DXY took off again last night and that did all of the work:

AUD fell though is tearing it up on the crosses as Albo’s inflation shocker mushrooms:

Commods are holding on hope:

EM stocks faded:

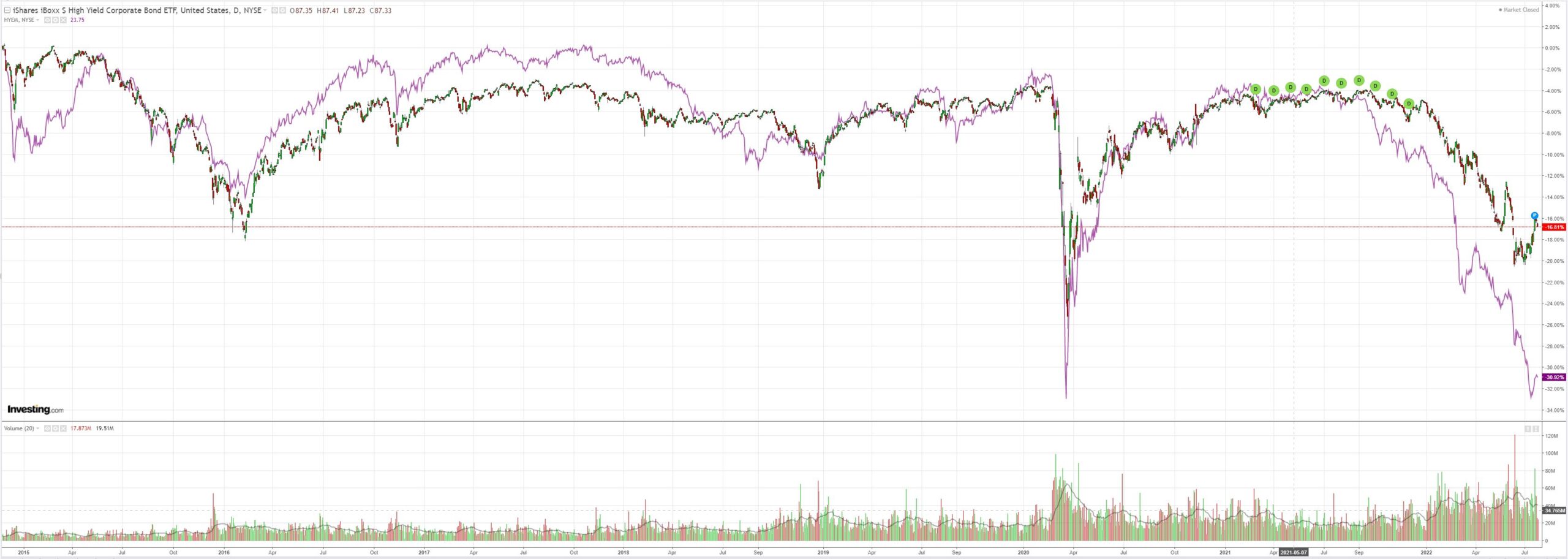

Junk rolled:

