Fairfax’s Jess Irvine has done a good job exposing the fearmongering tactics used by the superannuation industry to make Australians believe they will never have enough savings in retirement, which they have also used to leverage policymakers into lifting the superannuation guarantee:

Enough of this scaremongering from the super industry that you need about a squillion dollars (paraphrasing) to avoid eating baked beans every day in retirement.

Don’t forget, of course, that the super industry is paid a percentage fee on every dollar you scrimp and save for when you stop working.

Super Consumers Australia.. released its first “rule of thumb” estimates of the true dollar figures workers at certain ages need to accumulate in super to secure adequate income in retirement.

“Bottom line: a single person retiring between age 65 to 69 today would need to have saved $258,000 in super to draw a “medium” level of income in retirement of $38,000 a year (including income drawn from super and the age pension).

The figures are based on analysis of the actual spending levels of retiree households today…

By comparison, the super industry estimates a single person needs to draw an annual income of about $46,000 to fund a “comfortable” retirement (requiring a super balance of $545,000). So, that puts their “comfortable” standard somewhere at the upper end of actual spending of retirees. Interesting…

The industry’s definition of a “comfortable retirement” is laughable when compared against what a typical Australian takes home in pay.

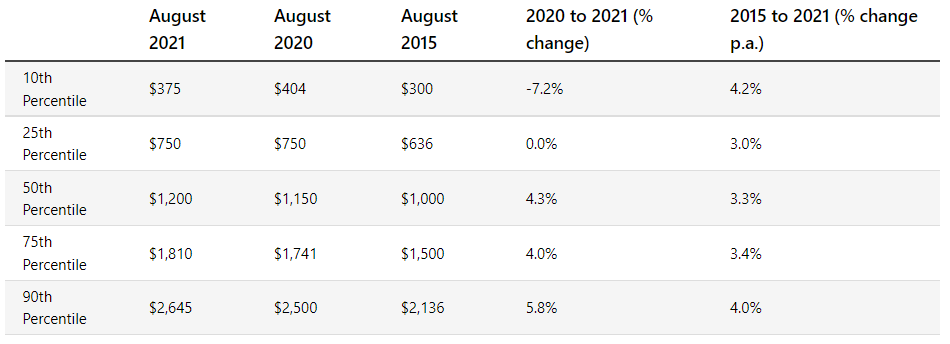

According to the Australian Bureau of Statistics (ABS), the median Australian employee earned $1,200 a week ($62,400 a year) as at August 2021:

The median Australian earns $62,400 a year before tax.

These are gross earnings, however, so the typical Australian employee must also deduct around $11,000 in personal income tax and the Medicare Levy.

Unlike most retirees whom own their home outright, the median working Australians also must pay rent or a mortgage. Many also have the financial burden of supporting children.

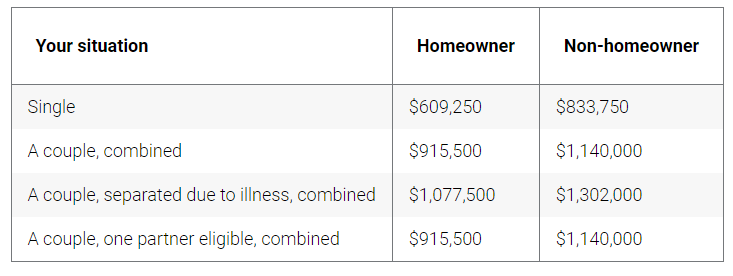

Those with a “comfortable retirement” level of super ($545,000) will also receive a part pension and discounts on medicines, alongside receiving seniors discounts on a range of expense items (e.g. movie tickets).

Part pension assets test.

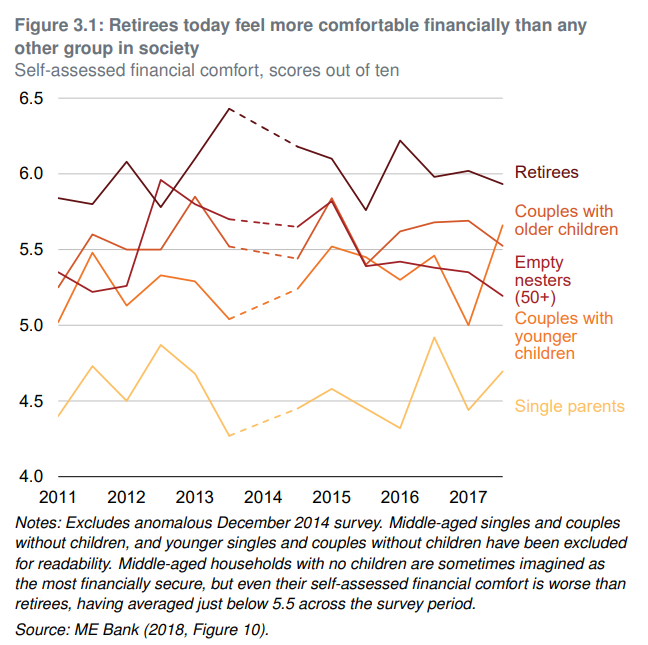

It should not be surprising, then, that modelling from the Grattan Institute found “that the vast majority of retirees today and in future are likely to be financially comfortable” with retirees “less likely than working-age Australians to suffer financial stress”:

Retirees are the most financially comfortable cohort in Australia.

Clearly, the ‘comfortable retirement’ estimate used by the superannuation industry is more luxurious than most Australians enjoy over their working lives. It is blatant propaganda aimed at pushing policy makers and members to funnel more money into the super, in turn enabling the industry to skim fatter management fees. It is pure and simple rent-seeking.

As long as there is easy money to be made, the super industry will continue to talk its own book regarding a ‘comfortable retirement’.