The latest US inflation print has come in very hot indeed, with a 9% reading that has spiked concerns that the Fed will raise rates even more aggressively than currently planned, with the Canadian central bank taking the cue, raising rates a full 100 bps overnight. Wall Street continued to fall amid growing hesitation on risk taking alongside European stocks with volatility in currencies expected around the inflation print that still has the USD leading the way against, well everything. Euro remains stuck at parity while the Australian dollar was basically unchanged at its two year low. Bond markets jumped around as the yield curve continued to invert with US interest rate futures moving higher with a 90bps rise expected at the next Fed meeting. Commodity prices are still volatile with Brent crude off slightly while copper continued to fall and gold range trading with wide intrasession volatility that saw it drop below the $1700USD per ounce level before recovering, somewhat.

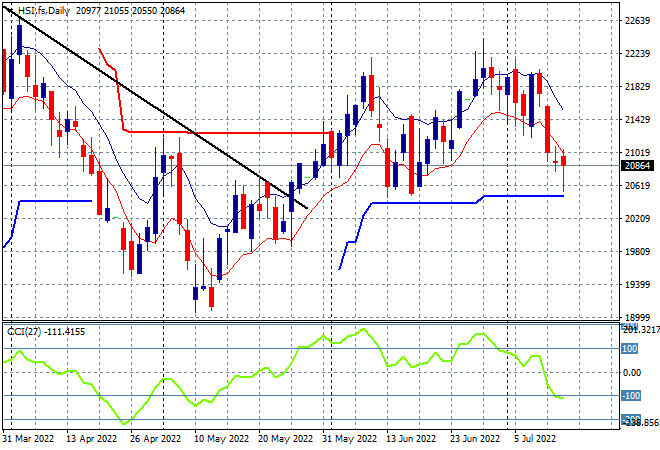

Looking at share markets in Asia from yesterday’s session, where Chinese share markets were somewhat mixed with the Shanghai Composite closing up just 2 points to 3284 while the Hang Seng Index nearly put in a scratch session before closing 0.2% lower at 20797 points. The daily chart continues to firm the 22000 point level as considerable resistance that still keeps this market locked in place as price retraces back to the early June lows around the 20600 point area. Watch daily momentum readings that are now oversold carefully for signs of a follow through below ATR support at 20000 points proper:

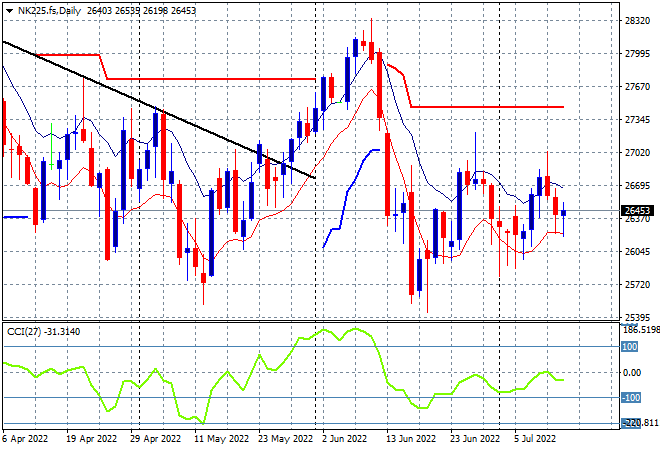

Japanese stock markets were the strongest in the region, with the Nikkei 225 index closing 0.5% higher at 26478 points. Risk sentiment on the daily chart however, is continuing to show stiff resistance at the 27000 point area with daily momentum still unable to get out of its negative funk. I’m still looking for an attempt to break support at the 26000 point level proper next: