Another turbulent night for overseas stock markets with some measure of calm from some Fed board members as the possibility of a big 100bps rate rise at the next Fed meeting was played down, despite the big inflation readings. Wall Street wobbled nonetheless, not helped by poorer than expected corporate earnings while European stocks fell sharply as Italy goes Australian on replacing prime ministers again. The USD lead the way against everything undollar with Euro pushed below parity briefly while the Australian dollar was also pushed into the 66’s before a small rebond later in the session. Bond markets jumped around again with more roundtripping in yields as US interest rate futures still imply more than 200bps in rate rises this year. Commodity prices are still volatile with Brent falling more than 5% before recovering back to just below the $100USD per barrel level while copper slid slightly lower as gold made a new daily low again, almost falling below the $1700USD per ounce level.

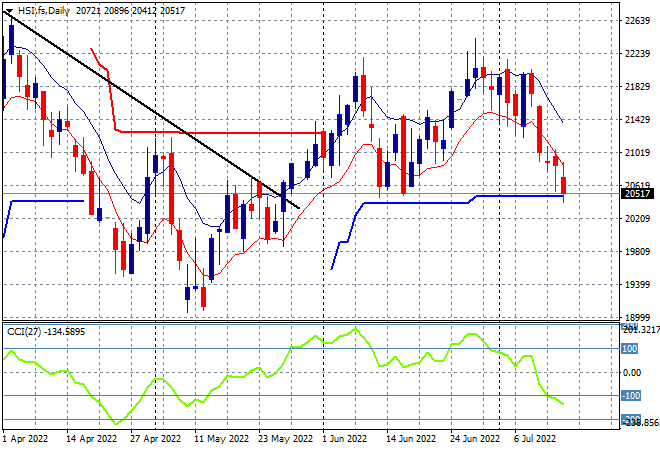

Looking at share markets in Asia from yesterday’s session, where Chinese share markets remain somewhat with the Shanghai Composite finishing dead flat at 3281 points while the Hang Seng Index went down just 0.2%, closing at 20751 points. The daily chart continues to firm the 22000 point level as considerable resistance that still keeps this market locked in place as price retraces back to the early June lows around the 20600 point area. Watch daily momentum readings that are now oversold carefully for signs of a follow through below ATR support at 20000 points proper:

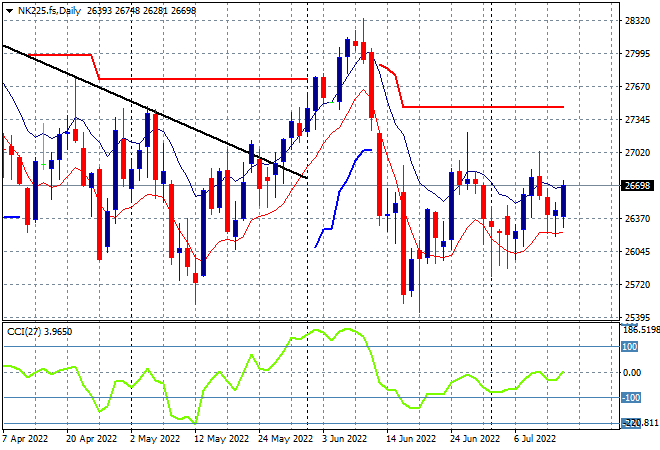

Japanese stock markets were again the strongest in the region, with the Nikkei 225 index closing 0.6% higher at 26643 points. Risk sentiment on the daily chart however is continuing to show stiff resistance at the 27000 point area with daily momentum still unable to get out of its negative funk. While price is coming close to making a new weekly high, I’m still looking for an attempt to break support at the 26000 point level proper next: