By Gareth Aird, head of Australian economics at CBA:

Key Points:

- The RBA will raise the cash rate at the August Board meeting. We expect a 50bp hike.

- The risks sits with a larger increase, albeit we consider that risk to be very low.

- The RBA will publish their full suite of updated economic forecasts in the August 2022 Statement on Monetary Policy (SMP) on Friday.

- The RBA will significantly upwardly revise their near term profile for underlying and headline inflation (consistent with the Governor’s comments in late June that the RBA now expect headline inflation to peak at ~7% by the end of 2022).

- The RBA is likely to make a downward revision to their near term profile for the unemployment rate to 3.6% and hold that rate flat over their forecast horizon (i.e. we do not expect the RBA to forecast an increase in the unemployment rate).

- No forecast increase in the unemployment rate would imply that the RBA does not intend to take the cash rate to a contractionary setting (i.e. it would be consistent with the RBA taking the cash rate to their estimate of neutral which is~2.5% and then pausing for an extended period to assess the impact of rate hikes on the economy).

The decision

The coming week is another big one for Australian financial market participants. The RBA August Board meeting on Tuesday comes in the wake of the incredibly strong Q2 22 CPI.

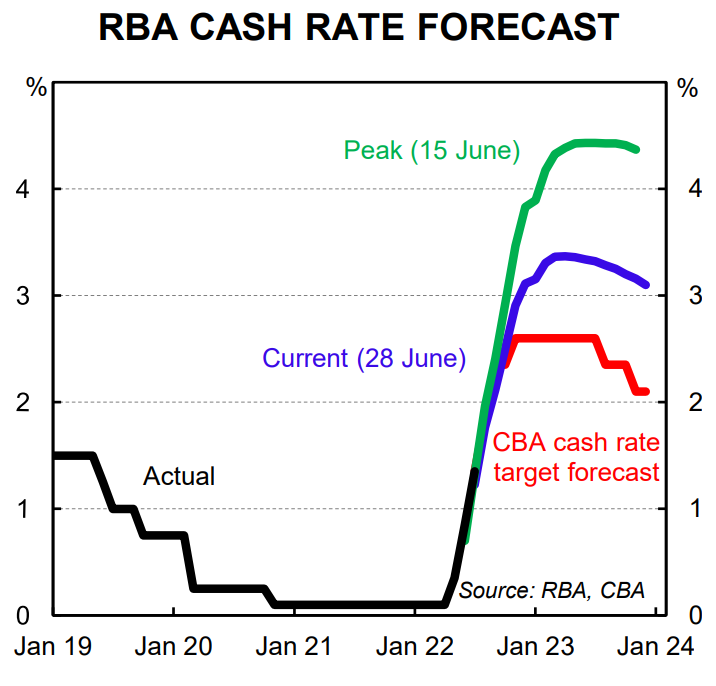

The strength and breadth of price rises in the inflation data means another big rate rise is likely and we expect a 50bp hike (this is the consensus call across the sell side of economists). Such an outcome would see the RBA take the cash rate to 1.85%.

And it would mean that 175bp of tightening has been delivered in just three months (i.e. 175bp of hikes over four meetings).

There is a small risk that the RBA delivers a bigger rate rise than 50bp. This could either be 65bp or 75bp. We consider both of these outcomes to be unlikely, but nonetheless the risk should be flagged.

A 65bp hike would take the cash rate to 2.0% (i.e. it would restore it to a conventional metric). In contrast a 75bp rate rise would keep the cash rate on an unconventional metric. And it would be a shock to financial markets participants (markets have currently priced a 50bp hike for the August Board meeting).

We believe the case to move the cash rate by more than 50bp at the August Board meeting is weak. The Q2 22 inflation data did not surprise to the upside. And whilst the annual rate increased, the quarterly pulse of inflation did not accelerate. In addition, the RBA Board meet more frequently than most other central banks, which reduces the need to deliver such a large hike at any given monthly meeting (here we must stress that 50bp is twice the size of a ‘business as usual’ 25bp hike – the economic fraternity is at risk of ‘normalising’ 50bp hikes).

The Governor’s Statement and the August SMP

Governor Lowe’s Statement accompanying the August Board decision will be important as he will preview the RBA’s updated economic forecasts, which will be published in the August SMP on Friday.

There will be some element of forward guidance in the Governor’s Statement. More specifically, we expect the RBA to retain a strict hiking bias and for the Governor’s Statement to contain the line, “the Board expects to take further steps in the process of normalising monetary conditions in Australia over the period ahead” – or words to that effect.

The RBA’s forecast profile for both inflation and the unemployment rate are the key metrics to consider when assessing the near term outlook for monetary policy.

Governor Lowe recently stated that the RBA now expects inflation to peak at ~7% by the end of the year. This was an upward revision relative to the RBA’s inflation forecasts in the May Statement of Monetary Policy (SMP) – headline inflation was forecast to peak at 5.9% in Q4 22 in the May SMP.

It is unusual for the RBA to revise their inflation forecasts between quarterly official forecast updates. But the recent upward revision has in large part been the basis for the RBA hiking rates in 50bp increments over the past two months rather than moving in ‘business as usual’ 25bp steps as they did in May.

We expect the RBA’s official updated inflation forecasts in the August SMP to mirror the Governor’s recent remarks that he expects inflation to peak at ~7% by end 2022.

The risk sits with a larger number given the Federal Treasurer this week stated the Government expects inflation to peak at ~7¾% by end-2022 (i.e. 0.75ppt above the RBA’s recent forecast).

The official forecasting family (i.e. the Commonwealth Treasury and the RBA) generally have similar economic forecasts at any point in time. But the Treasury has a higher estimate of the non-accelerating inflation adjusted rate of unemployment (NAIRU) which should result in a higher inflation forecast for a given level of unemployment.

In any event, the peak in inflation will not be the only important point to note in the RBA’s updated inflation profile. The rate at which inflation is forecast to fall will also be key to the policy outlook. We expect the RBA’s updated inflation profile to have both underlying and headline inflation returning to the top of the target band by either Q4 23 or Q2 24 (note that the RBA’s forecast profile is done on a semi-annual basis).

The RBA’s updated unemployment rate forecasts will also be important as they will provide a signal as to whether the RBA intends to take the cash rate to a contractionary setting. The RBA puts the neutral cash rate at ~2.5% (albeit they have low conviction on this estimate). If the RBA do not forecast the unemployment rate to rise over their forecast horizon it implies that they do not intend to take the cash rate above neutral. That does not mean they are unwilling to take the cash rate above neutral to a contractionary setting. But it would mean their base case internally is to take the cash rate to ~2.5% and leave it there for an extended period.

We believe such an outcome is the most likely result and aligns with our forecast profile for the cash rate. Namely, that the RBA takes the cash rate to 2.6% by November 2022 where we expect it to remain until H2 23 (note our forecast profile has two 25bp cuts in the cash rate in H2 23). Our estimate of neutral is ~100bp lower than the RBA’s, which means we think the central bank will inadvertently take the policy rate to a contractionary setting.

It is worth noting that the Government’s updated economic forecasts published this week put the unemployment rate at 3¾% in mid-2023 and 4% in mid-2024. These updated forecasts imply that the Australian economy does not have a hard landing and continues to perform well over coming years. We expect the RBA to have a similar profile for the unemployment rate albeit we think they are more likely to hold the jobless rate flat between mid-2023 and mid-2024 (the RBA’s lower estimate of NAIRU is likely to feed into this forecast).

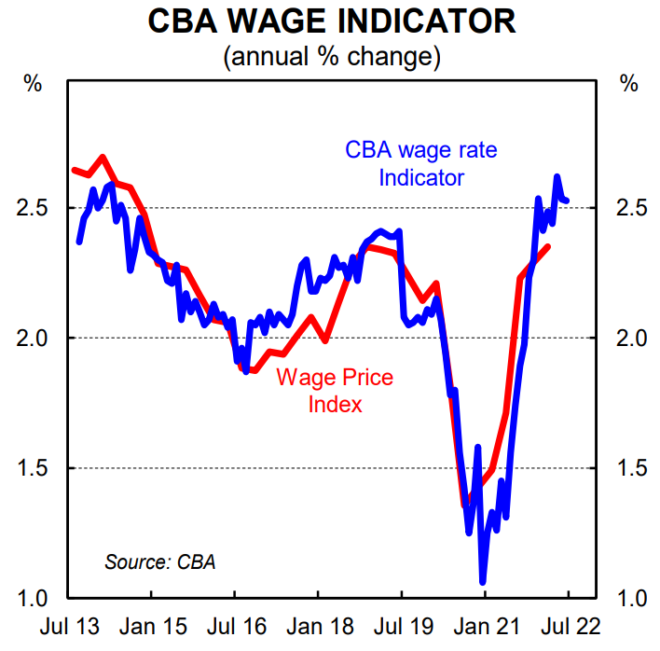

Finally we note that the Treasurer emphasised this week that Australia does not have a “wage-price spiral”. We very much agree. And our internal data on wages paid into CBA bank accounts supports this view (see below chart – latest data to June).