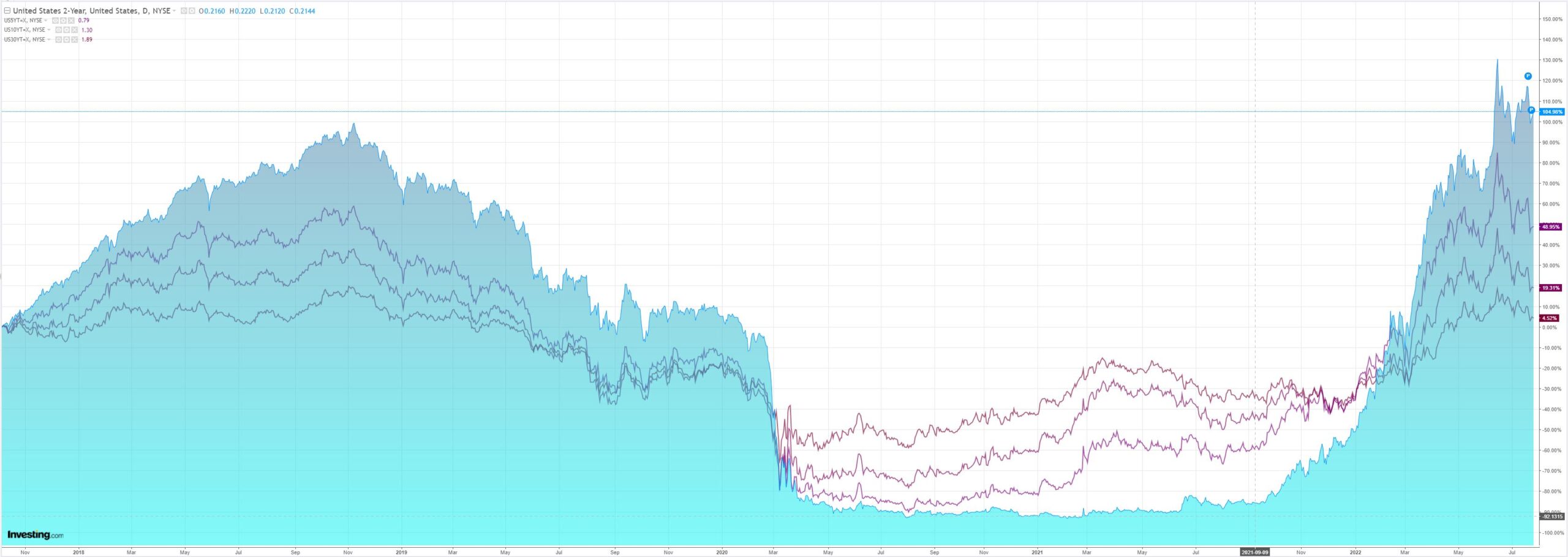

Yields were stable:

And stocks slammed:

Westpac has the wrap:

Event Wrap

US consumer confidence (Conference Board) disappointed at 95.7(est. 97.0, prior 98.4). Among components, the job strength index fell to a 14-month low, while 1-year ahead inflation expectations slipped to 7.6% from June’s all-time high of 7.9%. The Richmond Fed manufacturing survey beat expectations, at 0 (est. -14, prior -9). New home sales in June fell 8.1% (est. -5.9%, prior +6.3%) to a 26-month low. The median price fell 9.5% from May (April the all-time high). House prices (CoreLogic) rose 1.3% in May (est. 1.5%, prior 1.7%), for an annual pace of 19.8% (prior 20.6%).

The IMF again downgraded its world growth outlook and warned of a global recession. It forecasts growth of 3.2% this year (was 3.6%), and 2.9% in 2023. Notable risks included the Ukraine war, Russian sanctions, growth in China, fresh pandemics, and price pressures and rate hikes. It forecasts global consumer prices will rise by 8.3% this year (was 7.4%).

Event Outlook

Aust: The Q2 CPI will be published. In terms of key drivers, ongoing construction input inflation should see a solid lift in dwelling prices, while food and auto fuel components are also primed for a strong contribution. Westpac’s forecast of a 1.7%qtr (6.1%yr) lift in the headline CPI are slightly lower than the market’s (1.9%qtr; 6.3%yr). Widespread pressures from both domestic and international sources will support a solid 1.4%qtr (4.6%yr) gain in the trimmed mean measure.

China: Industrial profits will rebound as the recovery from COVID-19 ensues.

US: A 75bp hike is widely anticipated at the FOMC’s upcoming policy meeting, with the focus therefore being on the Committee’s views on risks. Wholesale inventories should post another robust gain in June (market f/c: 1.5%); however, economy-wide performance is varied, as evinced by businesses’ struggles against supply issues with durable goods orders (market f/c: -0.4%). Meanwhile, pending home sales are expected to decline in June as higher mortgage rates weigh on housing demand (market f/c: -1.0%).

It’s CPI day in Australia and Fed day in the US tomorrow. AUD is resisting the risk sell-off based on the former. The latter could end that.

I expect an undiminished hawkish Fed.