Tuesday’s speech by RBA assistant governor Michele Bullock concluded that Australian households are well positioned for rising interest rates:

As a whole households are in a fairly good position. The sector as a whole has large liquidity buffers, most households have substantial equity in their housing assets, and lending standards in recent years have been more prudent and have built in larger buffers for interest rate increases. Much of the debt is held by high-income households that have the ability to service their debt and many borrowers are already making repayments well above what is required. Furthermore, those on very low fixed-rate loans have some time to prepare themselves for higher interest rates.

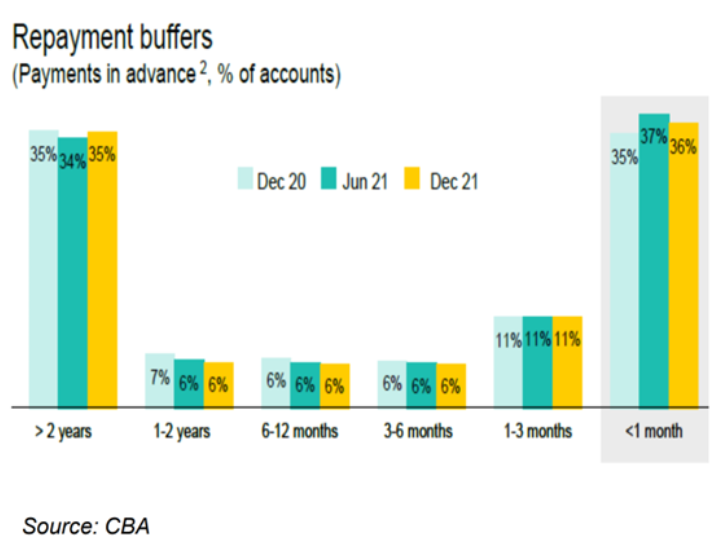

Yet, this claim is contradicted by data from the CBA, which shows that 36% of all borrowers have zero buffer and nearly half have less than 3 months buffer:

CBA: Nearly half of Aussie mortgage holders have minimal savings buffer.

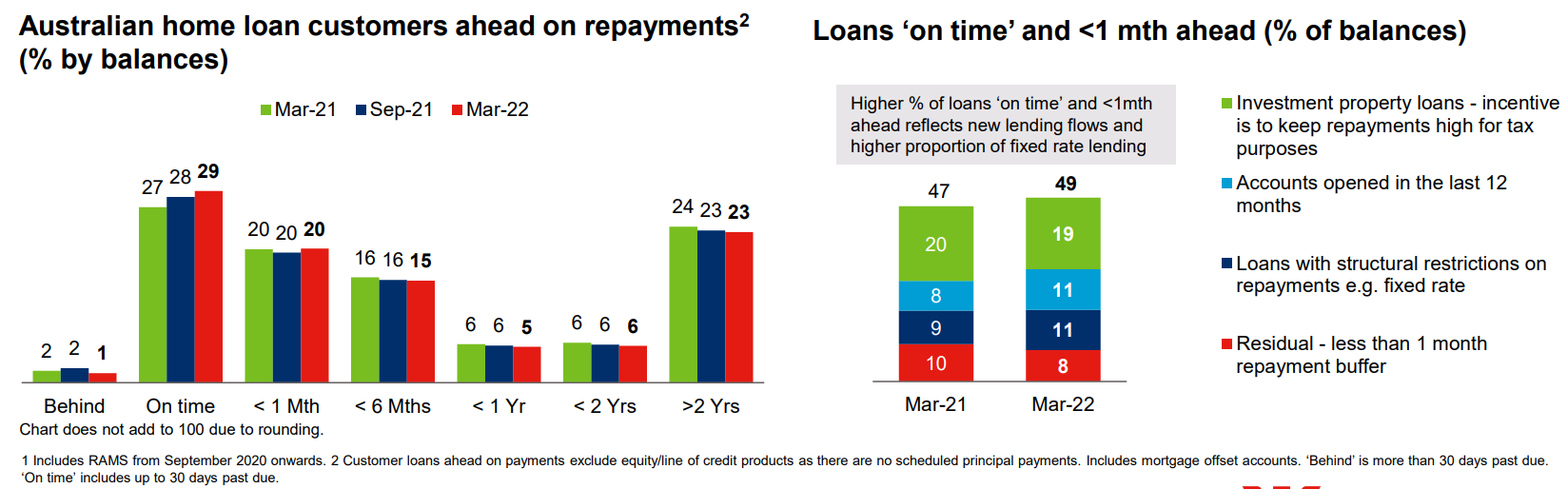

Separate data from Westpac, posted on Twitter by Chris Joye, likewise shows that exactly half of all borrowers are less than one month ahead on their mortgage repayments, or behind:

Westpac: Half of borrowers less than one month ahead on mortgage repayments.

So, according to Australia’s two largest banks, which comprise a huge share of the nation’s mortgage market, around half of all borrowers have minimal buffer.

Turning to the right side Westpac chart above, it is really the bottom three categories that are of most concern – i.e. recent buyers that have taken out mortgages over the past 12 months (11% of borrowers), those on fixed rate mortgages that will soon reset at a much higher rate (11% of borrowers), and the residual 8% of borrowers making minimum repayments.

These borrowers are likely to be most sensitive to rising mortgage rates, or will face a huge uplift in repayments when their cheap fixed terms expire next year.

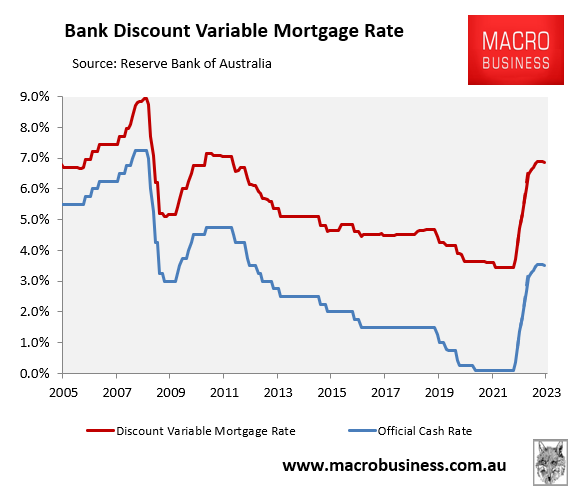

How it all plays out remains to be seen and will obviously depend on how aggressively the RBA hikes interest rates. However, if the RBA follows ANZ or the market’s forecast, and hikes the official cash rate (OCR) above 3% by year’s end, then variable mortgage rates will climb above 6.5% to levels not seen since 2012:

Markets and ANZ: variable mortgage rate to soar above 6.5%.

In turn, this would see average principal and interest mortgage repayments as a share of household disposable income climb to their highest ever level.

It is hard to fathom how the biggest increase in mortgage repayments in the nation’s history could be digested by households without many suffering severe financial pain, consumption spending collapsing, and the housing market crashing.