BofA joining the bears. It’ll be mild only if the Fed does not break something and it usually does. The other factor is the giant US inventory pile. Any destocking of size will turn a mild recession moderate.

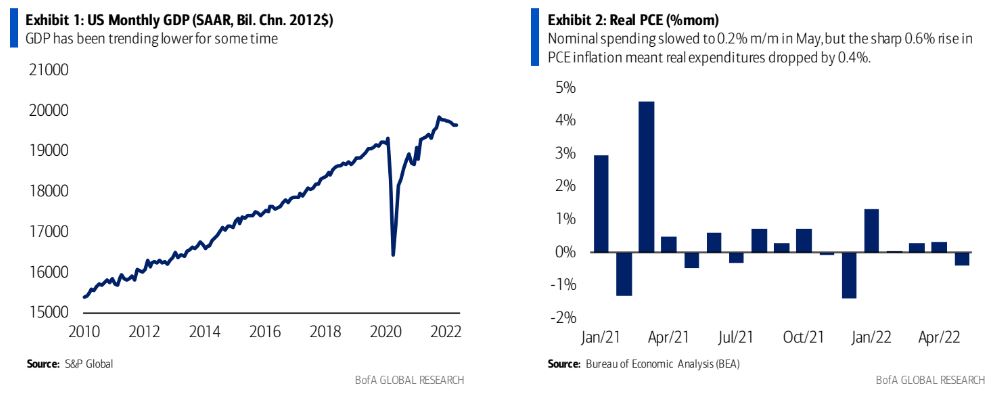

Economic momentum has faded faster than expected

Our previous baseline outlook for the US economy featured a growth recession (e.g.,output growth remaining positive, but below our estimate of potential), but a number of forces have coincided to slow economic momentum more rapidly than we previously expected. Perhaps most worrisome to us is the trend in services spending, where revisions to prior data and incoming data, including from our BAC aggregated credit and debit card data, point to less momentum than we had been assuming.