Risk sentiment remain ebullient overnight as markets basically ignored the latest disappointing US GDP print as German inflation picked up higher than expected. Wall Street and European stocks rose around 1% across the board while the USD was down slightly, as Euro remains in an holding pattern with the Australian dollar almost pushing through the 70 cent level. Bond markets saw some more tightening of yields with 10 year Treasuries moving well below the 2.7% level while commodity prices reduced in volatility as oil prices stabilised as Brent crude stayed above the $100USD per barrel level while copper and gold both rose nearly 1.5%, the latter now at a new weekly high above the $1750USD per ounce level.

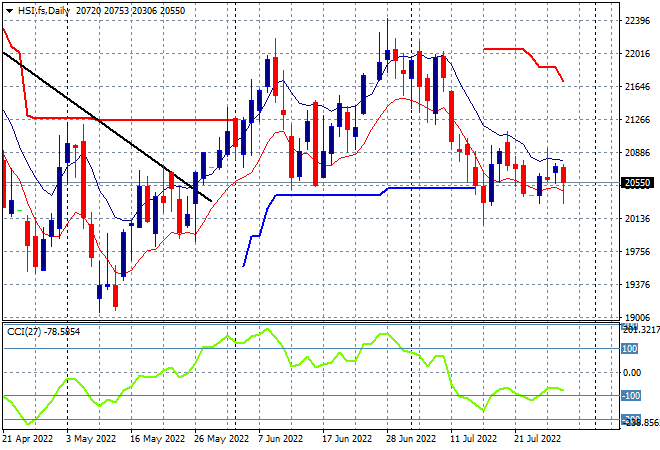

Looking at share markets in Asia from yesterday’s session, where mainland Chinese share markets were up at the halfway point but slowed down into the close with the Shanghai Composite finishing up just 0.2% higher at 3282 points while the Hang Seng Index was still in retracement mode, down 0.2% to 20623 points. Sentiment continues to wane on the daily chart with considerable overhead resistance and daily momentum readings remaining nearly oversold as the previous swing play reverts back to the downtrend although some support is building at the 20000 point level:

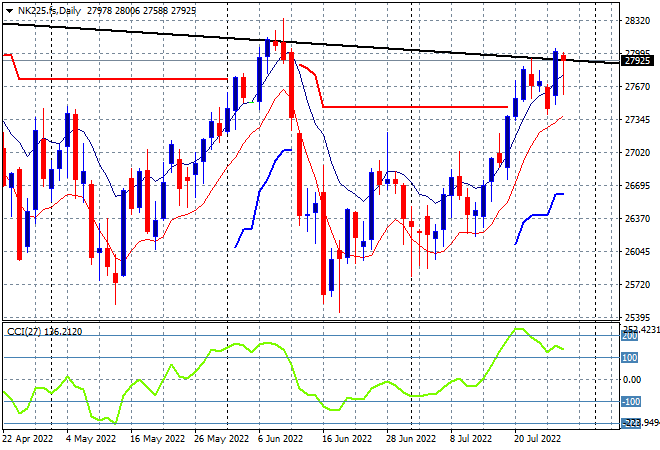

Japanese stock markets did a little bit better, with the Nikkei 225 up 0.3% to 27815 points. Futures on the daily chart are now suggesting a proper breakout after the reaction to the Fed, with resistance at the previous highs at 28000 points still the area to beat in today’s session. Daily momentum remains in an overbought status and while price has made a new weekly high, this market is in a pause phase for now with the overall monthly/weekly trend (sloping black line above) still in play: