RBA to plunge Australia into catastrophic recession

ANZ Bank yesterday dramatically lifted its forecast for Australia’s official cash rate (OCR) to 3.35% by November 2022.

According to David Plank, head of Australian economics:

“Our expectation is that the RBA will deliver this via four more successive 50 basis point rate hikes in August, September, October and November. This 200 basis points of additional tightening sees the cash rate target at 3.35 per cent by November.”

“A cash rate of 3.35 per cent implies that household interest payments as a percentage of household income peak below the level reached in 2008.”

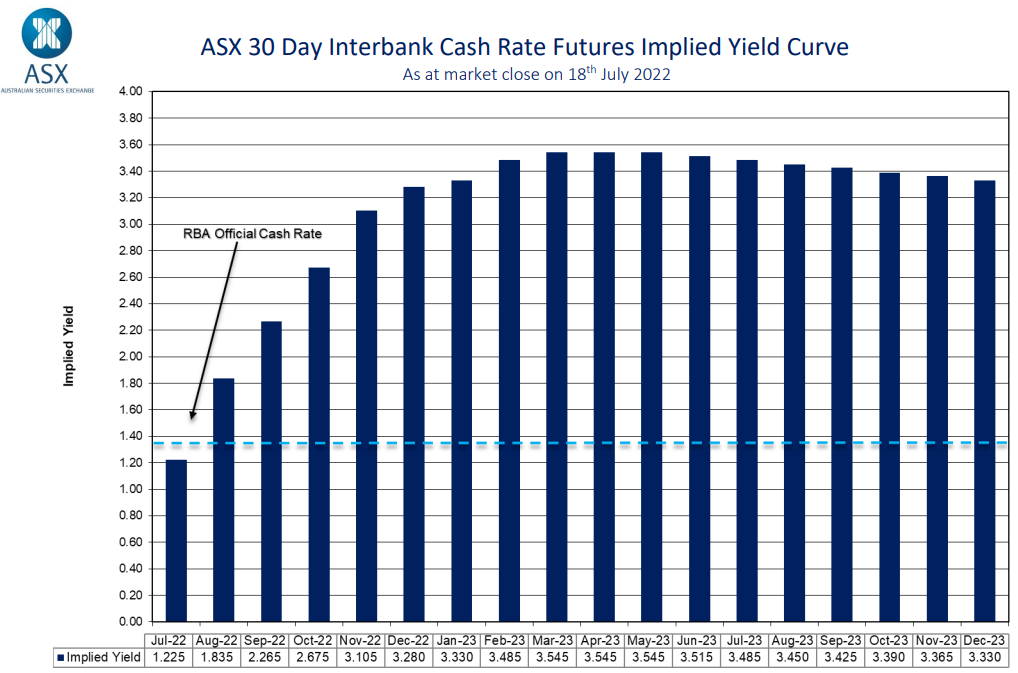

ANZ’s forecast basically mirrors the futures market, which tips an OCR of 3.3% by December, and a peak OCR of 3.5% by March 2023:

Biggest interest rate increase in Australia’s history.

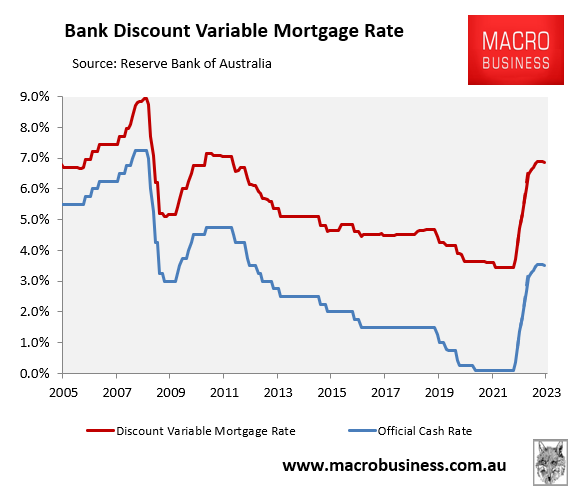

If the ANZ’s forecast came to fruition, it would lift Australia’s average discount variable mortgage rate to 6.7% by November, whereas the futures market’s forecast would see the mortgage rate climb to 6.9% by March 2023:

A near doubling of mortgage rates in only seven months!

Either way, Australians would face more than a 3% lift in variable mortgage rates in only seven months – the biggest rate of increase in the nation’s history.

