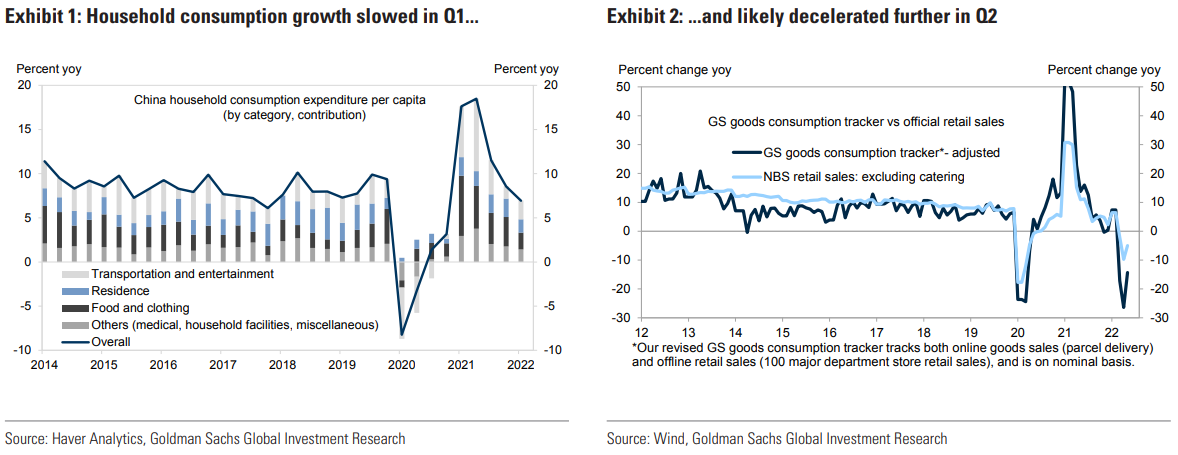

Goldman reports that Chinese household consumption slowed in Q1, and will very likely slow further in Q2. Given OMICRON is likely to rebound, and property sales will come off again, China’s economy is facing growing headwinds:

Sluggish consumption growth in Q1 and further weakening in Q2

According to the NBS household surveys, household consumption per capita grew 6.9% yoy in Q1 this year, slower than 8.6% yoy in Q4 2021. The deceleration of consumption growth appears relatively broad-based, with food and clothing consumption contributing the most to the deceleration. Going into Q2, the resurgence of Covid took a heavy toll on consumption growth – goods consumption indicators such as NBS goods retail sales and the GS goods consumption tracker (which captures large department store sales) fell further and showed double-digit year-over-year declines.

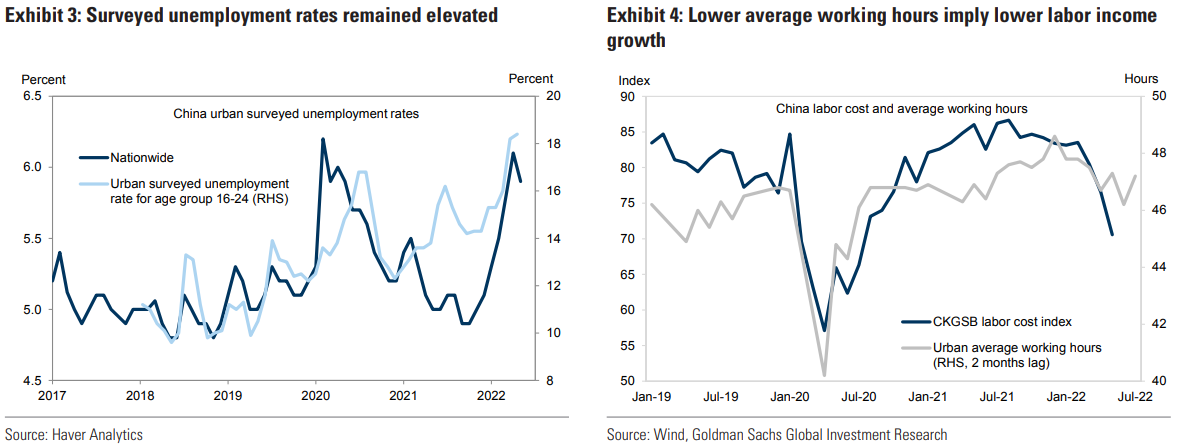

Labor market stress and slower households’ cash flow growth

Labor market stress increased in April with surveyed unemployment rates surging to close to record high levels. Surveyed unemployment rates moderated in May as activity growth rebounded. Despite the recent recovery, urban worker average working hours per week, which we found to be closely correlated with wage growth measures such as the Cheung Kong Graduate School of Business (CKGSB) Business Conditions Index (BCI) labor cost sub-index, showed that the labor market remained weak and suggested that wage growth might stay sluggish in the near term.