Wall Street continues to fall amid growing inflation concerns as traders await the latest US data tonight with German data beforehand possibly giving the beleagured Euro a legup. The union currency is stuck at parity with the ever strong USD, with the near 20 year high in the USD Index holding as the Australian dollar remains at a new two year low despite a late blip in the session. Bond markets saw range trading in yields as the inflation print weighs, with 10 year Treasuries still below the 3% level, with no change in interest rate futures which continue to firm up a 75bps rise at the next Fed meeting. Commodity prices however shot higher in volatility with oil prices slumping more than 6% lower, with copper down 3%, iron ore off by 5% and gold still not catching any breaks as it makes another new daily low price below the $1730USD per ounce level.

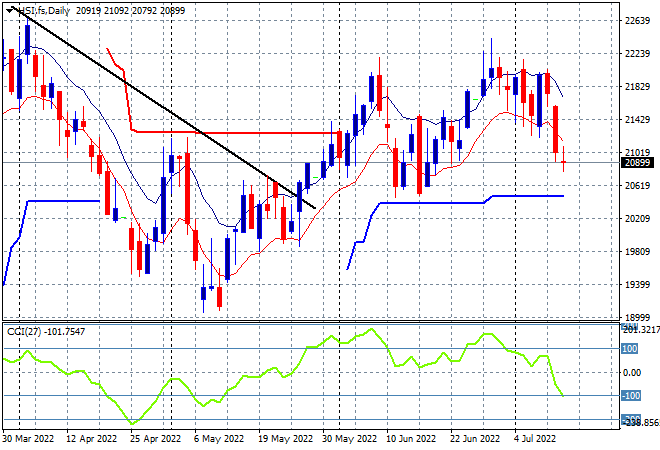

Looking at share markets in Asia from yesterday’s session, where Chinese share markets looked shaky at the open before retracing sharply going into the close with the Shanghai Composite finishing down 0.9% to 3281 points while the Hang Seng Index was off by 1.4%, closing at 20844 points. The daily chart continues to prove the 22000 point level as considerable resistance that has kept this market in check for sometime now with this steep rollover likely to see price retrace back to the early June lows around the 20600 point area next, so watch daily momentum readings that are now oversold:

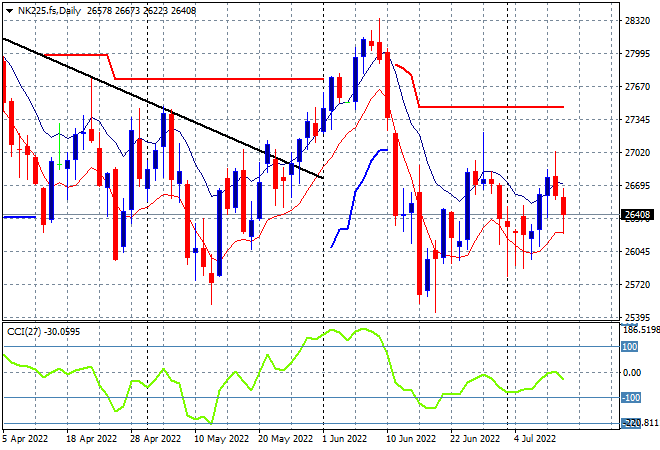

Japanese stock markets caught up to the risk off mood, with the Nikkei 225 index closing 1.8% lower at 26336 points. Risk sentiment on the daily chart is continuing to show stiff resistance at the 27000 point area with daily momentum still unable to get out of its negative funk. I’m looking for an attempt to break support at the 26000 point level proper next: