Even before today’s expected 0.5% rise in the official cash rate, Australia’s various housing indicators are flashing red for property prices.

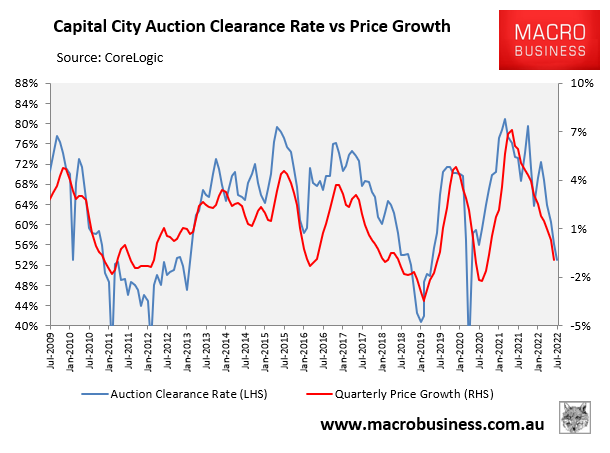

The latest national auction clearance rate, which has traditionally been a sound leading indicator for price growth, has collapsed – recording its worst result since April 2020 when the nation was in hard lockdown:

Auction clearances point to falling dwelling prices.

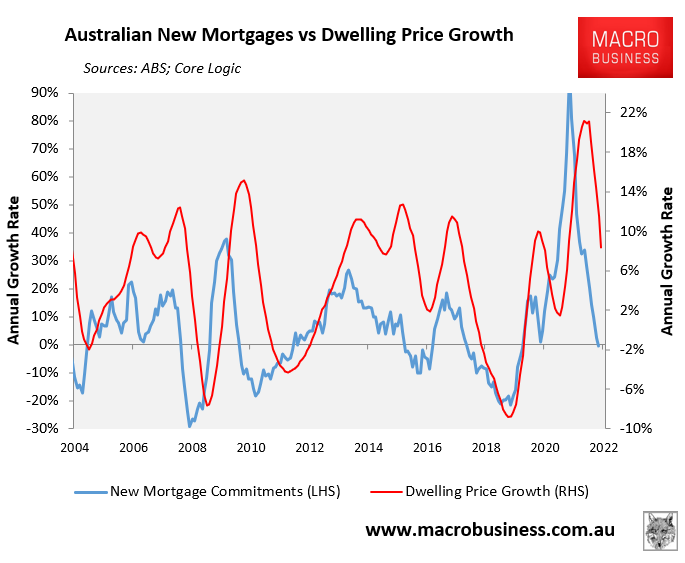

Annual mortgage finance growth also turned negative in May, which given historical correlations points to falling dwelling prices:

Mortgage demand also pointing to falling prices.

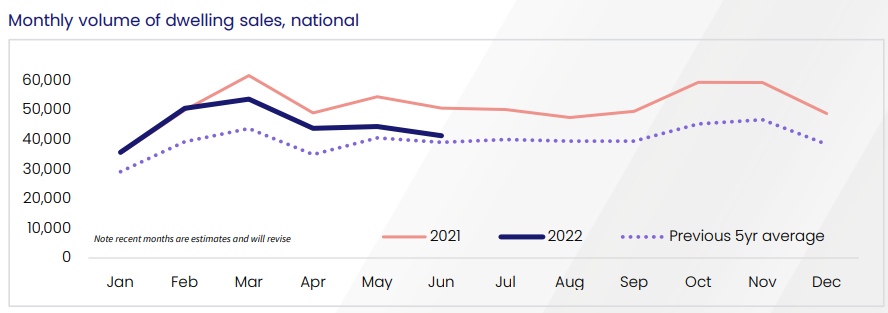

Viewed together, both indicators suggest that home buyer demand has evaporated. This view is supported by the trend reduction in dwelling sales over 2022 toward the five year average:

Sales volumes are falling.

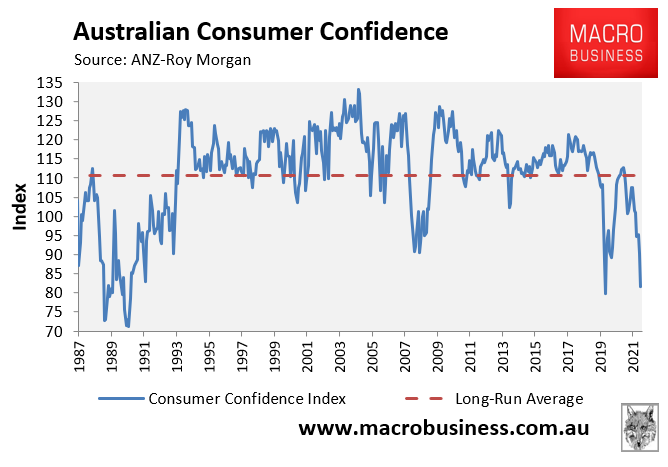

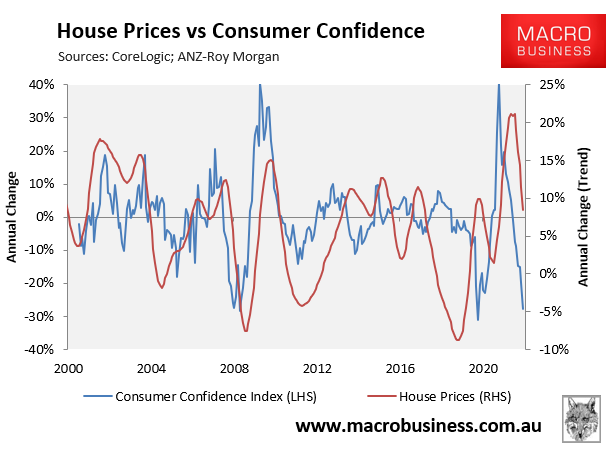

Finally, the Reserve Bank of Australia has commenced this monetary tightening cycle with consumer confidence at recessionary levels, well below the lows of the Global Financial Crisis:

Australian consumer confidence is already at recessionary levels.

The consumer confidence index has traditionally been another leading indicator for house price growth, as illustrated in the next chart. As such, the collapse in confidence points to falling house prices:

Poor consumer confidence usually means lower house prices.

The median economists’ forecast is for the official cash rate to peak at 2.85%. This would correspond to a discount variable mortgage rate of 6.2%, which would represent a huge increase on the 3.45% mortgage rate that existed before the RBA commenced its rate tightening cycle.

The futures market is even more hawkish, tipping the Reserve Bank to lift the cash rate to 3.6% by mid next year. This would lift the discount variable mortgage rate to 6.9% – exactly double its pre-tightening level.

If either scenario came to fruition, it would cause a further sharp contraction in home buyer demand and consumer confidence, thereby driving serious house price falls.