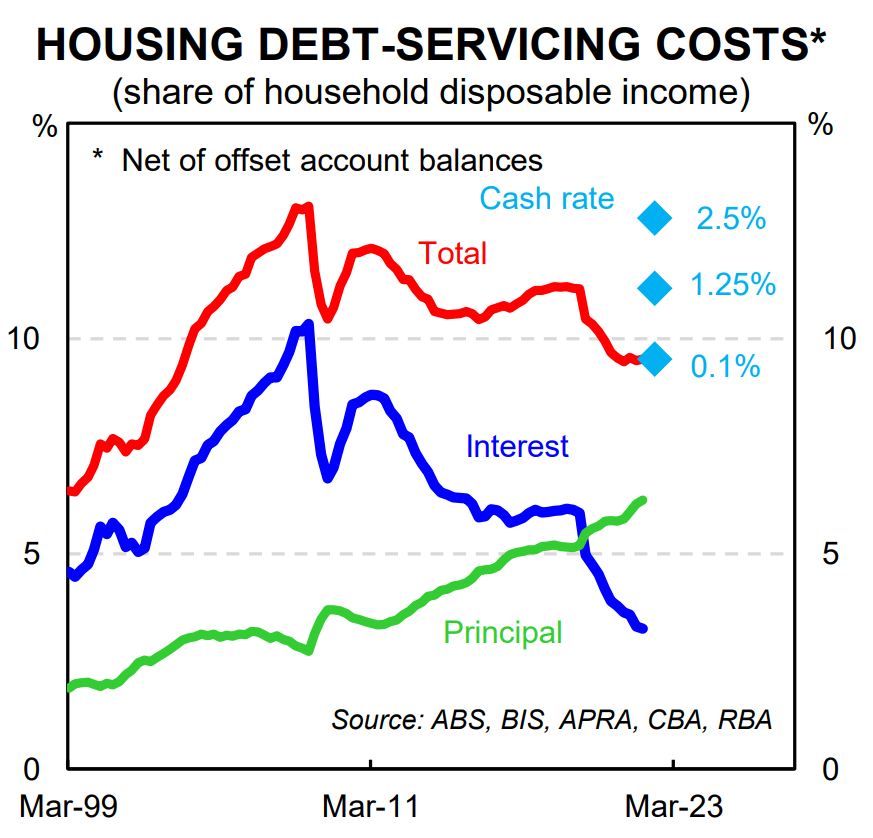

David Plank is also misguided when he claims that “household interest payments as a percentage of household income peak below the level reached in 2008”. When we add principal debt repayments into the mix – which have risen significantly alongside Australia’s house price boom – household debt repayments would soar well above their 2008 level, as illustrated below by CBA:

ANZ’s OCR forecast would lift debt repayments above the 2008 peak.

An OCR of 2.5% would lift average household debt repayments to around their 2008 peak. Therefore, a 3.35% OCR, as projected by ANZ, would lift debt repayments even higher.

The impact on the Australian economy would be devastating as the extra household income sacrificed in mortgage repayments, in addition to crashing house prices, would crater household consumption spending – the economy’s biggest driver.

