Risk sentiment was steady overnight as markets remain in a holding pattern waiting for the next Federal Reserve interest rate hike at the upcoming FOMC meeting this week. Both European stocks and Wall Street had scratch sessions amid lower volatility while on currency markets the USD pulled back slightly although it clawed back some ground lost against other safe havens like Yen, as Euro was flat above the 1.02 handle while the Australian dollar remained above the 69 cent level. Bond markets saw some loosening of yields with 10 year Treasuries lifting slightly to the 2.84% level, as US interest rate futures continue to indicate a 75bps rate rise at the next Fed meeting. Commodity prices were still volatile with Brent and WTI crude oscillating around the latest Ruzzian machinations while copper gained nearly 2% again while gold held on to its recent gains at the $1720USD per ounce level.

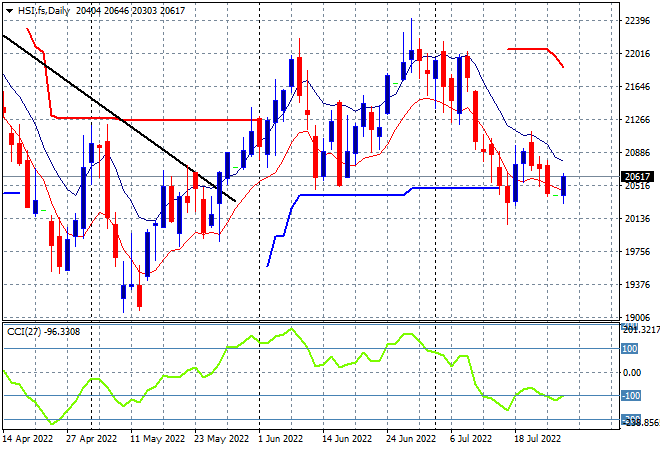

Looking at share markets in Asia from yesterday’s session, where mainland Chinese share markets slid into the close with the Shanghai Composite down 0.6% to 3250 points while the Hang Seng Index was all set to lose 1% before a recovery saw it close only 0.2% lower at 20562 points. Sentiment continues to wane on the daily chart with considerable overhead resistance and daily momentum readings remaining oversold as the previous swing play reverts back to the downtrend although some support is building at the 20000 point level:

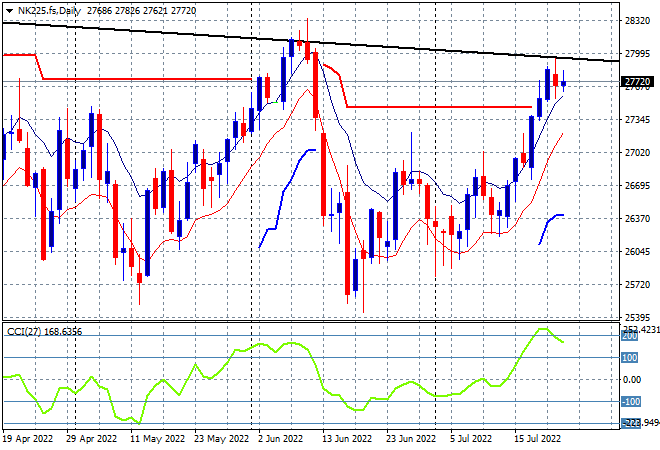

Japanese stock markets finally reverted after a week long surge, with the Nikkei 225 closing down 0.8% to 27699 points. The daily chart is suggesting this breakout may not have the legs to continue, with resistance building at the previous highs at the 28000 point area as daily momentum reverts from its overbought status. Although price has made a new weekly high, this market is in a pause phase for now: