Wall Street stalled and then stumbled overnight with more concerns mounting about aggressive rate rises by central banks. A key sign of that is the near 20 year high in the USD Index, with parity almost achieved against Euro while the Australian dollar was pushed down strongly below the 68 handle for a new two year low. Bond markets saw a retracement in yields with 10 year Treasuries pushed back down to the 3% level, with no change in interest rate futures which continue to firm up at least a 75bps rise at the next Fed meeting. Commodity prices are pulling back in volatility with oil prices down slightly, with copper and gold pulled back around 0.5% each, the latter on the ropes at the $1730USD per ounce level.

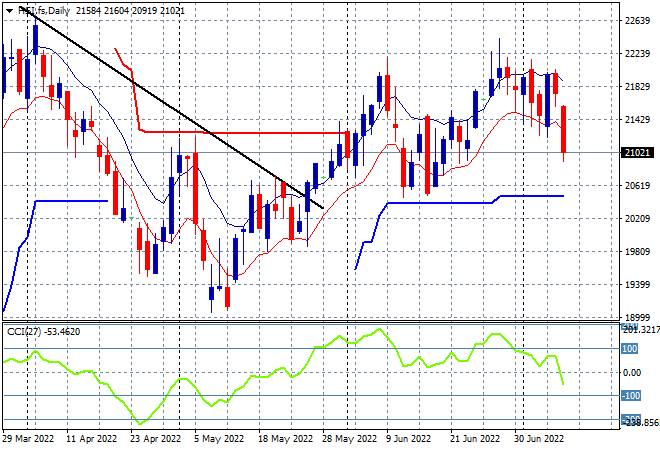

Looking at share markets in Asia from yesterday’s session, where mainland Chinese share markets started lower at the open and continued to retrace sharply with the Shanghai Composite closing 1.2% lower at 3313 points while the Hang Seng Index is slumping even faster, down 3% to 21085 points. The daily chart was showing the 22000 point level as considerable resistance that has kept this market in check for sometime now. This steep rollover could see price retrace back to the early June lows around the 20600 point area next, so watch daily momentum readings:

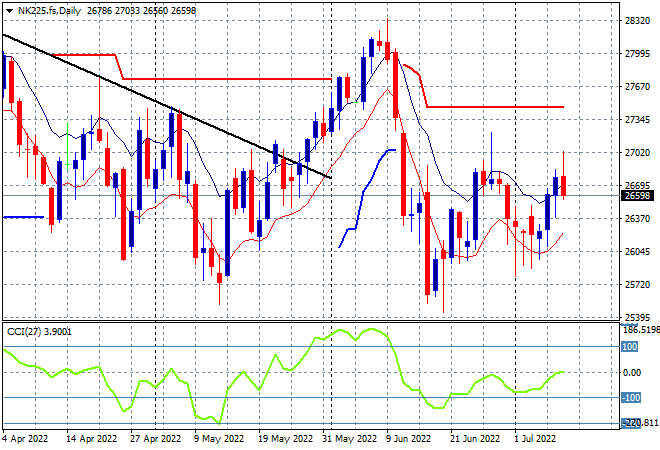

Japanese stock markets however bounced back the strongest, with the Nikkei 225 index closing 1.1% higher at 26812 points. Risk sentiment on the daily futures chart was looking to reverse here after this solid session to start the trading week but resistance continues to build around the 27000 point area with daily momentum still on the negative side: