By Gareth Aird, head of Australian economics at CBA:

Key Points:

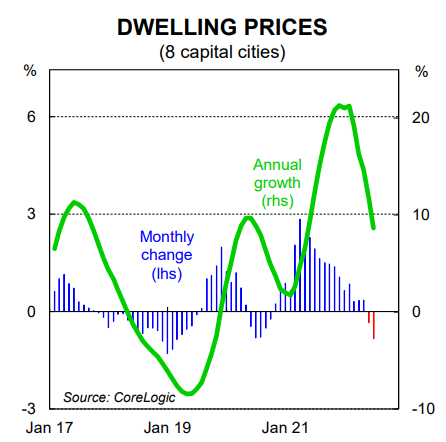

- Dwelling prices fell by 0.8% across the eight capital cities in June. Annual growth has dipped to 8.7%.

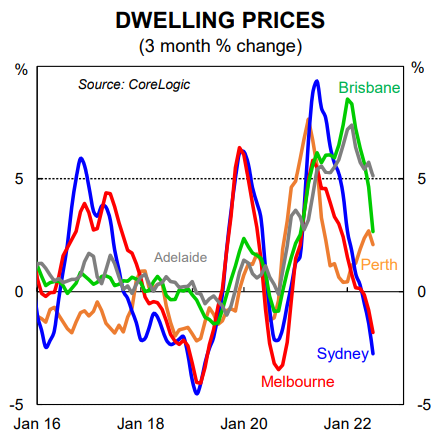

- Prices fell solidly in Sydney and Melbourne while gains were recorded in Brisbane, Perth and Adelaide.

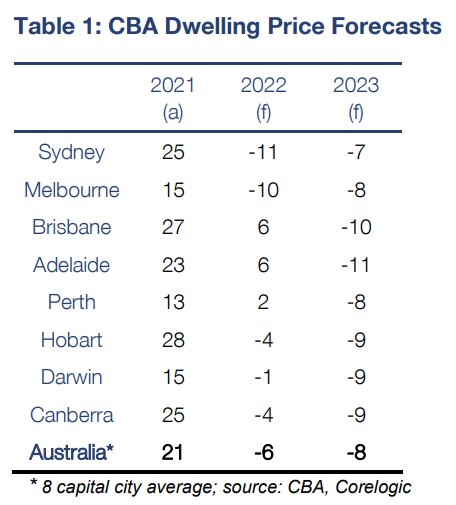

- Our expectation for the RBA to increase the cash rate to 2.10% by late-2022 means that we expect home prices nationally to fall by ~15% by end-2023 (peak to trough). Dwelling prices are anticipated to stabilise in late 2023.

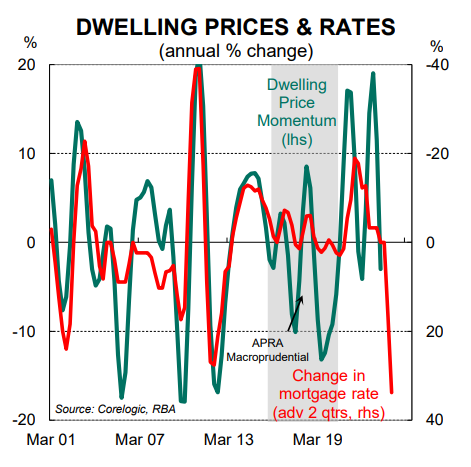

Dwelling prices in Sydney and Melbourne are moving swiftly lower

According to CoreLogic, Australian property prices fell for a second consecutive month across the eight capital cities in June. The 0.8% decline over the month was significantly larger than the 0.3% fall in May. The trend is now established and price falls will accelerate as the RBA continues to raise rates, which is widely expected.

Price outcomes are still divergent across the country. But we anticipate price movements will converge over H2 22 as rising rates both negatively impact the demand for credit across the country as well as weigh on borrowing capacity.

Dwelling prices fell by 1.6% in Sydney, our largest capital city, in June. This is a solid monthly fall and builds on the 1.0% decline in May. A large monthly fall was also posted in Melbourne (-1.1%). Buyer sentiment has turned sharply in Australia’s two biggest housing markets. Prices were also down in Hobart (-0.2%).

Dwelling prices rose across the other capital cities although it is clear that some markets are quickly running out of steam. Prices in Brisbane rose by just 0.1% in June whilst modest monthly gains were recorded in Perth (+0.4%) and Canberra (+0.3%). Dwelling price growth remained strong in Adelaide (+1.3%) and Darwin (+0.9%).

