NAB’s Q2 residential property survey is out, with the bank viciously downgrading its outlook for Australia’s housing market.

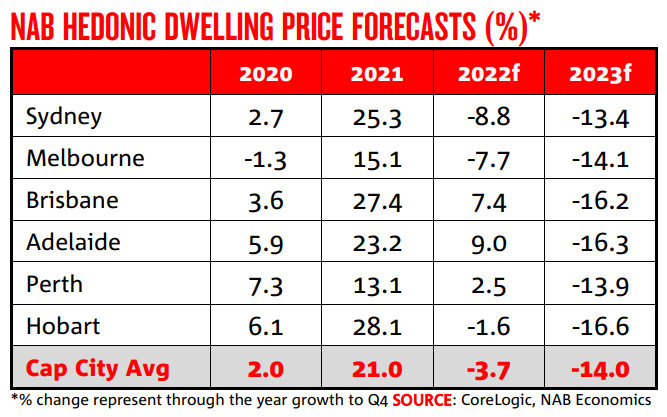

NAB now forecasts that Sydney and Melbourne dwelling values will plunge by around 22% over 2022 and 2023, with the other capitals also forecast to record heavy falls next year as the cash rate soars to 2.6%:

We have revised down our outlook for property prices, and now expect a larger peak to trough fall of around 18%. Sydney and Melbourne are expected to lead the declines, though the impact of higher rates is expected to impact all capitals. That sees the 8-capital city dwelling price index end 2022 down 3.7% (previously +2.5%) before falling a further 14% in 2023 (was -9.3%)…

In an historical context, this would be a very large fall in nominal terms, but is expected to occur alongside a relatively steep increase in interest rates and comes after a 25% increase in prices through the pandemic alone…

We largely see the adjustment in prices coming through reduced borrowing power, which will bind more in the larger capitals that have larger affordability issues…

Both Sydney and Melbourne have seen the most significant run-ups in prices over the past decade as rates have trended lower and most likely face the most binding affordability constraints…

On inflation, we see both headline and underlying measures rising further, peaking in the second half of 2022 – but remaining well above the target band in 2023. While many of the transitory factors that have been a significant boost to prices will fade, or even unwind, a tighter labour market and faster wage growth will eventually see domestic inflation pressure build. As a result, we think the RBA will continue to normalise rates at a rapid pace, lifting the cash rate by 50 bps at each of the next two meetings, with a 25 bps follow up in November, taking the cash rate to 2.1% by year end. We see a further two 25 bps increases in 2023, taking the cash rate to a broadly neutral level at 2.6%.

NAB’s price forecast looks about right in the context of a terminal cash rate of 2.6%.

Advertisement

That said, the futures market is tipping the cash rate to hit 3.7% by mid next year. If this was to occur, dwelling values would obviously fall much further.

Ultimately, how deep prices fall depends on the aggressiveness of the Reserve Bank of Australia.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.