A year or more ago I labeled Evergrande China’s Lehman moment. The year since has been a relentless crash in Chinese dwelling construction: equity, sales and starts.

It was obvious from the beginning that it would eventually end up as a problem for the banking system. That time has come.

It is the nature of the banking problem that is now the most noteworthy feature. Like the great US housing market crash that destroyed Lehman Brothers, it is home buyers who are about to end the system that has pumped the economy dry for a decade.

They are doing so using the same method, too. In the US it became known as “jingle mail”. The process of bankrupted or over-mortgaged mortgage holders sending the keys back to lenders in the post.

Advertisement

The Chinese version is typically a little more collective:

More and more home buyers across China refuse to pay mortgages as the properties they purchased have been left unfinished amid the liquidity crunch in the real estate sector.

As of July 12, home buyers of more than 100 property projects across provinces including Hubei, Henan, Shandong, Jiangxi, Jiangsu, Hunan and Shaanxi had issued statements saying that they refuse to pay mortgage loans as the properties they purchased have been left unfinished, according to a report to The 21st Century Business Herald.

Of the projects, more than 30 are in central China’s Henan province and many are in the provinces of Hunan and Hubei, according to a report by Caixin.

The construction of the projects had been in suspension due to the developers’ liquidity difficulties, which means the home deliveries would be delayed, forcing them to take actions to safeguard their legitimate rights, the homebuyers said.

The developers of the property projects involved include China Evergrande Group, Sinic Holdings, Greenland Holdings, Sunac China, Kangqiao Group, Xinyuan Group, Sichuan Languang Development Co, Zensun Group and Myhome Real Estate Development Group, etc.

For instance, homebuyers of a project developed by property developer Times China in Wuhan, capital city of Central China’s Hubei province, said in a joint statement on July 7 that they had made several attempts to communicate with the developer and safeguard their legitimate rights, but failed to make any progress in the issue and the construction remained in suspension.

“If the construction of the project does not resume by August 1, we will all stop paying mortgages,” the statement reads.

Refusal to pay mortgages in response to delayed deliveries reflects the lack of effective financial supervision of related banks, especially on pre-sales funds, which may have been misappropriated to meet property developers’ debt payments or provide operating funds, they noted.

In their joint statements, the buyers accused banks of granting home mortgage loans before the the main structure of the properties in question get completed, which violated related regulations; transferring funds from mortgages to unregulated accounts; failing to ensure security of pre-sales proceeds, etc.

Most Chinese property developers are heavily dependent on pre-sales proceeds to secure their cash flows and the country has introduced regulations on the use of the proceeds in order to ensure property construction and home deliveries.

As early as 2003, China introduced related rules, under which “home mortgage loans can only to granted to home buyers when the main structure of the properties in question is completed” and “when the funds from mortgage loans is misappropriated for purposes other than property construction, the banks have obligations to bring back the funds.”

Under the rules adopted in 2010, all pre-sales proceeds should be put in custodial accounts and regulatory bodies are responsible for ensuring that the pre-sale funds are used for property construction.

Yan Yuejin, research director of the Shanghai-based E-House China R&D Institute, said that “the flows of the pre-sales proceeds of the projects in question are murky and the regulation on the funds were inadequate, which means, to some extend, banks should be held accountable.”

Notably, in February this year, it’s reported that China was drafting nationwide rules to make it easier for property developers to access funds from sales still held in escrow accounts in a move to ease a severe cash crunch in the sector.

In April, China’s Politburo, the top decision-making body of the ruling Communist Party, expressed supports for local governments’ move to adjust property policies to stablize the housing market and, for the first time ever, pledged to optimize regulations on property developers’ pre-sale proceeds.

Earlier data has shown that, as of the end of 2021, delayed deliveries in 24 major Chinese cities made up 10% of the total in terms of sales areas, according to real estate consultancy CRIC China.

In the most pessimistic scenario, delayed deliveries would account for 5% -10% of the nation’s total, according to CRIC data, which put the scale of potential mortgage defaults at 360 billion yuan to 730 billion yuan nationwide.

This would be a default rate of 0.9-1.9% of the nation’s total outstanding mortgage loans over the first quarter of 2021.

The results are in. Chinese developer debt has been frozen for a year. But now it’s the banks’ turn:

Advertisement

While it’s not clear how many homebuyers are snubbing repayments, the delayed projects make up about 1% of China’s total mortgage balance, according to Jefferies. Should every buyer default, that would lead to a 388 billion yuan ($58 billion) increase in non-performing loans, Chen said.