Price growth has now cooled significantly across regional Australia. The CoreLogic regional benchmark index rose by 0.1% in June.

House prices have fallen by more than unit prices over the past few months. This is a reversal of the trend in 2021 when the prices of detached dwellings rose at a faster pace than apartments.

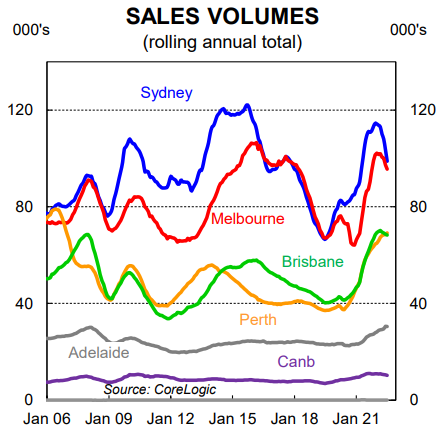

According to CoreLogic total advertised supply in Sydney and Melbourne is now ~7-8% higher than the same time a year ago. Advertised supply is well above the 5-year average in our two largest markets. And turnover has slowed.

CoreLogic estimate the volume of home sales was down by 36.7%/yr in Sydney over the June quarter while turnover in Melbourne was down by 18.3%/yr over the same period. Lower turnover has implications for state government stamp duty revenue.

And it will also negatively impact household goods retailing in time as turnover is positively correlated with some parts of the retail basket.

The Australian housing market is largely in the RBA’s hands

In early June we updated our forecasts for home prices based on our revised profile for the RBA (we expect the RBA to take the cash rate to 2.10% by end-2022 and leave the policy rate on hold for most of 2023; 50bps of cuts are pencilled in for late 2023). Our forecasts for home prices are very much conditional on the speed and magnitude at which the RBA lifts the cash rate.

Based on our forecast profile for the cash rate we expect home price falls nationally of around ~15% over the next eighteen months. Prices in Sydney and Melbourne are anticipated to decline by more than the other capital cities (see Table 1 below).

The expected falls in home prices are significant. But context is key. Price gains in 2021 nationally were extraordinary. Notwithstanding, there are many home owners who have bought recently. These buyers will feel the simultaneous negative impact of both rising interest rates and falling home prices. Deeply negative real wages growth further exacerbates the downbeat feeling amongst many households as evidenced in recent consumer confidence surveys.

The RBA does not target home prices. But the housing market and the broader economy cannot be separated. We expect the RBA to be cognisant of the nexus between changes in interest rates and the impact on home prices, household behaviour and consumer spending and the broader economy. Indeed behind closed doors we believe concerns will mount at the RBA if dwelling prices slide too quickly.

In the long run there are a number of factors that influence home prices; population growth and demographics, supply, household formation, taxation policy, income growth and policies around zoning and land release. But in the short run monetary policy is the key determinant of movements in home prices.

The RBA looks intent on front loading the tightening cycle and we expect a 50bp hike in the cash rate next week (see here). But if the RBA takes rates too high and too quickly relative to our forecast profile we would expect bigger falls in home prices. Larger falls in dwelling prices would have a negative impact on the real economy.

The RBA is placing a lot of weight on accumulated savings buffers in mortgage offset accounts to insulate many indebted households from rising rates. But whilst these buffers are positive from a financial stability perspective, households are unlikely to use money sitting in offset accounts to fund discretionary expenditure in an environment of sharply rising interest rates and falling home prices.

The RBA talked a lot in 2020 about the lower structure of interest rates supporting the economy through the normal transmission mechanisms which included “higher asset prices”. Indeed we saw the power of record low rates on full display in 2021 when they turbo charged the demand for credit and national home prices across the 8 capital cities rose by a whopping 21%.

We remarked on multiple occasions over the past few years that it is the percentage change in rates that has the biggest impact on home prices rather than the absolute change in rates. Thus changes in rates are at their most powerful when the rates are very low.

The reverse of what the RBA said in 2020 will also be true when it comes to a higher structure of interest rates and the impact on asset prices, particularly given the very low level of rates we started with. Indeed we expect an acceleration in home price falls over coming months due to further RBA rates rises. We believe the speed and size at which home prices correct lower will ultimately act as a limit to how high the RBA will be willing to take the cash rate.