Australian housing sentiment smashed

Westpac with the note.

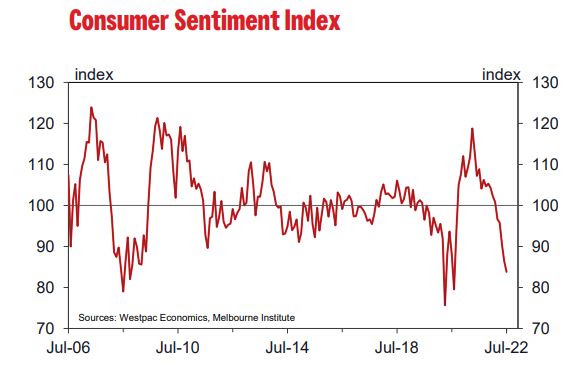

This marks the seventh consecutive monthly fall. Last month we noted the Index was already around levels that, since the beginning of the survey in 1974, had only been seen during periods of major disruption in the Australian economy including: the COVID pandemic; the Global Financial Crisis; the recession in the early 1990s; the slowdown in the mid–1980s and the recession of the early 1980s.

The fall in July means that the pace of the sentiment deterioration is now also in line with those earlier periods. The Index has now fallen 19.7% since December 2021, a precipitous tumble comparable to the two–month plunge during COVID (–20.8%); and the six–monthly declines seen heading into the Global Financial Crisis (–29.7%); the early 1990s recession (–20.5%); the mid–1980s downturn (–23.8%); and early 1980s recession (–18.8%).

Last month, responses to our quarterly questions highlighted the clear drivers of weakening sentiment with the most recalled news items being around inflation – around 60% of respondents recalled news on this topic compared to a long run average of 12%. Other news areas of note were ‘domestic economy’ (43% recall); interest rates (24%); and ‘international conditions’ (23%).

While we had expected inflation to be the main area of concern for consumers, we were a little surprised that interest rates did not figure more prominently, particularly given that the Reserve Bank had just delivered a surprise 50bp cash rate rise when most had been expecting a 25bp increase.

This milder than expected rate rise response last month was also apparent in the variations in sentiment across those surveyed before and after the RBA decision. The decision is always on the second day of the four day sample period.

Sentiment amongst those polled after the announcement, last month, was only 2.3% lower than sentiment amongst those polled before, indicating a fairly mild shock effect.

The response to the RBA’s 50bp rate increase in July was much sharper. Sentiment amongst those polled after was 7.4% below that of those surveyed before the decision.

Without doubt consumers are still very sensitive to the inflation pressures on their budgets but it appears their anxiety around interest rates is increasing.

This rising concern around interest rates is further emphasised by responses to our question on expectations for standard variable mortgage rates. Amongst those surveyed just after the RBA decision in June, 64.7% expected the rate to lift by more than 1ppt over the next twelve months. That proportion increased to 72.8% for those surveyed after the RBA’s July move, despite the materially higher starting point.

