortfall. As an immediate measure, we therefore recommend that the Minister initiate the first step of the ADGSM process, to:

• formally determine whether 2023 will be a shortfall year

• work with LNG exporters to supply more gas into the domestic market in 2023 over the latter half of 2022, so that the domestic market doesn’t commence the 2023 supply year facing a material shortfall in supply.

We also strongly encourage LNG exporters to act immediately to increase their supply into the east coast gas market.

There is a significant risk to the east coast’s energy security in 2023 with a projected shortfall in supply of 56 PJ

The east coast gas market is facing a 56 PJ shortfall in supply in 2023, signifying a substantial risk to Australia’s energy security. This shortfall is a significant deterioration in conditions relative to the 2022 forecast and suggests a bleaker outlook for 2023 than AEMO projected in its latest Gas Statement of Opportunities (GSOO). This could place further upward pressure on prices and result in some manufacturers closing their businesses, and some market exit has already occurred.

The supply shortfall in 2023 is 54PJ higher than the shortfall projected at the same time last year for 2022. This is primarily due to a 52 PJ increase in forecast demand by GPG and a 24 PJ increase in LNG exporters’ export forecasts, which are offset partially by a 23 PJ reduction in forecast demand by residential and C&I users (predominantly relating to C&I users). The effects of these changes are concentrated in the southern states (NSW, Victoria, South Australia, Tasmania and the Australian Capital Territory) where gas resources have been diminishing for some time and where the majority of C&I users are located, with a 54 PJ shortfall is forecast.

In Queensland, where the LNG exporters and their production and export facilities are located, and where the majority of future reserves and resources are, a 2 PJ shortfall is expected.

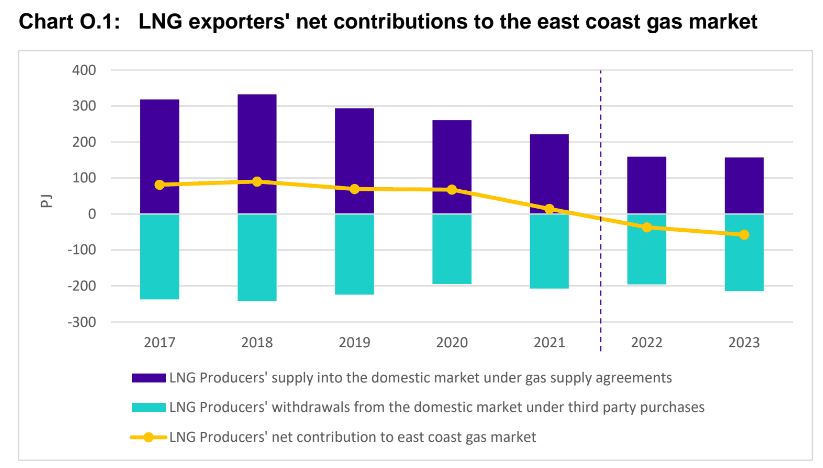

The LNG exporters are expected to contribute to the supply shortfall in 2023 by withdrawing 58 PJ more gas from the domestic market than they expect to supply into it. As shown in chart O.1, domestic third party purchases (from other gas producers who supply into the domestic market) will increase to 214 PJ while sales to the domestic market are expected to fall to half the volume actually supplied in 2017.5

Between 12 August 2021 and 16 February 2022 LNG exporters sold 24 additional spot cargoes for a total of 88.8 PJ. In this time, they contracted to supply the domestic market 27.5 PJ on a short term basis, however 12.3 PJ of this was contracted to other LNG exporters. Over this period, LNG exporters did not contract any gas for domestic supply with a term length of 1 year or greater.

The forecast 56 PJ shortfall shown in chart O.2 below is likely to result if LNG exporters decide to export all the gas that they expect to have in excess of their contractual commitments (167 PJ) as they did in 2021. This would be a 65% increase in forecast spot sales relative to 2022.

