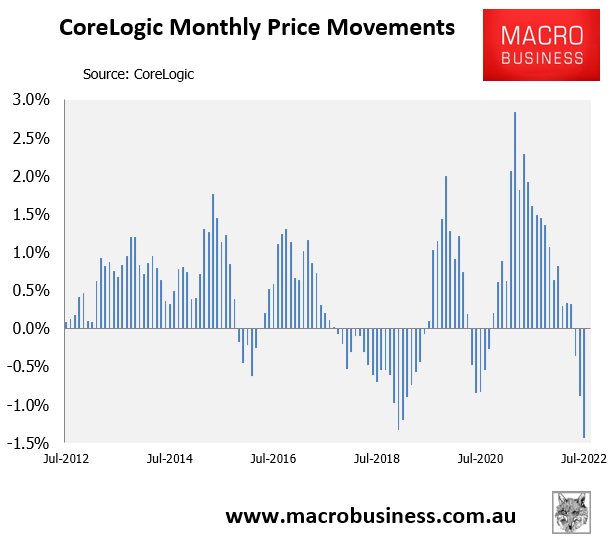

CoreLogic has released its daily dwelling value results for July, which track price changes across Australia’s five major capital cities.

At the 5-city aggregate level, dwelling values fell by 1.44% in July, which was is biggest monthly price decline since January 1983:

Biggest monthly price decline since 1983.

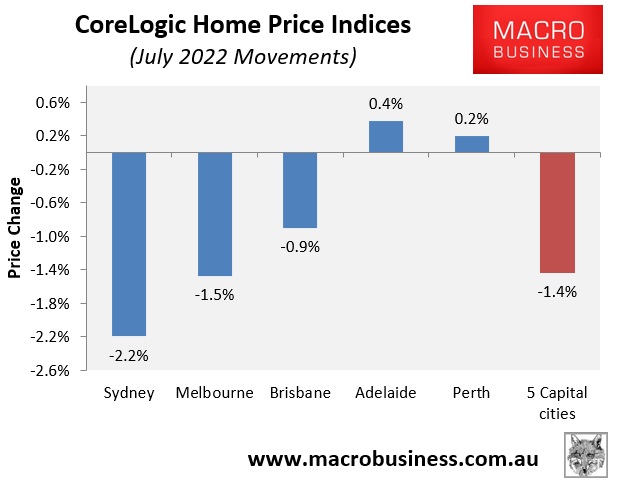

The collapse in prices was driven by Sydney (-2.2%) and Melbourne (-1.5%), with Brisbane (-0.9%) also recording a solid monthly fall:

Sydney and Melbourne lead the price bust.

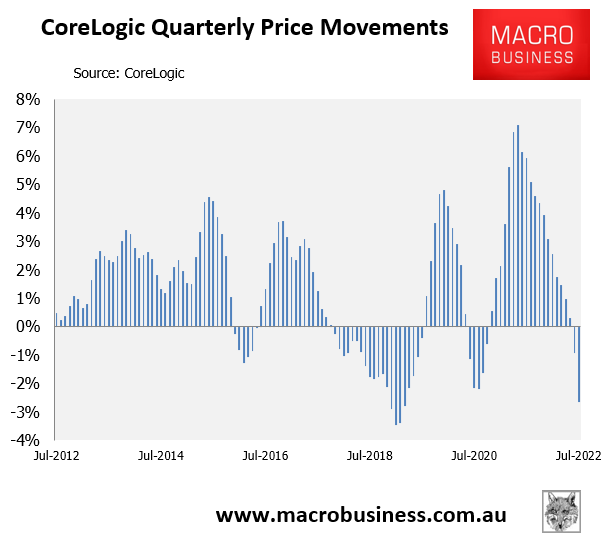

Across the July quarter, dwelling values fell by 2.7%, which was the largest fall since March 2019. But it’s the steepness of the decline that is particularly alarming:

Big acceleration in price falls.

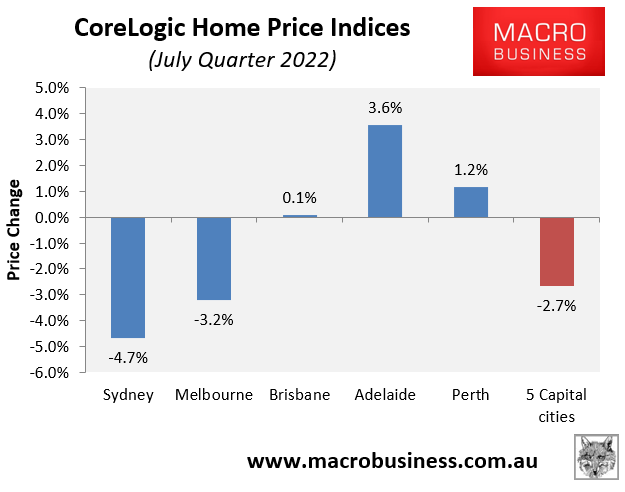

Again, the quarterly decline in values at the 5-city level was driven by heavy losses across Sydney (-4.7%) and Melbourne (-3.2%):

Heavy quarterly falls across Sydney and Melbourne.

The sharp fall in Australian dwelling values has obviously been driven by the Reserve Bank of Australia’s (RBA) aggressive monetary tightening, which saw three consecutive official cash rate (OCR) hikes in May (0.25%), June (0.5%) and July (0.5%), with economists and markets predicting another 0.5% hike on Tuesday.

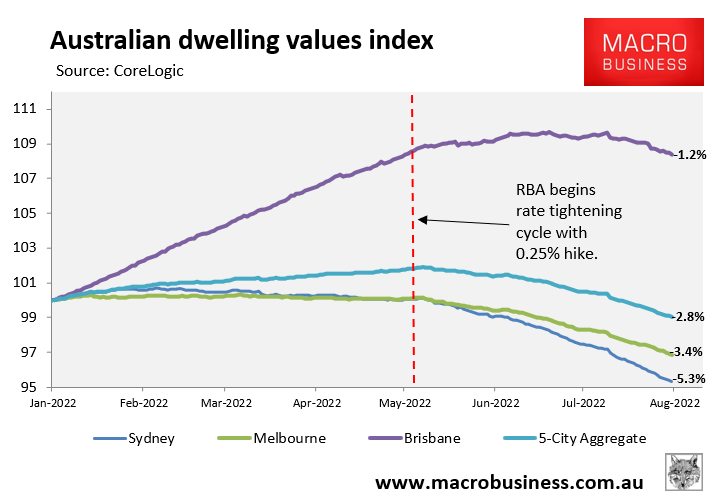

You can see in the next chart the sharp decline in dwelling values after the RBA began lifting rates in early May:

Dwelling values dived after the RBA began hiking rates.

Sydney dwelling values have so far declined by 5.3% from its February peak, whereas Melbourne’s are down 3.4%. Brisbane values started declining in late June, but are already down 1.2%. At the 5-city aggregate, dwelling values have so far fallen 2.8% from their peak.

With economists and the futures market tipping an OCR of around 3% by the end of the year – a sharp increase from 1.35% currently – it’s easy to see why Australia’s housing market is facing its biggest price crash in living memory.