When somebody “proper” says it, it must be true. It is all coming sooner than Nomura says but at least it is finally saying it.

I might add that Nomura also sees a global recession commencing this year and particularly large busts across DMs.

As for how bad it gets in Australia and when the RBA pivots, that is up to Albo’s cowards. If it acts on energy prices then the recession will be mild and short. If it doesn’t then it will be very nasty and very long.

—

Australia: sliding into recession

We expect more aggressive monetary tightening in 2022 to lead to recession in 2023, and eventual rate cuts. We have cut our 2023 GDP growth forecasts materially.

We have made a material downgrade to our 2023 growth outlook, and now see Australiasliding into recession next year, as a more aggressive and front-loaded rate hike cycle progressively bites, exposing Australia’s Achilles heel, a highly leveraged consumer and sky-high property prices. A weaker global growth outlook, and our expectation for relatively less fiscal support in 2023 form part of our view. We expect higher inflation to be somewhat “sticky”, limiting the RBA’s capacity to immediately respond, but we have pencilled in three 25bp rate cuts in late-2023, from a 3.1% cash rate peak by end-2022. Our “boom-bust” view is sharply out-of-consensus, but we think it is fair, and see risk as being evenly balanced around our central case.

A major growth downgrade: recession ahead

The economy has rebounded strongly from the initial COVID-19 crisis. The level of real GDP is 4.5pp above its pre-COVID level, unemployment is at a near 50-year low, cap useis very high and firms no longer appear hesitant to raise prices. Combined with difficult to predict global forces (China lockdowns, war in Ukraine and surging oil and gas prices), inflation has surged, after a slow start.

The RBA has clearly kept the punchbowl at the party for too long, and has now begun to tighten, at pace. However, with strong local momentum, we think an aggressive move into restrictive territory will be required to tame inflation. We think this will stun consumers, who heard a message that rates were unlikely to rise until 2024, and trigger a sharp downturn in the housing market and consumer spending, with boom turning to bust.

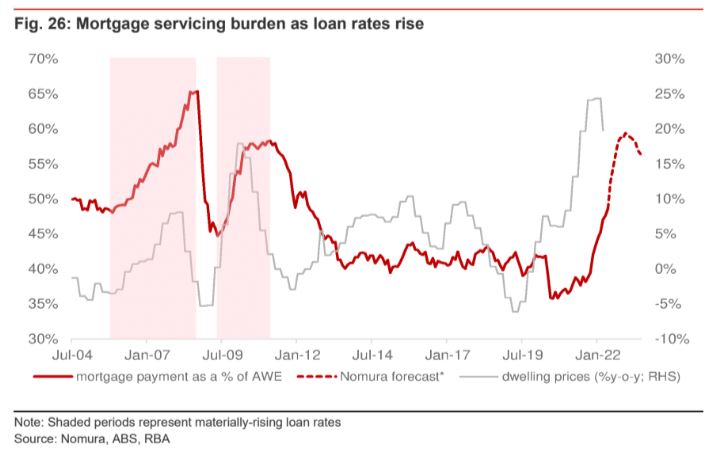

Housing affordability has already declined notably, and we see more pain ahead. The average loan rate has risen by around 1.7pp, and we think a further approximate 1.4ppmove is in store. Incorporating other assumptions – for 3.5-4.0% wage growth, an approximate 10% decline in loan size (and dwelling prices) – we think affordability will decline to levels seen around 2008 and 2011, periods that also saw dwelling prices fall. Leverage works well when rates are low and asset valuations are rising, but the opposite also holds.

Around 40% of current mortgages are fixed rate loans – this is above the longer-term average (~15%), so the impact of higher mortgage rates may take some time to flow through. Still, the average fixed rate loan in Australia has a short maturity (typically 2-3years) and around 75% of these fixed rate loans will reset at substantially higher rates bythe end of 2023. As a guide, 2-3 year fixed rate loans through the YCC period carried loan rates as low as 2%, and these rates have already risen to around 5.0-5.5%. We expectfloating (variable) loan rates to rise in lock-step with future moves in the cash rate. Variable rate loans have risen by 0.75% to date, and in view of our RBA forecasts, weexpect to see a further 225bp increase in these rates over the next six months.

Australian banks are required to assess loan affordability by adding 300bp to a loan rate(previously 250bp), so “on paper” most borrowers should be able to weather this increase in rates. Still, when it comes to housing, it is what happens at the margin that is most important, and we think some borrowers will get into difficulty, triggering some forced selling.

Recession watch

The latest high frequency and survey data highlight that consumer sentiment has already fallen notably, PMIs have moved lower and dwelling prices are now falling, led by declines in Sydney prices. Weakness is not uniform; in particular forward orders and employment indicators remain strong. However, rates have only recently started to move higher, andwe do not expect the recession to commence until early 2023. Overall, we judge that afew cracks have started to appear, and we think our recession thesis is on track.

The policy response

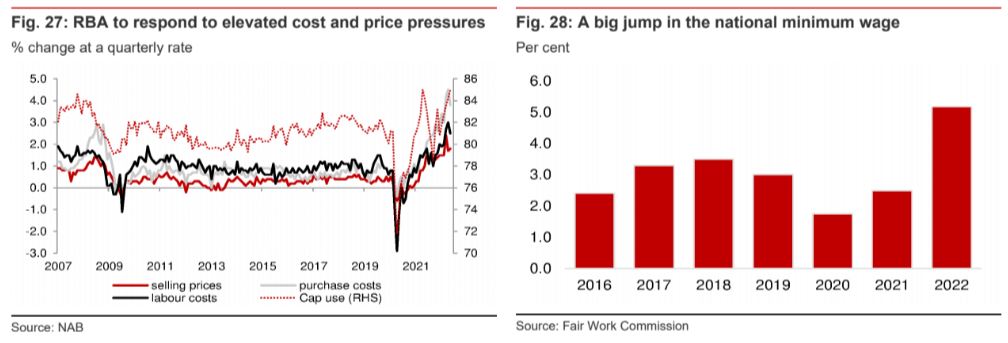

Uncomfortably high and rising inflation pressures, and a complete shift in the “inflation psychology” are likely to drive an aggressive and front-loaded RBA policy response. Inflation pressures are coming from domestic as well as global sources, and local inflation pressures could continue for a time, even if, and as, global supply chain problems ease. A large jump in minimum wages could add to RBA concerns about “second-round” effects from high prices too.

The RBA governor has conceded there is a “narrow path” to tame inflation without inflicting economic pain and inducing recession. The stakes are high, but we think the RBA now has little choice but to walk down this path.

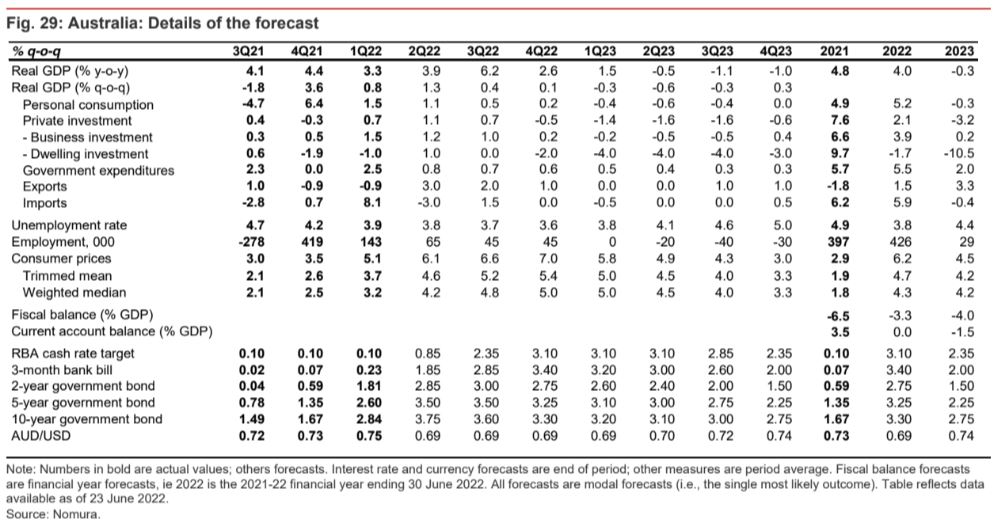

We expect the RBA to deliver three further, and consecutive 50bp rate hikes (July, August, September), taking the cash rate to a roughly neutral level of 2.35%. From there, we think the pace of hiking may moderate, as it moves into restrictive territory; we expect three further, and final, 25bp hikes (October, November, December), taking the cash rate to a peak of 3.1% by end 2022. After a slow start, we think this constitutes a surprising and aggressive response, and we think it will shock consumers.

As recession becomes clear (to be confirmed by Q2 2023 GDP data released in September next year) and inflation gradually eases, we think we could see easing commence, and pencil in three 25bp rate cuts in late 2023 (September, November, December), with the cash rate ending 2023 at 2.35%. On the fiscal side, we expect only limited support, targetted at helping lower income cohorts cope with higher prices. The new Labor government is inheriting high post-COVID debt levels, and continuing budget deficits, and we think it will wish to push back against notions that it is a less prudent economic manager. Overall, we expect public final demand to expand at a subtrend pacein 2023, notably weaker than in 2022.

Our revised forecasts

We have trimmed our 2022 GDP growth forecast by 0.4pp, and have lowered our 2023GDP growth forecast by a striking 3pp. We expect negative growth to be recorded over three quarters (Q1-Q3 of 2023) but note that growth is forecast to be very weak on either side of this period.

Within this, we have cut our consumer spending forecasts sharply, reflecting our expectations for the housing market and interest rates. We have also trimmed our already-negative dwelling construction forecasts and lowered our business investment numbers too. Weaker import growth, with lower domestic demand, offers a partial offset,but with weaker global growth likely, we have cut our export forecasts as well.

With weaker growth, we now expect the unemployment rate to end 2022 at 3.6% (was 3.4%), and to rise to around 5.0% by end-2023 (was 3.3%). Employment typically lags the cycle, and we expect a notable rise in unemployment, commencing in Q1 next year.

We have not touched our CPI inflation forecasts for 2022, and still forecast an increase in headline CPI inflation to around 7% y-o-y, noting we made this call before the governor did so, on 14 June. However, we have trimmed our 2023 CPI inflation forecasts, reflecting our revised growth and labour market forecasts.

Balanced risks around our new central case

There are certainly upside risks: 1) China could “come to the rescue” again (as it did during the GFC) with larger-than-expected stimulus and stronger-than-forecast growth; 2)AUD could fall sharply and perform a helpful “shock absorber” role, as it has in the past; and 3) the RBA and Fed could hike by less than we expect.

However, we think that this is balanced by downside risks: 1) we are wary about how financial assets might perform if global central banks are true to their word and aggressively pursue their “unconditional commitment” to fight inflation; 2) commodity prices could fall sharply if global growth plunges, and 3) the housing downturn could be worse than in our base case.On the latter, we are particularly mindful of potential downside and non-linear “amplifier effects”, as Australian consumers are carrying very high debt levels by global standards.An inflated balance sheet is manageable, even desirable, when rates are low and asset prices are rising, but the inverse is also true. This could deepen the recession and make it last even longer than the US recession, in view of the very high debt levels being carried by Australian consumers. In this scenario, banks could tighten lending standards as loan collateral deteriorates and the current low level of defaults starts to rise. This could result in a larger hit to consumption too.