Coolabah Capital’s Chris Joye phoned me yesterday to tell me that Sydney dwelling values are crashing at their fastest monthly pace in at least 30 years, according to CoreLogic’s dwelling values index (which he helped create).

So I went and checked, and it turns out that he’s right!

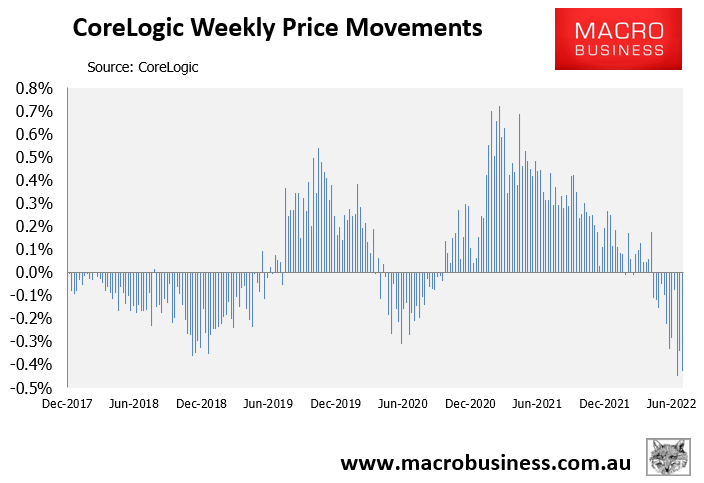

As shown in the next chart, the CoreLogic daily dwelling values index, which captures price changes across the five major capitals, tanked by 0.43% in the week ended 28 July – the 12th consecutive weekly decline:

Weekly house price declines are getting steeper.

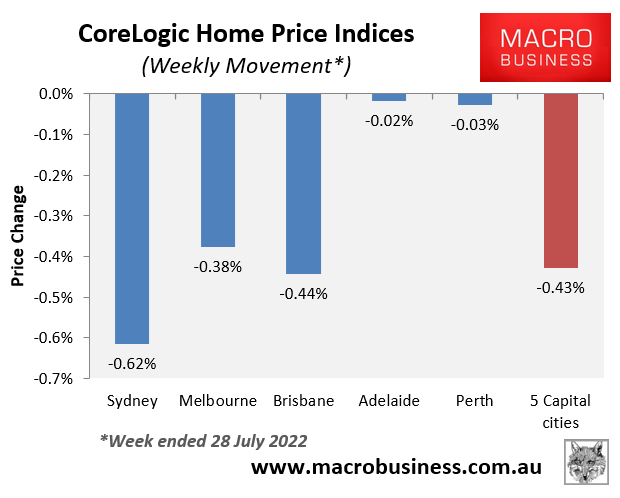

Once again, the weekly decline was led by Sydney where values tanked another 0.67%; although all major capitals recorded losses:

Sydney leads across-the-board house price falls.

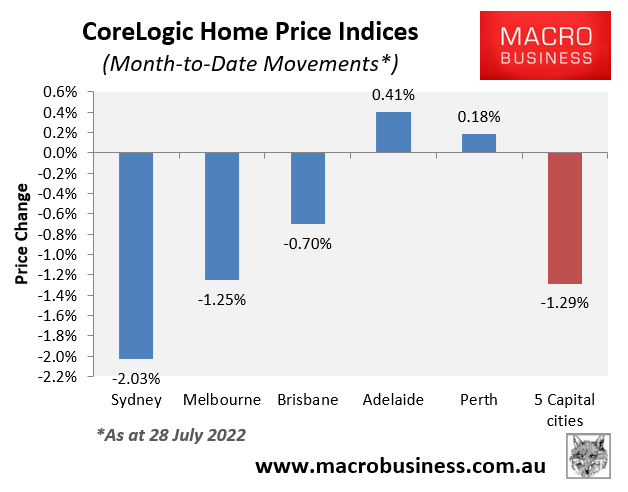

So far in July, Sydney dwelling values have crashed 2.03%, with Melbourne (-1.25%) and Brisbane (-0.70%) also posting falls. These markets have driven a 1.29% decline at the 5-city aggregate:

Big house price falls in July.

With three days to go in July, Sydney’s 2% monthly fall is already the largest in at least 30 years, according to the CoreLogic index (Chris Joye notes that the CoreLogic dwelling values index is unreliable prior to 1990).

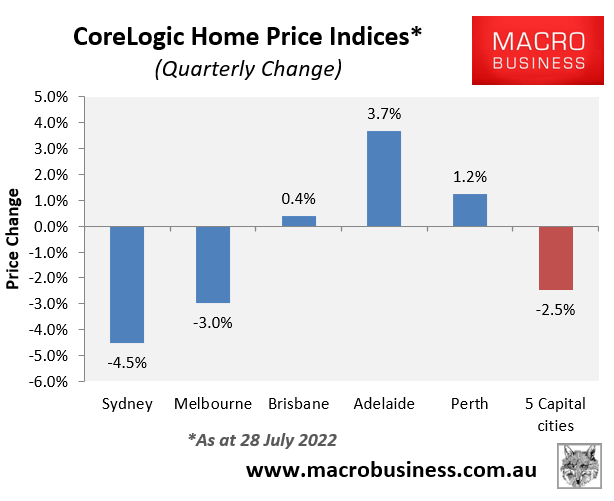

Quarterly value declines have also accelerated, down 2.5% at the 5-city aggregate level, driven by heavy falls across Sydney (-4.5%) and Melbourne (-3.0%):

Accelerating declines across Sydney and Melbourne.

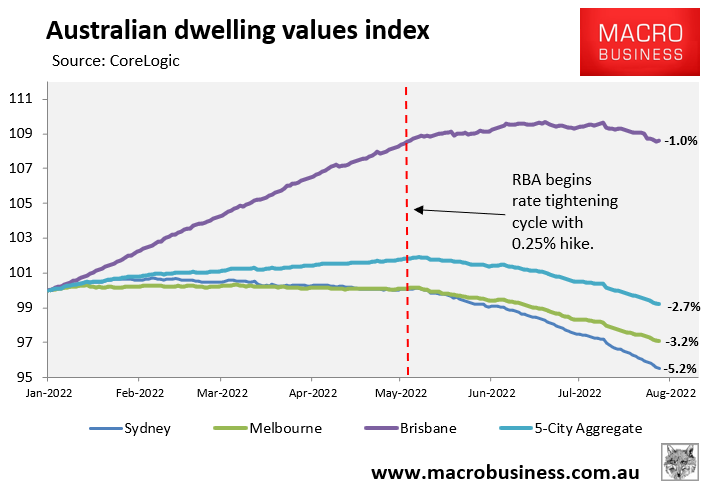

The final chart shows the peak-to-trough declines, which have accelerated since the RBA first commenced its monetary tightening cycle in early May:

Rising rates is driving house prices down.

Sydney dwelling values have tanked 5.2% from their February 2022 peak, while Melbourne’s are down 3.2%. Brisbane dwelling values only began falling in mid-June, but are already down 1.0%.

The RBA has so far only lifted the official cash rate (OCR) to 1.35%. With ANZ, Westpac and the futures market each tipping an OCR above 3% by year’s end, Australian house prices are set to record heavy falls.

While Sydney and Melbourne values will fare worst, given their status as Australia’s most pricey markets, soon the correction will spread to nearly every housing market across the nation, both capital city and regional.