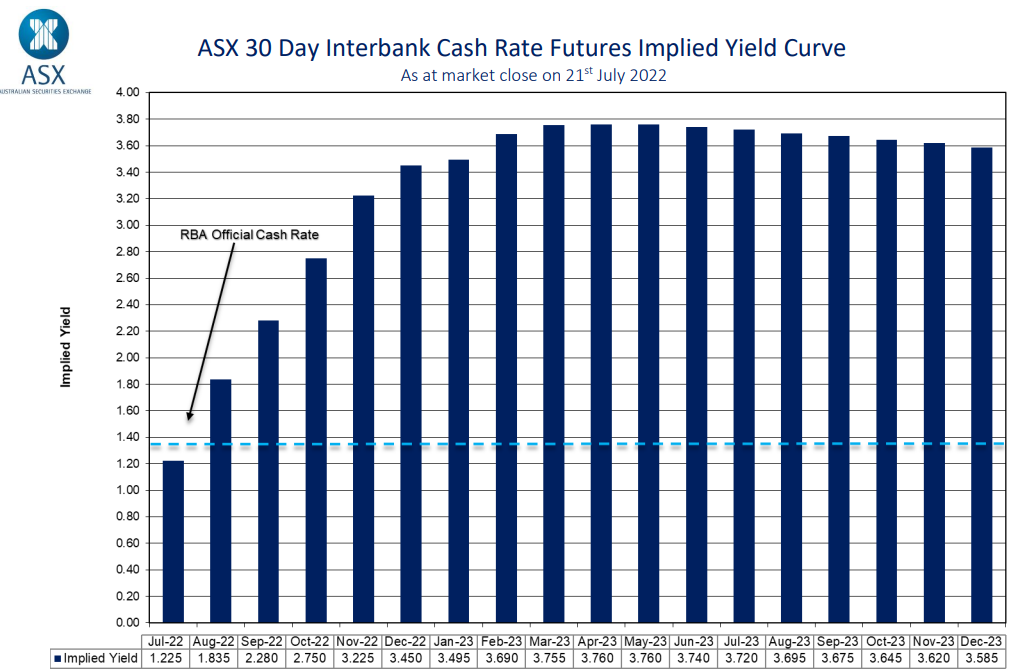

A week ago, the futures market tipped the Reserve Bank of Australia (RBA) to hike the Official Cash Rate (OCR) to 3.45% by December and to 3.75% by March 2023:

Futures market cash rate forecast: 21 July 2022

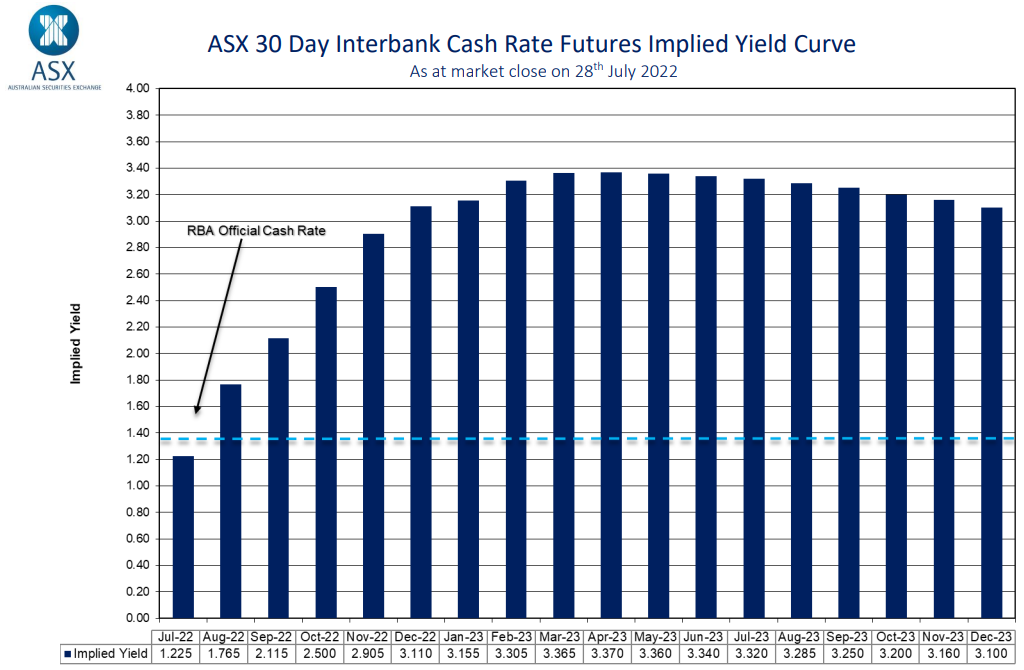

At the market close on 28 July, the futures market had cut its OCR forecast to 3.1% by December and 3.35% by March, a downgrade of 40 basis points:

Futures market cash rate forecast: 28 July 2022

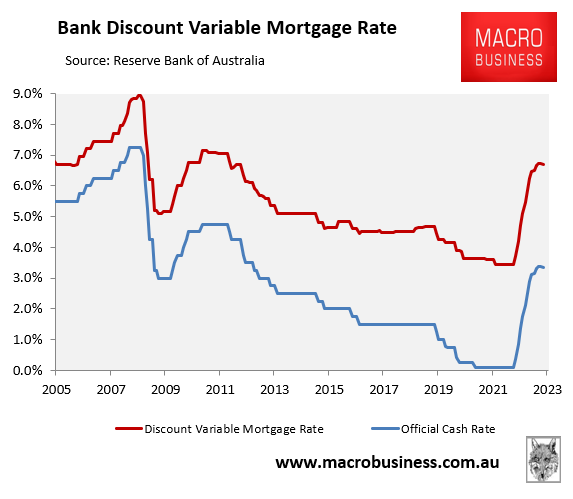

The market’s OCR forecast remains too bullish in my opinion. Because if it came to fruition, it would drive the average discount variable mortgage rate to 6.7% by March 2023, assuming increases in the OCR are passed onto mortgage holders. This would still represent a near doubling of mortgage rates from their end-April 2022 level of 3.45%:

Average discount variable mortgage rate to double.

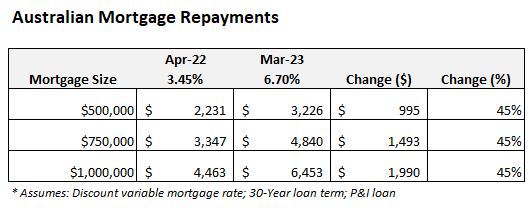

Thus, in only 11 months, Australia’s average discount variable mortgage rate would go from its lowest level on record to its highest level in a decade. In turn, average principal and interest mortgage repayments would soar by 45%:

Mortgage repayments would rise 45% under futures market’s forecast.

Given Australian households are among the most indebted in the world, such a sharp lift in mortgage rates would plunge thousands of households into severe financial stress, would slash household spending, would crash house prices and construction, and would drive the economy into recession.

For these reasons, I still view the market’s OCR forecasts as overly hawkish and unrealistic.

Surely the RBA won’t be that foolhardy? Only time will tell.