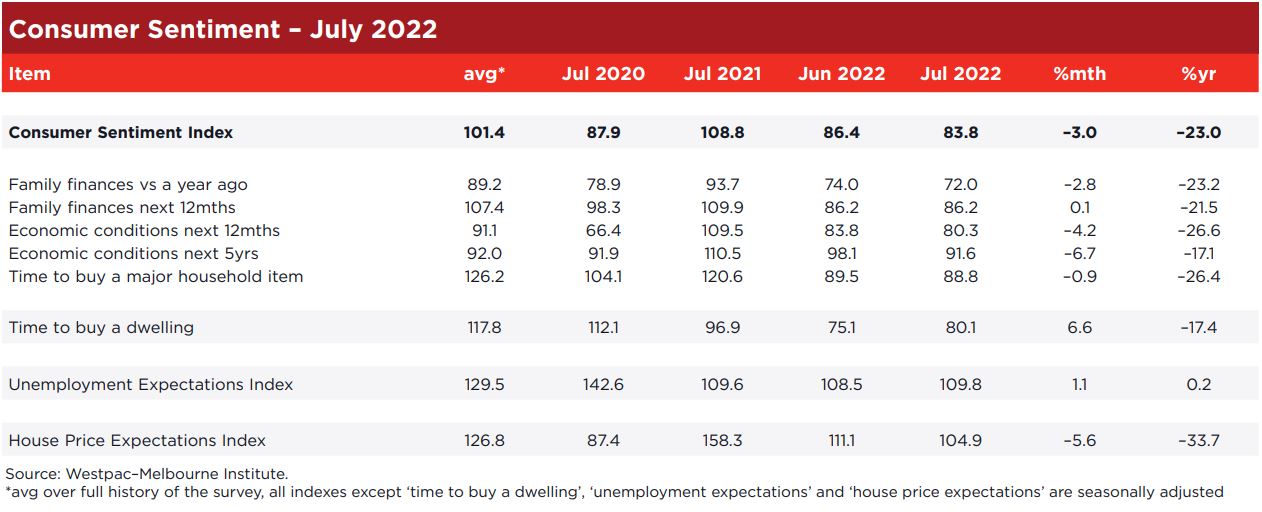

Component–wise, the biggest falls in July were around the economic outlook. The ‘economy, the next 12 months’ sub–index fell 4.2% and the ‘economy, next 5 years’ sub–index dropped 6.7%.

The ‘finances vs a year ago’ sub–index recorded a milder 2.8% decline while the ‘finances, next 12 months’ sub–index held steady. Both components registered very large falls in June (–7% and –7.6% respectively).

The ‘time to buy a major item’ sub–index was also relatively steady, falling 0.9%, having posted monthly declines of 3–6% over the previous four months.

Sentiment around the labour market remains strong. The Westpac Melbourne Institute Index of Unemployment Expectations lifted slightly from 108.5 to 109.7 – still a remarkably low print and well below the long run average of around 130 (recall that lower reads mean more consumers expect unemployment to fall in the year ahead).

We should not be complacent about labour market conditions as there are often significant lags between shifts in the confidence measures and the labour market. During the Global Financial Crisis for example, the peak in the Unemployment Expectations Index came in early 2009, more than six months after the low in Consumer Sentiment. That cycle saw the Unemployment Expectations Index go on to average 173 over the following nine months in 2009, 33% above its long run average level!

However, some of the resilience of the Unemployment Expectations Index to date reflects the constrained supply of labour following extended external border closures. This factor, while easing somewhat, will likely work to offset any prospective weakening in labour demand, meaning shocks to Unemployment Expectations may continue to be milder than in 2008–09.

The survey continues to send a very clear message about housing.

While the ‘time to buy a dwelling’ index lifted 6.6% in July, to 80.1 it remains at a weak level overall (39% below its recent peak in November 2020). The monthly gain was due to large increases in Queensland and Western Australia, with homebuyer sentiment still very weak in NSW (holding almost steady at 73.9) and Victoria (falling by 11% to 75.7).

Meanwhile, consumer house price expectations are continuing to slide. The Westpac–Melbourne Institute House Price Expectations Index declined a further 5.6% in July to 104.9. Expectations have dipped into net negative territory in NSW (–6.2% to 97.3) and Victoria (–2.4% to 99) meaning more consumers now expect prices to decline than rise over the next twelve months. This compares to a much firmer read of 115.2 in Queensland (albeit with price expectations down a heftier 9.3% in the month).

While price pessimists now hold sway in the two big states, there is considerable scope for expectations to fall further. During the last significant housing market sell–off, in 2018–19 the NSW index bottomed out at 68.7 while the Victorian index hit a low of 71.7.

Respondents who own their homes outright are particularly downbeat with a House Price Expectations Index read of 78.9, down 16.8% in the July month alone. Perhaps, these experienced homeowners, who have seen cycles in the past, are more attuned to the damage sharp increases in interest rates can have on housing markets.

The Reserve Bank Board next meets on August 2. We expect the Board to raise the cash rate by a further 50bps, taking it to 1.85%, near the top of our assessed ‘neutral zone’ of 1.5–2.0%.

The move will come after a June quarter CPI update, due on July 27, that is expected to show a significant further lift in inflation – we expect annual underlying inflation to come in at 4.5%yr, up from 3.7%, and annual headline inflation to hit 5.8%yr, up from 5.1%yr.

The Board is committed to containing inflation over the medium term. To deliver on this, and to contain inflation expectations, it will need to continue taking strong actions with policy, pushing the cash rate from a very stimulatory starting point to something well into the neutral zone.

However, the Board will also be wary of the heavy impact this is having on what is now very fragile confidence and the historical precedents we have noted in this report. The cash rate has increased at a faster pace than we have seen in any cycle since 1994 and this is clearly unsettling for consumers also facing a sharp rise in the cost of living.

A more cautious approach will be appropriate once policy has moved to ‘neutral’ in August. We advocate and expect the Bank to pause to assess conditions, both domestic and global, prior to moving rates into the contractionary zone later in the cycle.