Of course, MOAR is coming. But not before an epic rout in everything! This is not bullish bonds enough for me but it is in the right direction. BofA with the note.

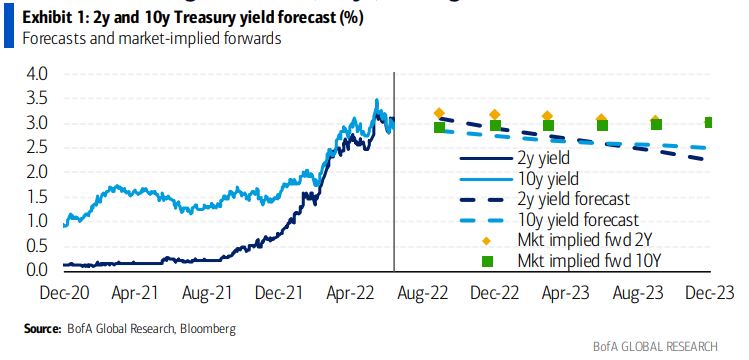

US rate forecasts revised lower, with less-aggressive Fed

The US rates team is making substantial downward revisions to our rate forecasts following our US economics team’s new call for a mild 2022 recession and lower Fed funds rate path. We are lowering our 10yT end ’22 forecast from 3.50% to 2.75% and end ’23 forecast from 3.25% to 2.50%. Our new forecasts are very bullish vs the forwards given the expectation for Fed rate cuts in 2H23 and 1H24 (Exhibit 1).