The Chinese recovery had a few good weeks but it is in trouble again.

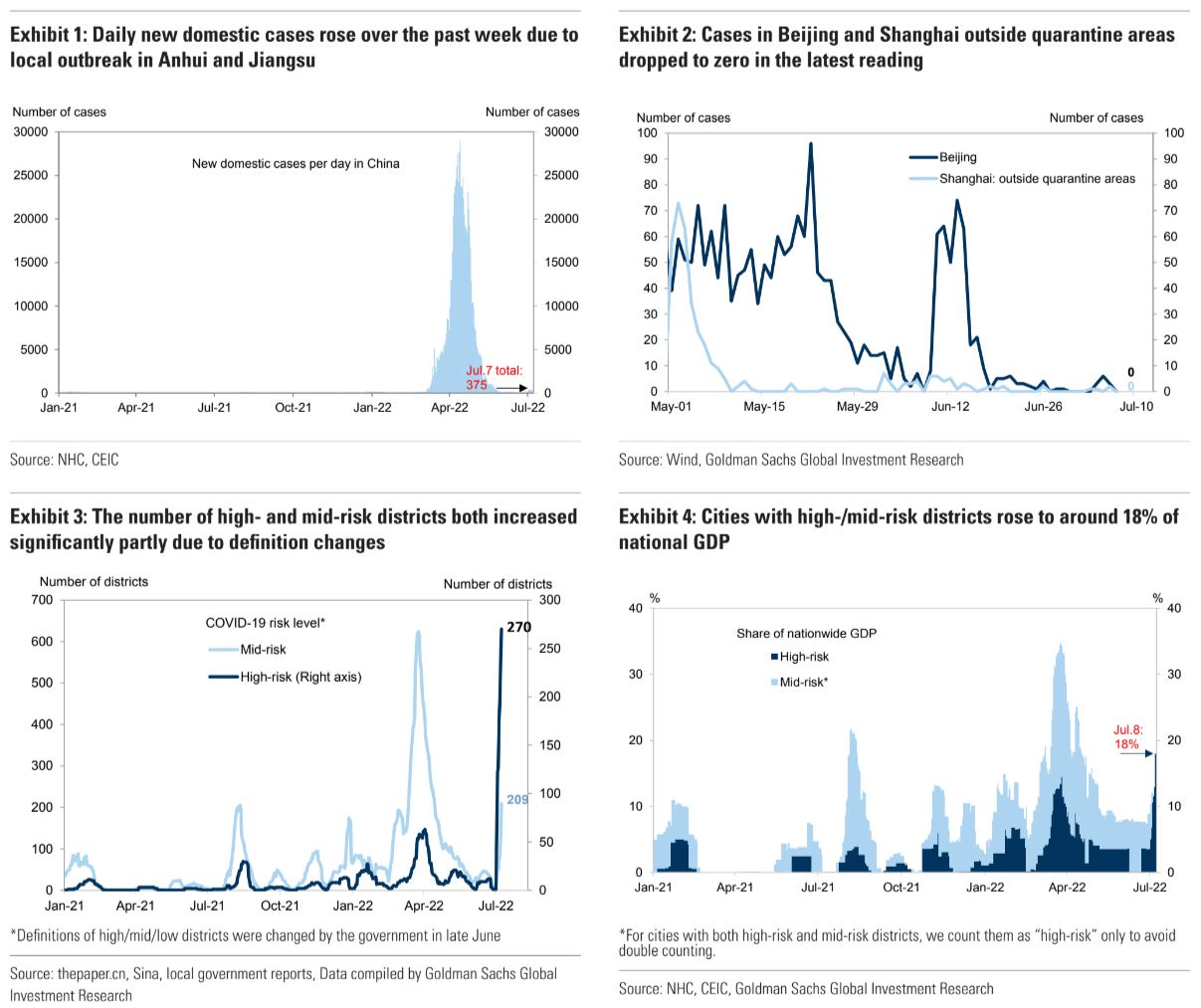

COVID being the first problem:

