Risk sentiment remains solid despite the ECB coming out flying with a 50bps rate hike overnight, with Wall Street and European stocks actually not that fussed, while currency markets absorbed it with aplomb. The USD remains somewhat weak against the majors although Euro didn’t fly as high as expected, with the Australian dollar firming above the 69 cent level. Bond markets saw more roundtripping of yields with 10 year Treasuries retracing back below the 3% level as US interest rate futures still imply a near 80bps rate rise at the next Fed meeting. Commodity prices were still volatile with Brent crude falling back to the $100USD per barrel level before recovering while copper and gold both lifted, although the latter did roundtrip violently below the $1700USD per ounce level.

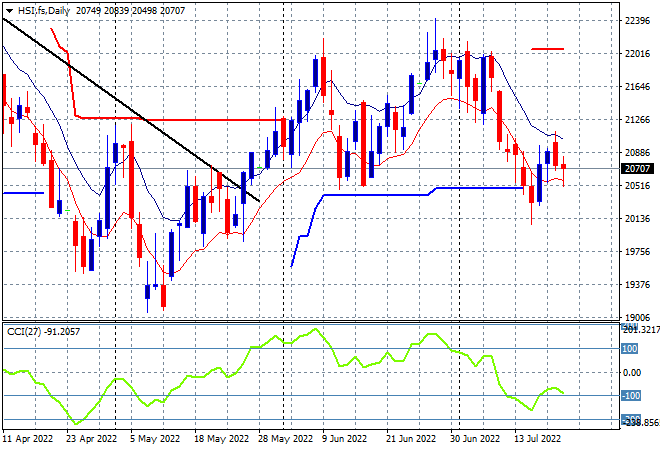

Looking at share markets in Asia from yesterday’s session, where mainland Chinese share markets tried to clawback their early morning losses but slumped going into the close with the Shanghai Composite finishing down 1% to 3272 points while the Hang Seng Index has retreated further to lose 1.5%, closing at 20574 points. Sentiment continues to wane on the daily chart with considerable overhead resistance and daily momentum readings remaining oversold as the previous swing play reverts back to the downtrend:

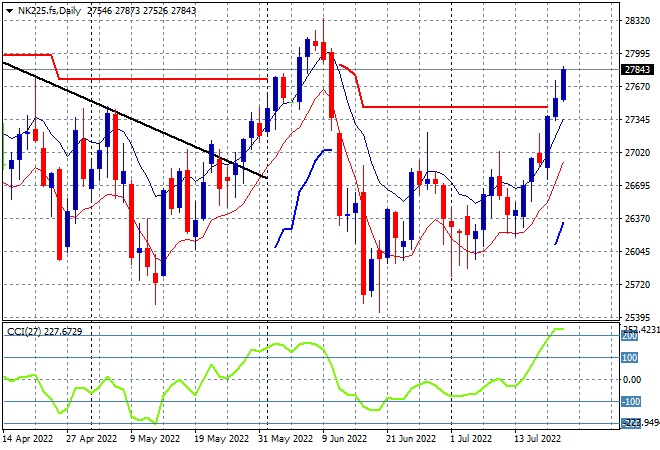

Japanese stock markets continued their surge, with the Nikkei 225 up 0.4% to 27803 points. The daily chart is suggesting this breakout to continue despite a rise in Yen overnight on the ECB rate hike, with resistance at the 27000 point area now turning into short term support as daily momentum remains nicely overbought. Price has made a new weekly high, which should support further upside here as the better lead from Wall Street should help in the short term: