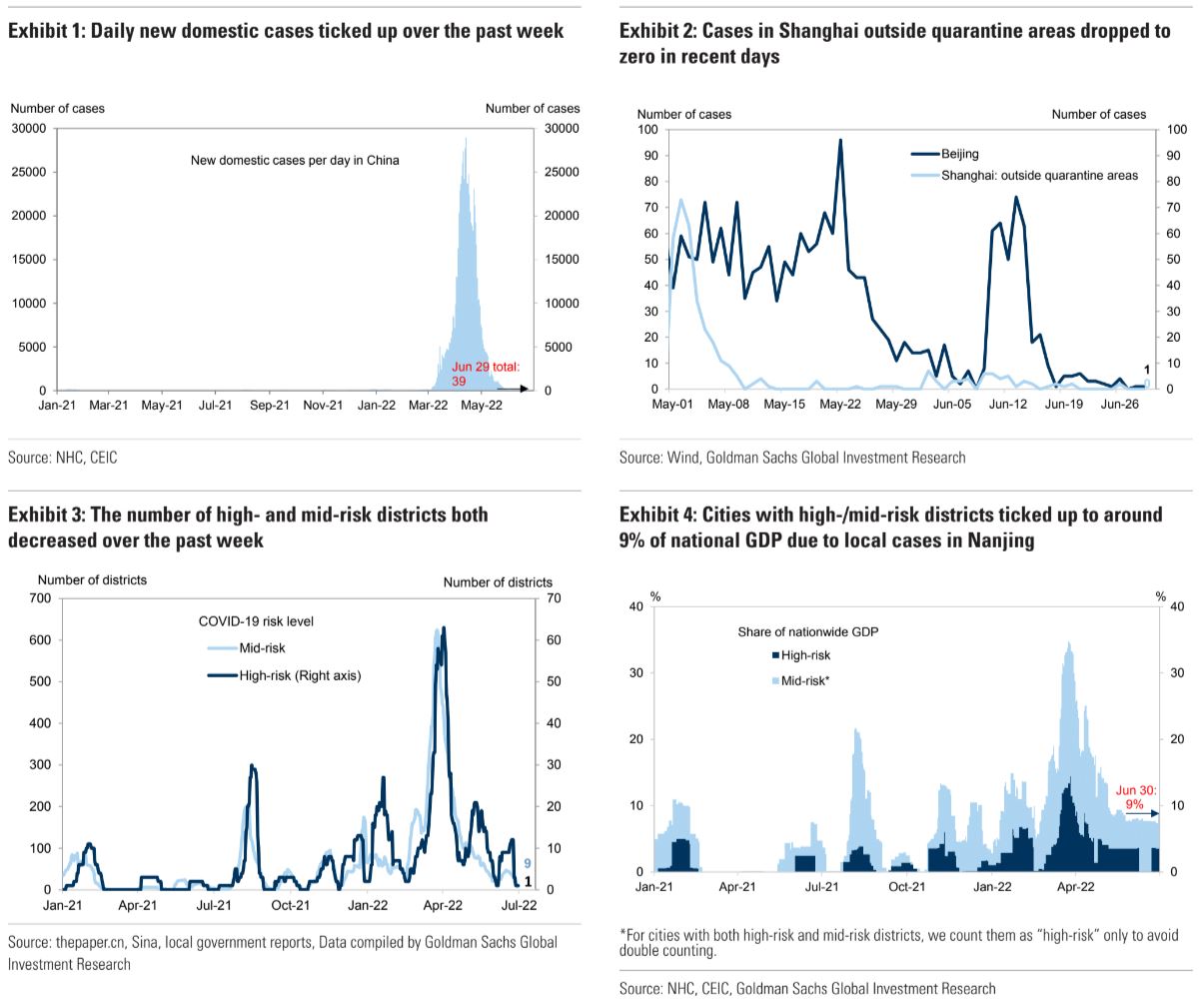

OMICRON has been imprisoned in Xinjiang:

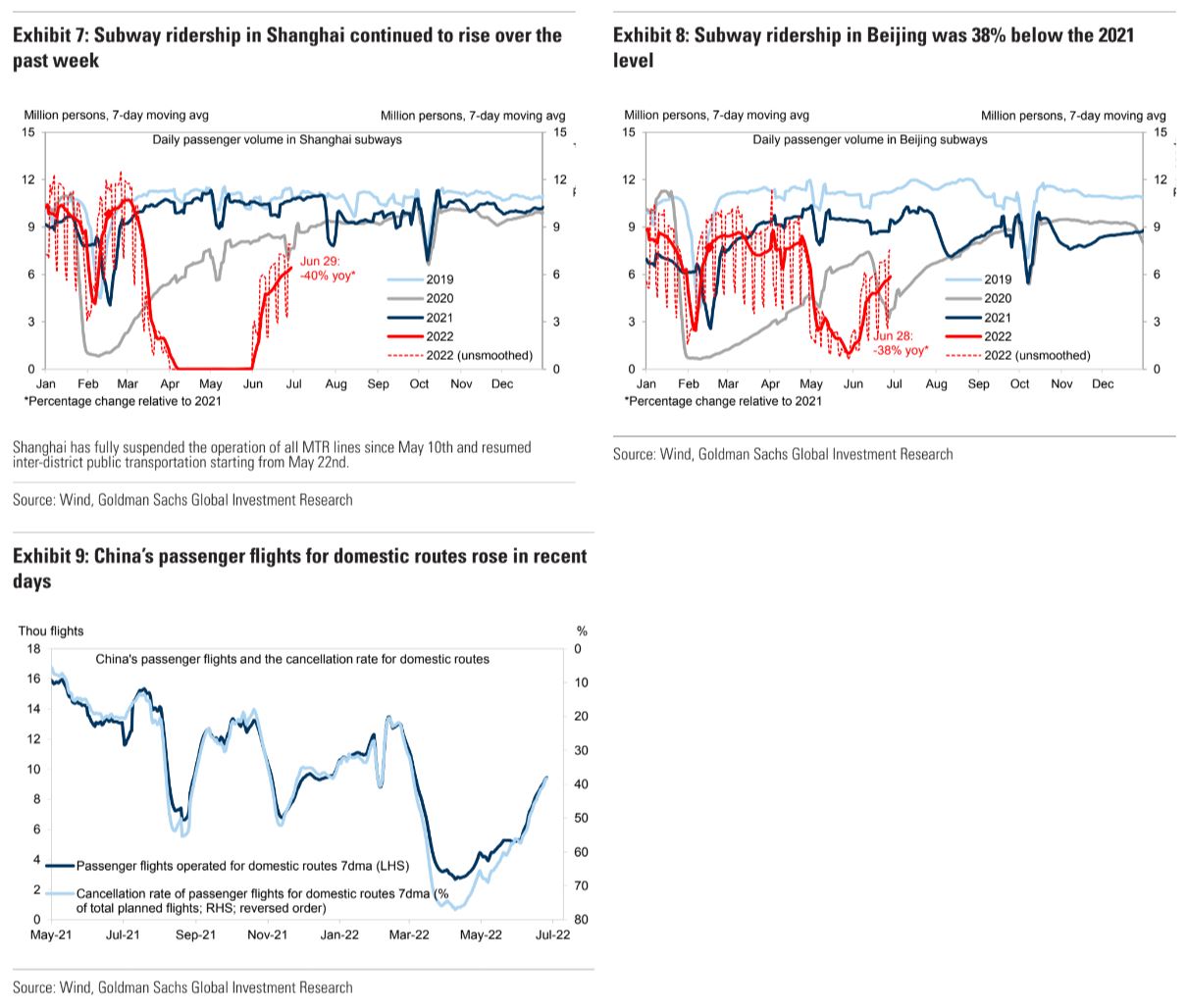

Mobility is back

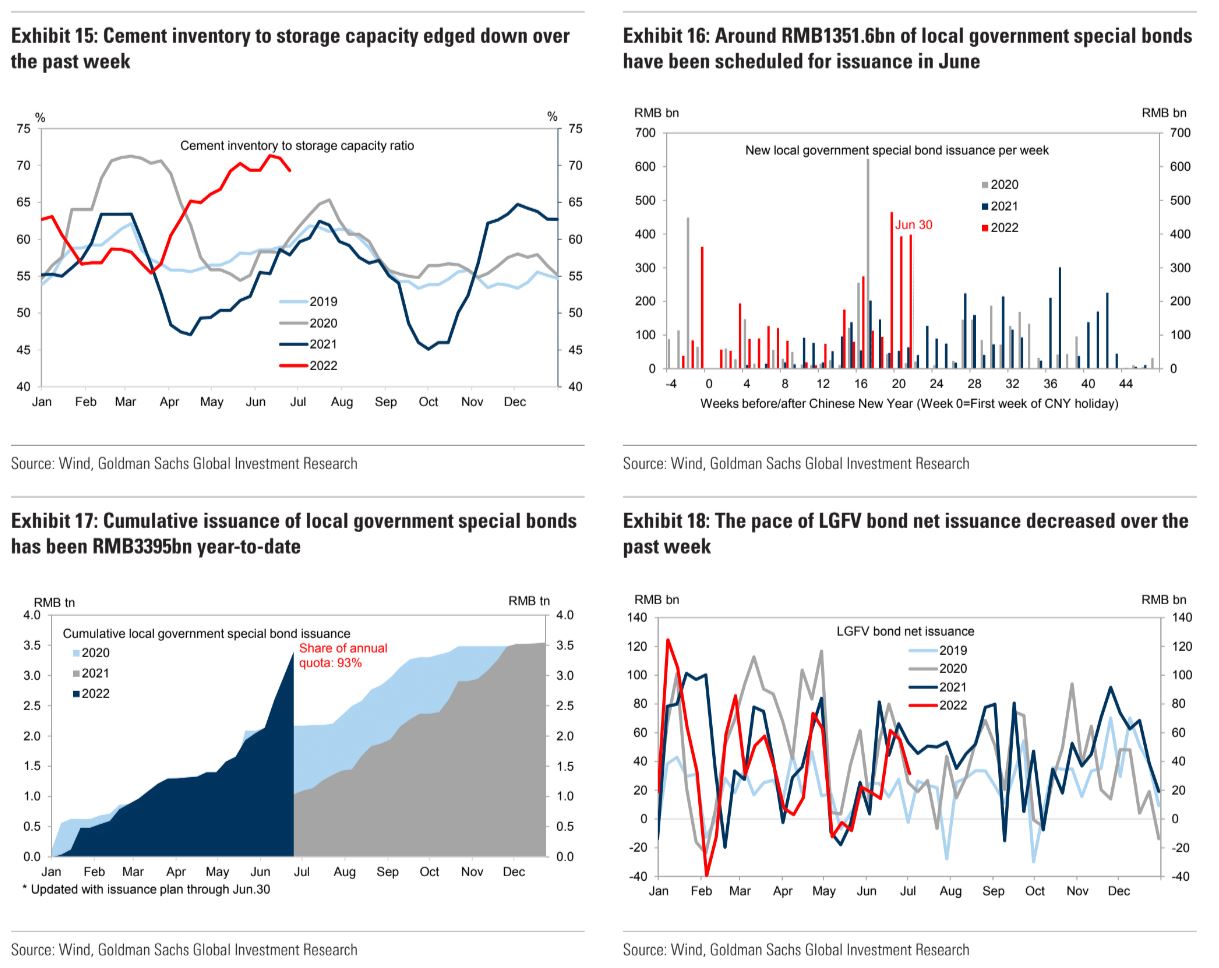

Infrastructure is the stimulus tip of the spear:

OMICRON has been imprisoned in Xinjiang:

Mobility is back

Infrastructure is the stimulus tip of the spear:

The full text of this article is available to MacroBusiness subscribers