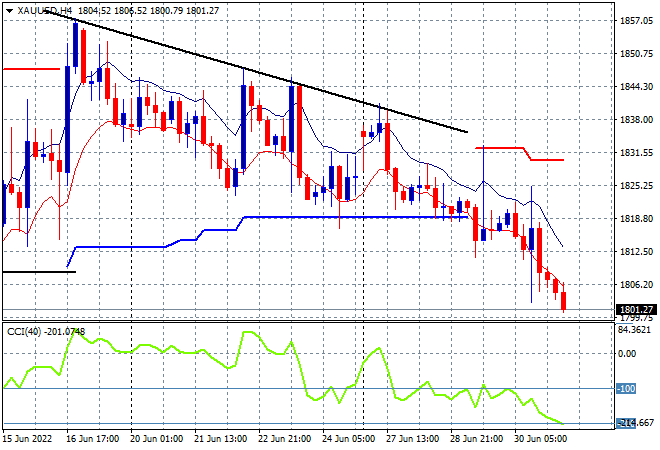

Yet another sea of red across Asian share markets although mainland Chinese and their Australian satellite bourses are looking to put in scratch sessions. The souring of risk sentiment on Wall Street is keeping all risk markets depressed with the defensive USD joining in with a stronger Yen as the Australian dollar gets smoked down to the 68 cent level. Oil prices are trying to stabilise with Brent crude retreating below the $109USD per barrel level. Meanwhile gold is now in rollover mode having broken key support levels as it prepares to breakdown below the $1800USD per ounce level:

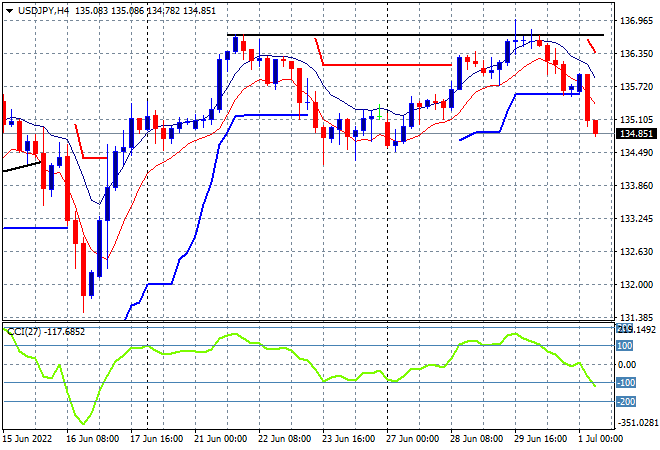

Mainland Chinese share markets are slipping slightly going into the close with the Shanghai Composite down nearly 0.3% to 3389 points while the Hang Seng Index is slowly slipping away into another falling session, down more than 0.6%, currently at 21859 points. Japanese stock markets however are not liking the stronger Yen, with the Nikkei 225 index more than 1.6% lower at 25937 points while the USDJPY pair has retraced sharply below the 135 handle, having rejected last weeks high and barreling in on a new weekly low:

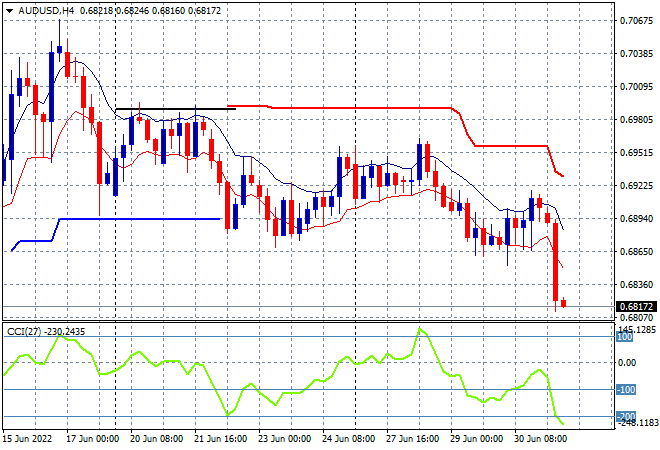

Australian stocks were able to escape the selling with the ASX200 looking set to finish 0.1% higher, currently at 6567 points. The Australian dollar was smacked down this afternoon with a sudden move towards the 68 handle for a new weekly low:

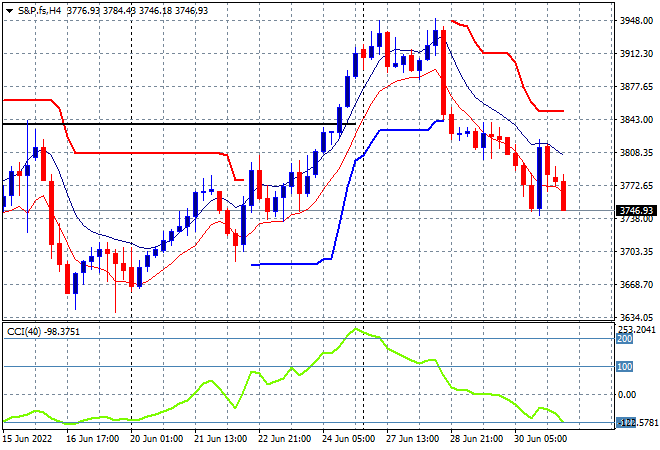

Eurostoxx and Wall Street futures are heading down sharply as we head into the European open, with the S&P500 four hourly futures chart showing price action ready to head towards the 3700 point level with momentum going into the oversold zone and ready to break lower:

The economic calendar finishes the week with two big releases, Euro-wide core inflation and the latest US ISM manufacturing print.