To address the projected shortfall in 2023 significant additional volumes of gas will need to be:

• produced in the east coast from gas fields that are already connected to the market • produced in the Northern Territory and transported via the Northern Gas Pipeline (NGP) into the east coast

• withdrawn from storage and/or

• diverted by LNG exporters into the domestic market.

However, these possible means of addressing the shortfalls are in large part dependent on the decisions of the LNG exporters and all but the last measure are likely to have only a small impact on the forecast shortfall.

It is very likely that to avoid the forecast shortfall in the east coast gas market in 2023, LNG producers will need to divert a significant proportion of their excess gas into the domestic market. This has led us to recommend that the Minister for Resources initiate the first step of the ADGSM process, and also strongly encourage LNG exporters to act immediately to increase their supply into the east coast gas market.

Users are receiving offers at higher prices with less flexibility

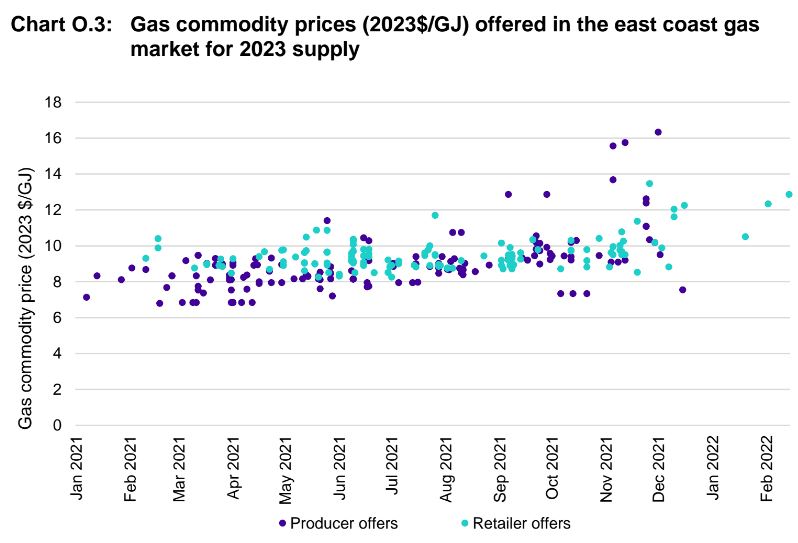

Prices offered for supply in 2023 increased over the course of 2021, accelerating from around August 2021, as shown in chart O.3. Prices offered around $16/GJ, made between November and December 2021, are the highest we have observed since early 2017.

Weighted average prices offered by producers for 2023 supply have climbed above $10/GJ, and for the first time quantity weighted average producer prices have exceeded those offered by retailers.

Global gas and oil prices increased sharply in the second half of 2021 and prices offered by producers for supply in Queensland largely tracked this increase.

Prices offered to users in southern states also increased in the latter part of 2021 but were lower than Queensland prices.

The average price payable for 2023 supply in recent Gas Supply Agreements (GSAs) in the southern states is expected to be $9.25/GJ for supply by producers, and $10.01/GJ for supply by retailers. The average price under GSAs with producers in Queensland is expected to be $7.37/GJ.

Users reported LNG exporters were making price offers linked to the ACCC’s export parity price series (the LNG netback price series) for the first time and expressed concern that this had only occurred once LNG netback prices were high. Many users were reluctant to sign up to these prices, due to the inherent uncertainty they saw in these price mechanisms.

We are very concerned at reports of even higher prices being offered to C&I users in April and May 2022, with reports of gas price offers as high as $21.20/GJ. We are also concerned with the extremely high prices observed in domestic spot markets since May 2022 (Section 2.2), along with high LNG prices, which may flow through to long term contract prices.

While in previous years some users engaged directly with domestic spot markets to help secure their gas needs and pay lower prices, they have been exposed to significantly higher prices since our last report. They are also now facing increasingly volatile domestic spot markets. Managing spot market trades and acquiring the necessary pipeline transportation services, as well as effectively hedging price risks, can be particularly difficult for smaller firms.

Similarly, spot market volatility can also impact customers of some retailers, as can be seen by the recent market suspension of Weston Energy by the Australian Energy Market Operator, which supplied gas obtained via spot markets.

Concerns about supplier behaviour reported in the January 2022 interim report have intensified. Users report suppliers are unwilling to negotiate offers and are offering reduced flexibility in non-price terms.

A well-functioning HoA with LNG exporters could ensure that LNG exporters make gas broadly and transparently available to all domestic C&I users (and gas retailers) at demonstrably competitive prices, in volumes and for periods suitable to buyers’ needs, and with sufficient notice.

While further improvements have been made by LNG exporters in demonstrating compliance with the HoA, we remain concerned that some LNG exporters are not engaging with the domestic market in the spirit in which the HoA was signed. Even if some behaviour might be argued to be technically compliant, there remain instances where some suppliers are not engaging with the domestic market in ways that are likely to result in supply agreements being reached and market conditions improving. In particular, we are concerned:

• with instances of LNG exporters not providing counteroffers to parties that bid into EOIs

• that reasonable notice does not appear to always be provided to domestic market participants

• that an LNG exporter is offering gas to the domestic market at prices it cannot reasonably expect to receive when selling uncontracted gas to the international market.

There remains significant scope for LNG exporters to learn from ACCC concerns about the behaviour of other LNG exporters, based on our examination of material provided to us to demonstrate HoA compliance. We will provide a summary of all our findings on compliance directly to each LNG exporter to provide further guidance and encourage improved HoA compliance.

Transport and storage costs will become increasingly relevant to many gas users

The forecast 54 PJ shortfall for southern states in 2023 means the net amount of gas transported south will likely need to increase over the course of the year. There is currently sufficient capacity on the relevant facilities to enable this.

Over the longer term, changes in the location of gas supply and demand centres will continue to affect the demand of gas transportation and storage services. The relative decline of production in the southern states will further increase the need to transport gas from Queensland and, to some extent, the Northern Territory to meet demand.

This growing dependence on the infrastructure of a small number of operators is concerning given the monopoly pricing previously observed by the ACCC largely persists. Since our last report, most transportation prices have moved in line with inflation, maintaining monopoly pricing.

Where gas must travel on multiple pipelines, the transportation costs can be significant. For example, the standing price for transporting gas from Wallumbilla to southern demand centres can range from $2.24 to $2.58/GJ which is a significant proportion of commodity gas prices. The cost of transporting gas from the Northern Territory is significantly higher.

The regulatory reforms for gas pipeline regulation announced in April 2022 should improve transparency by pipeline operators and should strengthen the relative bargaining position of shippers.

The local monopolies enjoyed by pipeline operators are also a feature of gas storage infrastructure. Storages are also expected to play an increasingly important role in meeting peak demand periods throughout the year. The Dandenong LNG storage facility plays an important role in meeting intraday peak periods for retailers and other major users, as well as system security more generally. AEMO recently contracted 60TJ of LNG reserve (storage capacity) on 20 January 2022 to counteract the threat to system security in the Victorian Transmission System.

Ensuring sufficient supply in the east coast market is critically dependent on measures to improve competition and encourage timely supply

Recent events across the east coast’s gas and electricity markets have shown the consequences of having insufficient gas supply to meet demand and ineffective upstream competition. Concerningly, supply conditions in the east coast gas market are expected to deteriorate further in 2023, with a significant supply shortfall now expected. This is expected to occur against the backdrop of a highly concentrated upstream market, with competition posing little constraint on the behaviour of producers.

In January 2021 we announced our intention to undertake a review of upstream competition and the timeliness with which gas is brought to market. This review is being undertaken in response to concerns raised throughout the Inquiry about the degree of concentration in this part of the market and the structural and behavioural factors that may be impeding competition or limiting gas supply. The need for the review has been reinforced by:

• the pricing behaviour we have observed over the course of the Inquiry and our review of suppliers’ pricing strategies, which indicates that competition is posing little constraint on producers’ pricing decisions

• the C&I user surveys we have undertaken, which have consistently raised concerns about the lack of effective upstream competition and the adverse effect this has on selling practices, gas prices and non-price terms and conditions in GSAs.

Stage 1 was completed in January 2022 and focused on the structural factors that may be impeding competition or the timeliness of supply. We found that:

• Greater diversity and more timely supply could be encouraged through changes to government processes for releasing acreage and approving, monitoring and enforcing compliance with work programs.

• Upstream competition and the timeliness of supply could be significantly improved by reducing the infrastructure, regulatory and capital barriers faced by producers, including by introducing a light-handed third party access regime for upstream infrastructure.

Stage 2 has focused on the degree of concentration in the part of the market and the behavioural factors that may be impeding competition or the timeliness of supply. Our key findings of this stage of the review are that:

• The upstream market is highly concentrated and dominated by the three LNG exporters and their associates. In 2021, the three LNG exporters and their associates had influence over close to 90% of the 2P reserves in the east coast, through a combination of their direct interests in 2P reserves, associates, JVs and exclusivity arrangements. This highlights the effective control that the LNG exporters have over the supply and development of gas in the east coast, as well as competition in the domestic market.

• JVs can adversely affect competition if participants do not put in place and adhere to robust ring-fencing arrangements that prevent the sharing of commercially sensitive information,8 with other projects in which JV participants have an interest. A JV participant can also have the incentive and opportunity to exploit their position in a JV to delay the development of gas if it improves the participant’s competitive position in other projects.

• Joint marketing by incorporated and unincorporated JVs is more prevalent than we expected, with the LNG exporters and some other producers engaging in joint marketing in the domestic market without authorisation. This results in a material reduction in the number of producers competing to supply gas into the domestic market.9

• Exclusivity provisions in GSAs entered into between domestic producers (as sellers) and LNG exporters (as buyers) are restricting the ability of domestic producers to compete to supply gas into the domestic market. These provisions can also reduce the incentive that domestic producers have to develop gas over time and result in development decisions being based on the requirements of the LNG exporters, rather than the domestic market.

• Mergers and acquisitions of other producers, tenements or interests in JVs by larger producers, can result in a reduction in producers competing to supply gas into the market and slow the progress of gas development.

Together with the high degree of concentration in this part of the market, these arrangements contribute to a lack of effective upstream competition in the east coast. They may also increase the risk of coordinated conduct and increase the market power of the LNG exporters. This is concerning, given the supply conditions that are expected to prevail in the east coast in 2023 and beyond, and the reliance that will be placed on the LNG exporters to supply more gas into the domestic market.

Entering into these types of arrangements without authorisation risks breaking the restrictive trade practices provisions in Part IV of the CCA if they amount to cartel conduct, or have the purpose, effect or likely effect of substantially lessening competition.

While in the past producers may have considered that these arrangements would not substantially lessen competition, in a concentrated and tight market the effect on competition can be heightened. We will continue to review some of these arrangements and, where appropriate, consider enforcement action.

Producers should also consider whether they could implement changes to their arrangements to help improve competition and the timely supply of gas to the market as a matter of priority.

Future work of the inquiry

We expect to provide our next interim report in January 2023. Consistent with the 2017 direction from the then Treasurer to conduct a wide-ranging inquiry to improve transparency and monitor gas supply, and the most recent letter from the current Treasurer to monitor and report on prices and the supply of gas, we will provide updates on:

• the prices offered and agreed for gas supply for 2023

• the gas supply outlook for 2023 and the longer term outlook to 2034

• the C&I gas user experience

• the pricing and utilisation of transportation and storage services.

We will continue publishing the LNG netback price series, and make information available and policy recommendations where we consider it appropriate and necessary. Our priorities over the next 12 months will be to:

• continue our review of upstream competition, in particular how producers make decisions about when to bring gas to market and any potential competition concerns under the CCA

• assist the Australian Government as appropriate as it reviews the ADGSM and renegotiates the HoA • assist in the ADGSM process to determine if 2023 is likely to be a shortfall year, should the government commence that process • monitor and report on compliance with the HoA signed with LNG exporters

• monitor and report on the implementation of the Gas Code of Conduct • commence our examination of competition in the supply of gas to C&I users.