The Reserve Bank of Australia (RBA) has updated its household finances data for the March quarter, which presents the financial position of Australian households at the housing market’s peak just one month before the RBA commenced hiking rates.

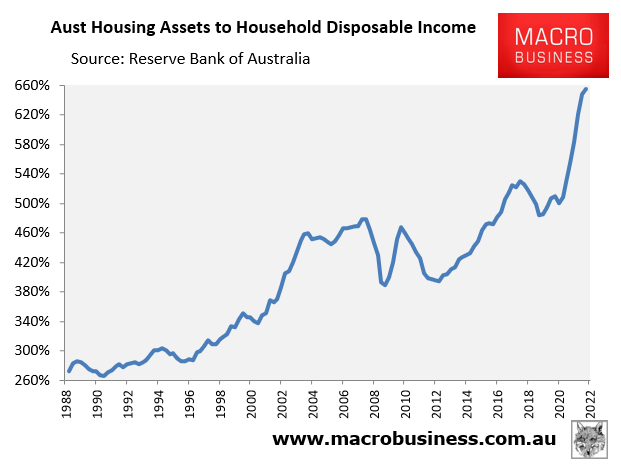

As shown in the next chart, the value of Australia’s housing assets hit an all-time high 6.6 times household disposable income in the March quarter – up significantly from the pre-COVID level of around 5.1 times incomes:

The rise and rise of Australian property valuations.

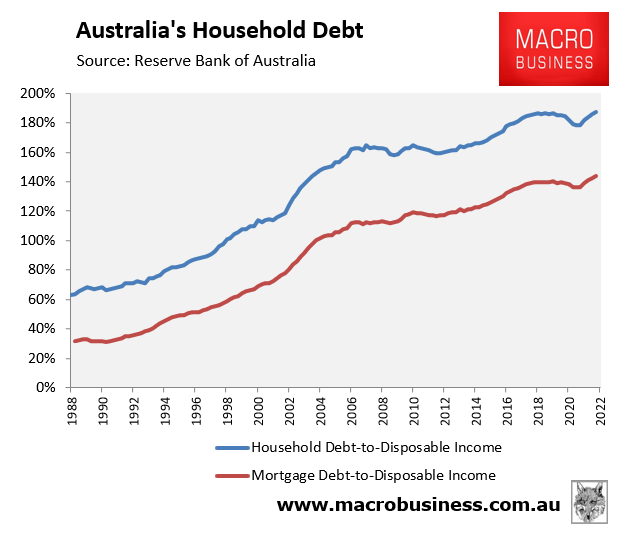

This rise in housing values was associated with an escalation of mortgage debt, which hit a record high 144% of household disposable income in the March quarter, in turn driving the ratio of household debt to income to an all-time high 187% of income:

Australia’s mortgage and household debt hits record highs.

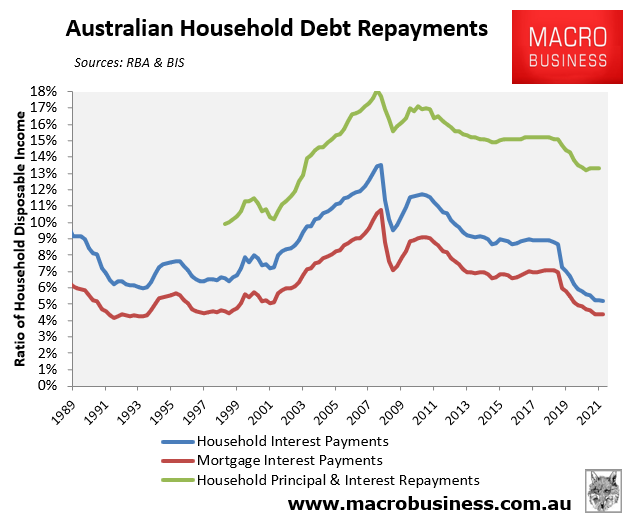

The inexorable rise in house prices and debt was driven by the cratering of mortgage rates, which lowered the cost of servicing debt and enabled Australians to leverage-up.

As illustrated in the next chart, interest payments on mortgages fell to a 22-year low of 4.4% of disposable income in the March quarter, whereas interest payments on total household debt fell to an all-time low 5.2%. However, because the sticker cost of housing has risen so sharply, total principal and interest repayments have not fallen as sharply; albeit were at around 2003 levels in the December quarter of 2021 (green line below):

Australian household debt repayments shrunk as interest rates hit rock-bottom.

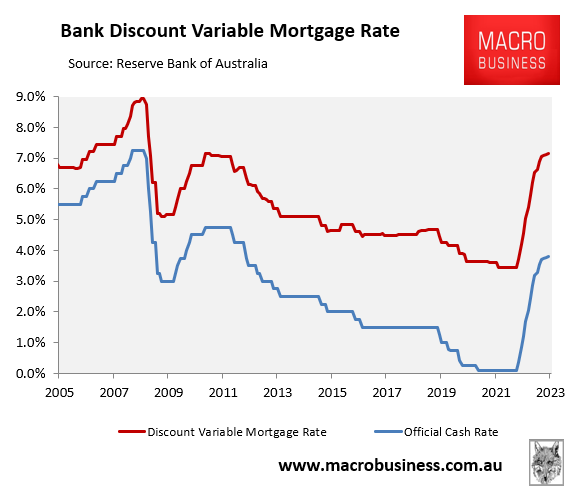

The above data obviously represents the turning point. In May, the RBA commenced its rate hiking cycle with its initial 0.25% increase, which was followed by another 0.5% hike in June.

The futures market tips that the official cash rate will lift to 3.15% in December before hitting 3.75% in June 2023. If true, this would push the average discount variable mortgage rate to 7.1%, which would be more than double its pandemic low of 3.45%:

Australian mortgage rates to double!

In turn, average principal and interest mortgage repayments would soar by around 50% from their level immediately before the RBA’s initial 0.25% rate hike – representing the highest debt repayment burden in the nation’s history.

Given both housing valuations and debt were at their highest levels ever in March, this means Australians have never been as sensitive to interest rate hikes. Thus, any aggressive lift in interest rates by the RBA is certain to cause extreme financial pain and could drive a major house price crash and recession.

Australian households’ extreme debt loads necessarily mean that the RBA must tread very carefully on rates.