Risk sentiment stabilised overnight only because of a lack of economic catalysts and closed markets on Wall Street due to the long weekend. European stocks struggled without direction while the USD was mixed against the undollars, with Euro and Pound Sterling lifting slightly, while the Australian dollar stalled out after trying to bounce back from its slamming below the 68 handle on Friday night. Bond markets were subdued due to the lack of volume, with 10 year Treasury futures indicating a 2.9% level on the reopen tonight, with interest rate futures still firming 170 bps suggested rate rises by the Fed this year. Commodity prices were also mixed, with oil prices up more than 3%, copper down to a yearly low while gold tried to stabilise above the $1800USD per ounce level but looks under stress.

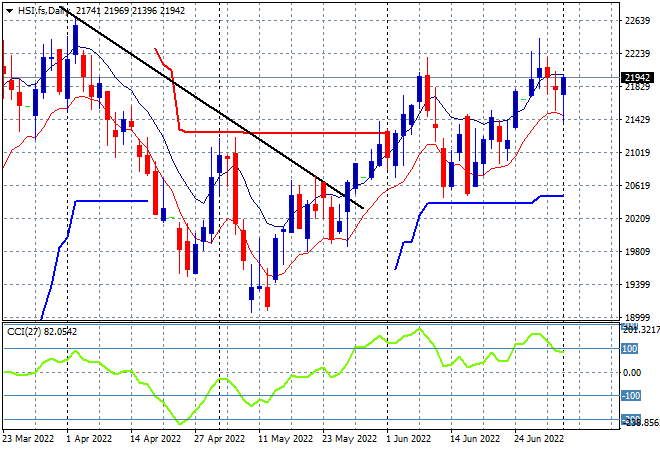

Looking at share markets in Asia from yesterday’s session, where mainland Chinese share markets lifted somewhat, with the Shanghai Composite up nearly 0.5% to crossover 3400 points while the Hang Seng Index went slightly backwards, down 0.1% to 21830 points. The daily chart is still showing a desire to breakout above the previous highs at the 22000 point level but considerable resistance is keeping this market in check, with session highs failing to match the previous false breakout tops. Momentum continues to rollover here, so be cautious of low volatility that could beget higher downside volatility soon:

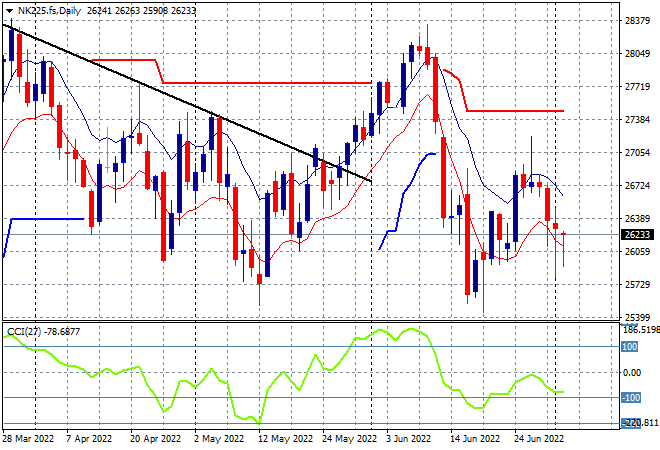

Japanese stock markets however are not minding the stronger Yen, with the Nikkei 225 index up nearly 0.8% at 26150 points. Risk sentiment on the daily futures chart however still shows possible further downside with price action still unable to make any move above the high moving average. Daily momentum is building on the negative side as this looks more and more like a dead cat bounce, although a mild uptick is probable for today’s session: