Some hawkish minutes from the latest FOMC meeting and the latest ISM services PMI assuaged recession fears overnight after a wobbly start to the trading week, with Wall Street gaining modestly, while European stocks bounced back after a steep selloff previously. The USD continued to rise however against all the undollars, with Euro approaching parity and Pound Sterling at near decade lows, while the Australian dollar remains depressed below the 68 handle. Bond markets reversed sharply with 10 year Treasuries bouncing back to 2.9% on the minutes, with interest rate futures also pushing up, with expectations of a 70bps rise at the next Fed meeting. Commodity prices remain under pressure with oil down nearly 3%, copper down another 4% to almost make a two year low while gold fell another 1% or so, still crushed below the $1800USD per ounce level.

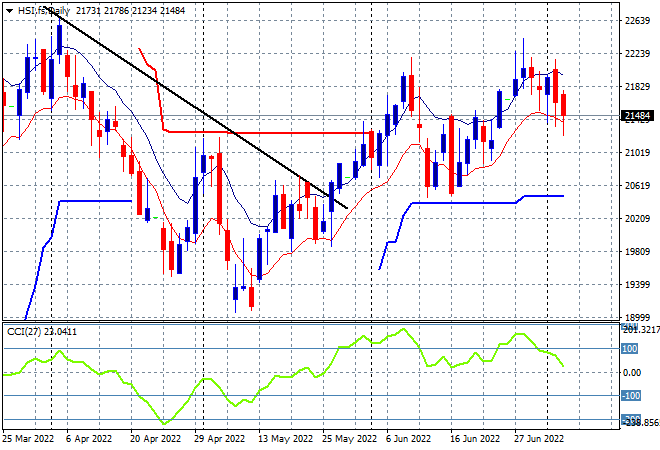

Looking at share markets in Asia from yesterday’s session, where Chinese share markets dropped sharply going into the close with the Shanghai Composite down 1.4% to 3355 points while the Hang Seng Index was off by more than 2% at one stage, eventually closed 1.2% lower at 21586 points. The daily chart is now showing a potential rollover here as price action rejects the previous highs at the 22000 point level as considerable resistance is still keeping this market in check, with session highs failing to match the previous false breakout tops. Momentum continues to rollover here:

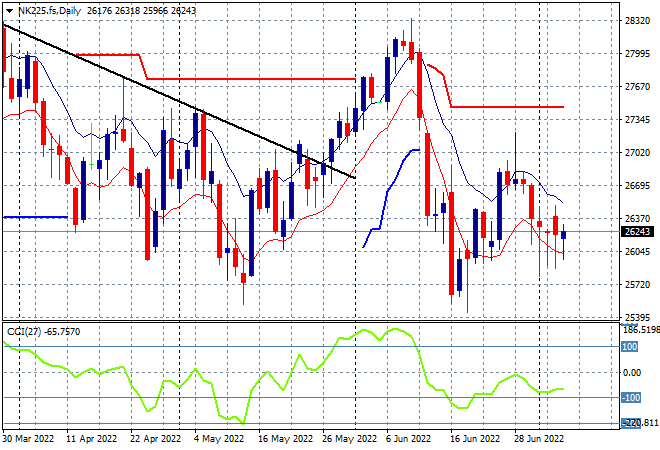

Japanese stock markets are also selling off, with the Nikkei 225 index closing some 1.2% lower at 26107 points. Risk sentiment on the daily futures chart remains very poor but a small up session today is still unlikely to see any move above the high moving average. Daily momentum is building on the negative side as this looks more and more like a dead cat bounce: