At least they had one. Unlike the poor working sods Downunder who have been blamed for a profits-driven inflation cycle. Still, it looks like it’s well and truly over in the US as well. Goldman with the note.

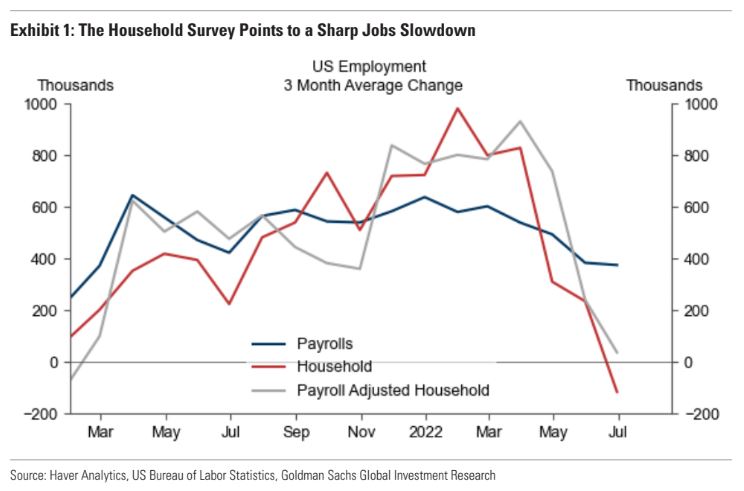

Fears of an imminent US recession have abated somewhat after the 372k nonfarm payroll gain reported for June. But there is no doubt that a labor market slowdown is underway. Job openings and quits are declining, jobless claims are rising, the ISM employment indices in manufacturing and services have fallen to contractionary levels, and many publicly traded companies have announced hiring freezes or slowdowns. Perhaps most tellingly, the household survey of employment has shown essentially no job gains for the past three months, both on a headline basis and when adjusted to the definitions of the establishment survey. While the household survey is much noisier than the establishment survey on a month-to-month basis, it picks up changes in net new firm creation in real time and therefore often outperforms the establishment survey at cyclical turning points, provided both measures are averaged over several months. This suggests that the still-robust nonfarm payroll prints of recent months probably overstate true job growth.

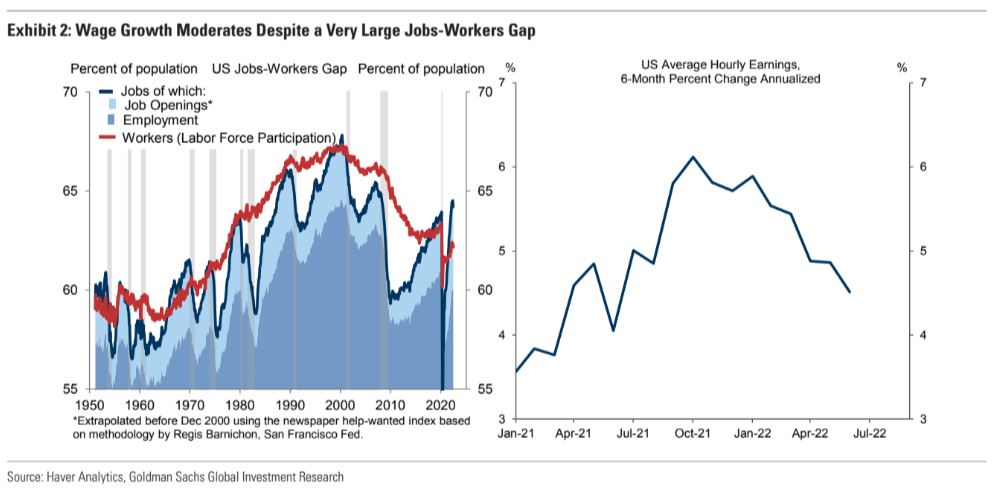

How much adjustment is needed to rebalance the labor market? So far, our jobs-workers gap has only declined modestly to 5.3 million, still the biggest in postwar history both in absolute terms and relative to the population. In estimating the degree of labor market overheating, however, we would also put some weight on the recent wage slowdown. The 6-month annualized growth rate of average hourly earnings has declined from 6.1% in October 2021 to 4.5% in June 2022, probably reflecting a combination of slowing economic activity and waning temporary boosts, including last year’s pandemic unemployment benefits and the need to incentivize people to return to work when covid death rates were still high. To be sure, even 4.5% is 1pp above the wage growth rate we estimate is consistent with 2%inflation, but the slowdown suggests that the jobs-workers gap might overstate the imbalance in the labor market. (Another explanation might be that expectations are so anchored that even a large overheating would only have given us a modest wage acceleration had it not been for the special factors of 2021.)