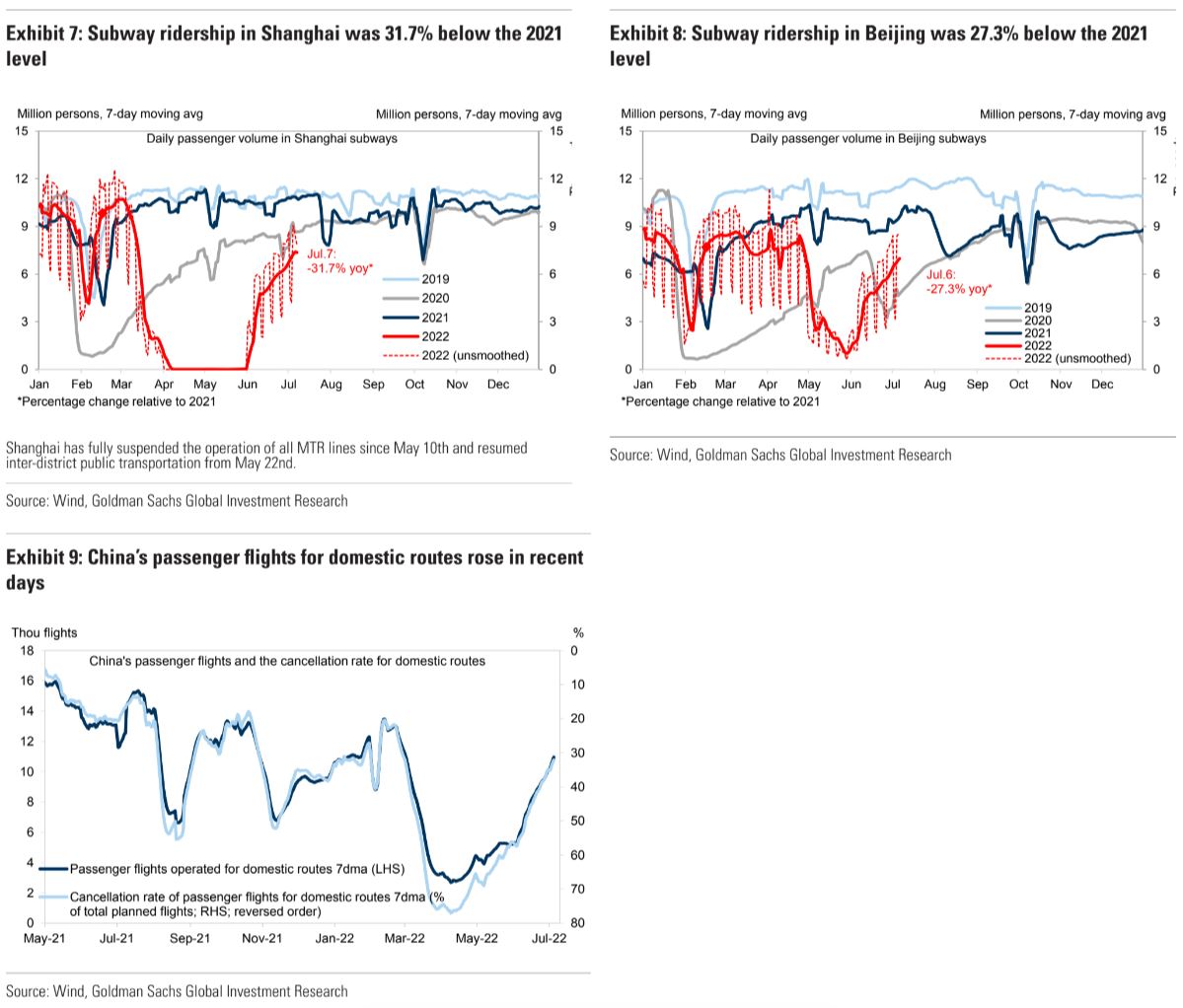

Mobility is lifting so expect more disease:

The Chinese recovery had a few good weeks but it is in trouble again.

COVID being the first problem:

Mobility is lifting so expect more disease:

The full text of this article is available to MacroBusiness subscribers