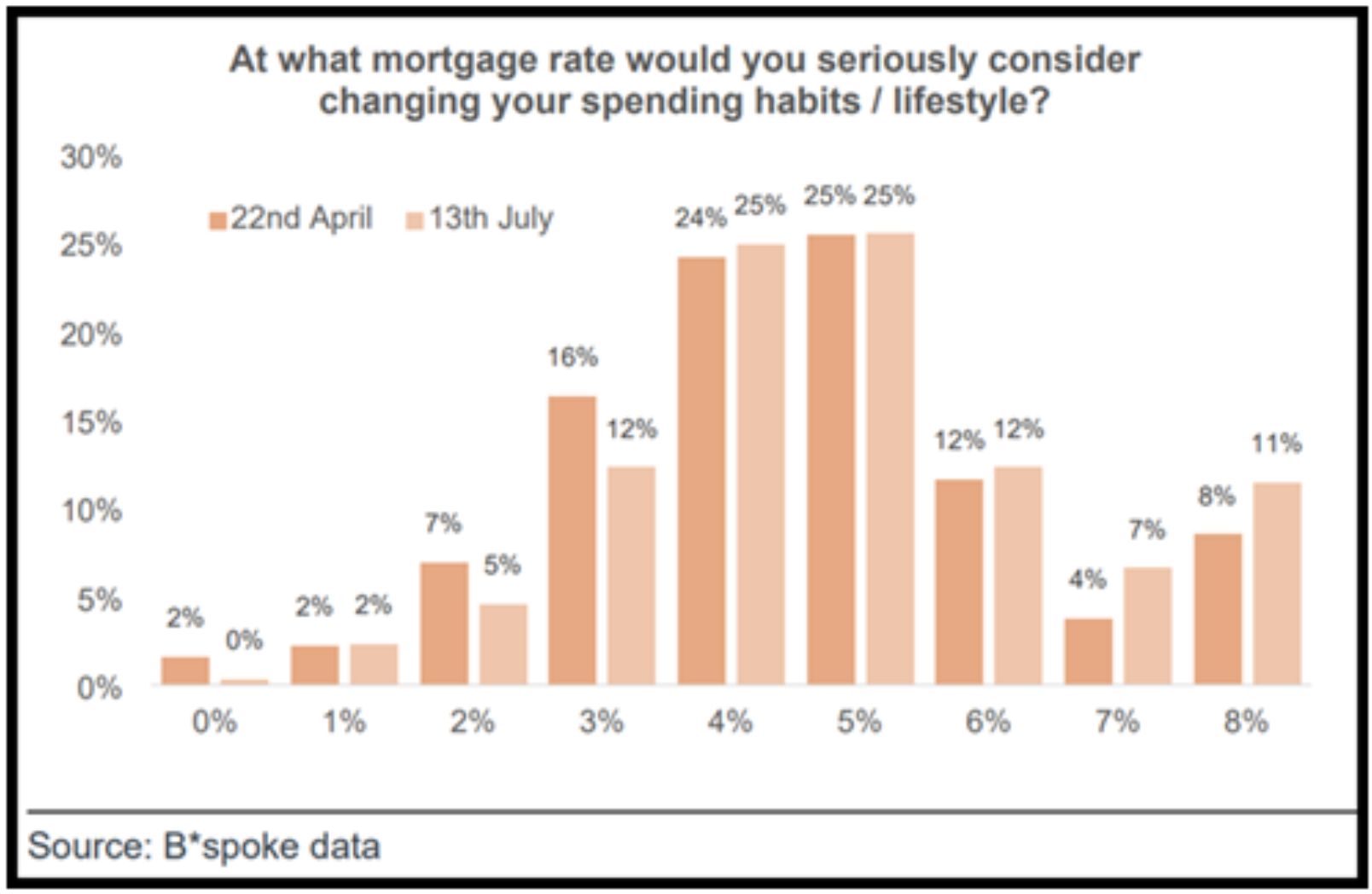

Indeed, a recent survey from Barrenjoey Capital Partners showed that 82% of Australian mortgage holders would cut back on consumption spending if mortgage rates climbed above 6%:

82% of mortgaged households would cut consumption under ANZ’s forecast.

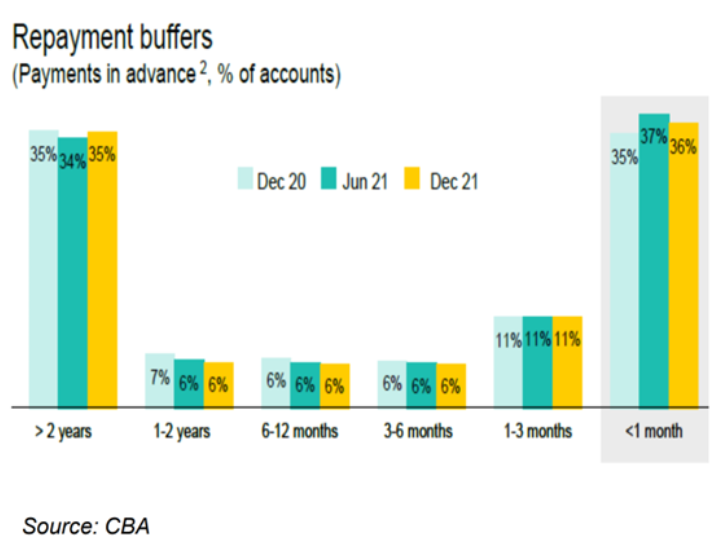

Nor would Australian households’ supposedly strong savings save the day. According to CBA, 36% of all borrowers have zero buffer and nearly 50% of borrowers have less than 3 months:

Nearly half of Aussie mortgaged households have inadequate savings.

Thus, Australia’s households are extremely sensitive to increasing mortgage repayments arising from RBA rate hikes, and they will necessarily cut back heavily on consumption if mortgage rates lift too far.

The RBA, therefore, must tread very carefully on interest rates. If it follows the hawkish forecasts of ANZ or the futures market, then the Australian economy will plunge into an unnecessary and painful recession.