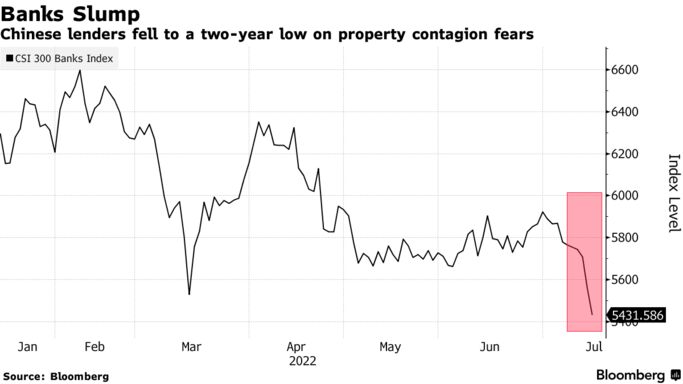

Some major Chinese banks rushed to respond during trading hours on Thursday as the CSI 300 Banks Index fell as much as 3.3%. State-owned Agricultural Bank of China Ltd. said it held 660 million yuan of overdue loans on unfinished homes, while smaller rival Industrial Bank Co. said 1.6 billion yuan of mortgages were impacted, of which 384 million yuan have become delinquent. China Construction Bank Corp., the nation’s largest mortgage lender, said overall risks are controllable as its exposure to delayed projects is small.

Chinese policymakers face a dilemma in dealing with the problem, according to Chen at Jefferies. On one hand, easing lending rules to favor homebuyers waiting for their properties to be completed may encourage more delinquencies. On the other, social stability remains the top priority for the government. Avoiding a deeper property crisis that sends shockwaves across markets and banks is a political necessity ahead of this year’s Communist Party Congress.

Any move to tighten mortgage lending would put further pressure on already weak home sales as potential buyers balk at higher borrowing costs and longer loan approvals. The outlook for sales — which some say recently bottomed — is also being dimmed by a resurgence in Covid cases and potential restrictions.

…Nomura Holdings Inc. said the refusal to pay mortgages stems from the widespread practice in China of selling homes before they’re built. Confidence that projects will be completed has weakened as developers’ cash woes intensified.

“We are especially concerned about the financial impact of the homebuyers’ ‘stopping mortgage repayments’ movement,” Nomura economists led by Ting Lu wrote in a note on Wednesday. “China’s property downturn may finally adversely affect onshore financial institutions after hitting the offshore high-yield dollar bond market.”

Lu estimated that Chinese developers have only delivered around 60% of homes they presold between 2013 and 2020, while in those years China’s mortgage loans rose by 26.3 trillion yuan. GF Securities Co. expected that up to 2 trillion yuan of mortgages could be impacted by the boycott.

Like jingle mail before it, expect the strike to grow. There is no policy fix for this in current settings. The “Three Red Lines” policy that began the great correction by limiting developer leverage has shattered the counterparty trust between buyers and builders. The only way to fix this is to remove the policy.

But it is Xi Jinping’s signature reform in his new Chinese vision. And even if it is reversed, who is going to trust that it won’t be reimposed in a year?

Advertisement

Morgan Stanly sums it well. Beware “non-linearity”:

Mortgage delinquency is rising on pre-sold but halted projects.

We estimate 188mn sqm (1.7mn units) are at risk. We expect local governments will be urged to help completion, but a national bazooka solution remains difficult in near term. Nonlinearity is the key to watch.

What happened: Growing number of home buyers in dozens of Chinese cities are not making mortgage payments, according to Bloomberg. This is because construction of the housing units they bought is facing extended suspension, due to liquidity stress among developers.

What is the significance? Mortgages are widely considered a high-quality asset in view of strict lending standards and historically low delinquency rates, but while the banking industry has been relatively better insulated in the ongoing housing slowdown so far, the latest development suggests that it might not be immune, particularly if the slowdown continues to worsen.

What is the scope of mortgages “at risk”? Currently, mortgages at risk account for ~2% of the outstanding balance, according to our property team (link). The implications for social stability could be meaningful,as ~1.7mn households are likely affected.

What is the key downside risk? Non-linearity kicking in: Home-buyer confidence weakens further from a low starting point, leading to further deterioration in property sales. This may force more developers,even relatively strong ones today, to suspend unfinished projects, furthering the downtrend. In the meantime, housing prices may continue to fall, exacerbating the downward spiral.

Furthermore, the stress in the housing sector could spread to the broader economy,given the extensive inter-sector linkages, while being magnified by the financial system.

What is the potential policyresponse?

Damage control:Local governments will likely be called upon to mobilize resources on a by-project basis, possibly with the help of SOEs and LGFVs, to kick-start suspended projects, signaling to the public thathousing completion is the over-arching priority. SOE developers may be encouraged to conduct M&A activities, taking over stalled projects.

Reining in systemic risk beyond the near term: Policy makers will likely need to send a clear and strong signal that they stand ready to be the “rescuer of the last resort” to rein in systemic risks. Plausible moves include more meaningful demand stimulus, more explicit guarantees on quality developers, or (less likely) a TARP-like program.

The implications of this are profound:

There will not be a “sudden stop” in Chinese lending given the banks are publically owned. But this is now a balance sheet recession for property punters and debt revulsion will overtake banks on the demand side. Chinese banks are road kill.

As the Fed tightens, capital will flee China. CNY is going to fall much further.

An external crisis with Chinese characteristics is shaping as the event that ends Fed tightening. But first, it is going to wipe out commodities, especially bulks and metals.

The downside for EM equities and debt are obvious.

Anybody related to China should bend over and place their head firmly between their legs.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.