A manic bond bid has emerged:

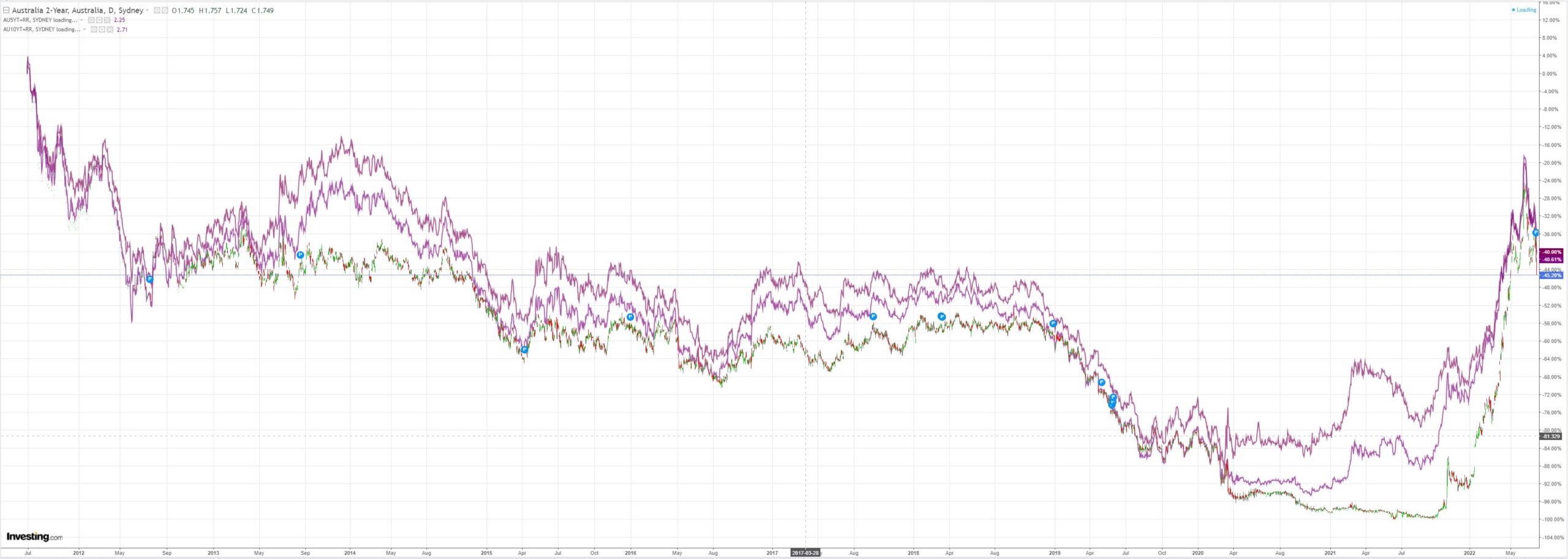

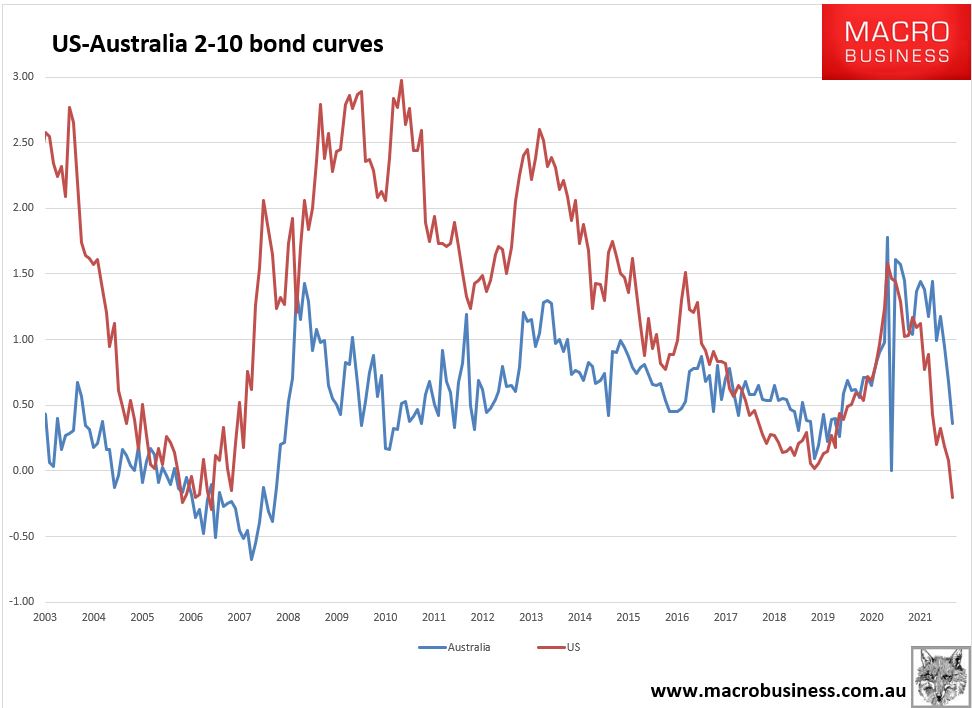

The Australian cycle is lagging that of the US by a quarter or two. The US is already in recession with an inverted yield curve. We’ll invert in the next quarter:

More from The Market Ear:

Advertisement

Yields – giant head and shoulders? US 10 year is close to the massive 2.7% level. A close below and things could get very “dynamic”. It looks like a huge head and shoulders “staring” at us… Refinitiv

TLT – time to try the huge trend line? On June 22 in our post The revenge of the TLT?, we outlined the long TLT logic. We have moved higher since then and the TLT is now at very big levels. The longer term negative trend line is right around these levels, with the 100 day some higher. A close slightly higher and the second phase of this trade could easily start kicking in. Remember what Albert Edwards wrote in June: “Who cares about how deep the recession will be. Much more interesting according to Soc Gen’s Albert Edwards is how much will yields fall. “ Refinitiv

Some rate moves are more violent than others German 10 year has been the relatively more “wild” 10 year compared to the US 10 year. German yields trying to tell us something? Refinitiv

Not all volatilities are calm EUR rate volatility is a special breed… BofA

Recession probability ain’t low MS writes: “Deterioration in the underlying components has been broad based, pushing the probability of a recession within 12 months sharply higher. A flat or slightly rising unemployment rate is a key precursor to recessions, as is an accelerating rate of YoY PCE price inflation.” MS

Recession – almost a slam dunk DB reminds us: “We still think a recession is almost a slam dunk over the next 12 months but want to see more evidence of employment rolling over before we would call the current US environment a recession”. DB/@carlquintanilla

Tightening in a pic Financial conditions have tightened by the equivalent of 283bp in fed funds since the start of 2022. MS

Cuts du jour EDZ2-EDZ3 spread holding close to recent lows… Refinitiv

Sectoral correlations to real yields US sectoral correlations to real yields, past 5 years. JPM

That ultra-low liquidity in the treasury market The sharp rise in delivered volatility is largely responsible for the steep decline in liquidity conditions in the treasury market. JPM