Today’s meeting by the RBA, where everyone and his dog is expecting a solid 0.5% or 50 basis point hike, is not going to save the beleaugured Australian dollar.

First, the wonks at ING rationale for the big five oh:

- the inflation expectations data, (with a) 6.7% print in the latest release, should have banished any thoughts of a lesser hike or even no hike at all.

- The other factor to consider is that with the latest inflation rate at 5.2%, and probably higher when we get the 2Q figure on 27 July, at 0.85% the RBA cash rate target is well off where it needs to be to even remove stimulus from the economy, and even further away from actually starting to restrict growth and bring inflation down.

- So it has to be at least 50bp.

Of course the best thing to arrest inflation is to make two thirds of all households mortgages (borrowers and slumlords) more expensive, thus pushing workers to ask for more for wages to cover the shortfall? The macro outlook is more opaque still with a slowing China, a pullback in iron ore prices, stubbornly high energy prices and a probable US recession around the corner.

The RBA does like to play catchup, usually late and well after they’ve been invited to the game, so “normalising” rates quicker than expected is nothing new for the boffins at Martin Place.

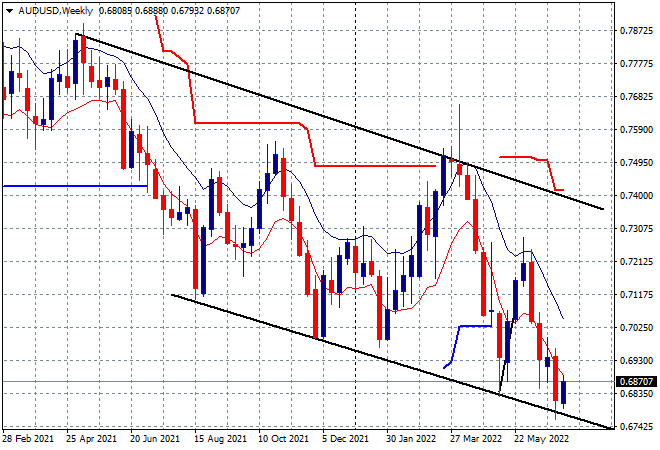

But for the technical picture on the Aussie, its all downhill, with the weekly chart looking through the usual 200 pips a month volatility that many market economists seem to forget about when analysing the Pacific Peso. Its currently at the bottom of its trend channel, so a bounceback towards the mid zone at the 70 handle is not unlikely at all in the reaction to a 50 bps hike by the RBA:

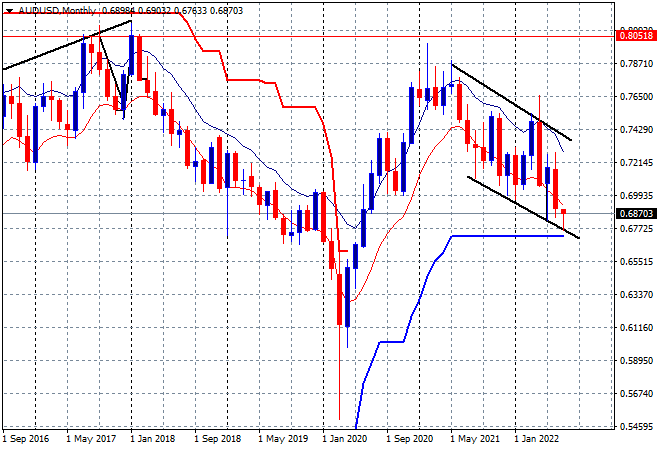

But perspective matters and switching to the monthly chart shows how the post COVID bounce is now rolling over like a dead cat, with an inverse relationship to the cash rate:

With the Federal Reserve (currently at 1.5 to 1.75%) looking to add nearly 200 bps in rate hikes before the year is out, the RBA is way behind, even with the 50 points added to make it 1.35%, which will not give the Australian dollar any relief past the temporary volatility.

- Aussie dollar approaches the July RBA meeting with mostly headwinds, and a significantly weakened link between domestic monetary policy dynamics and AUD/USD suggests that a rebound towards the 0.7000 mark is unlikely to materialise soon even in the event of a hawkish surprise by the RBA (markets are not fully pricing in a 50bp hike).

- The size of RBA tightening likely has implications for FX only beyond the short-term, and in an environment where markets feel more comfortable with their pricing of a global slowdown and see the peak in rates, which could fuel a stabilisation in global risk sentiment and re-connection between short-term rate dynamics and FX. From this perspective, a more aggressive RBA tightening can suggest a wider room for AUD/USD recovery towards the end of this year and the start of next year (assuming that’s when market sentiment begins to recover), but a number of other factors – especially related to China’s demand and the USD outlook – will continue to be playing a big role too. All this makes any consideration about the AUD outlook purely based on rates dynamics still reductive.