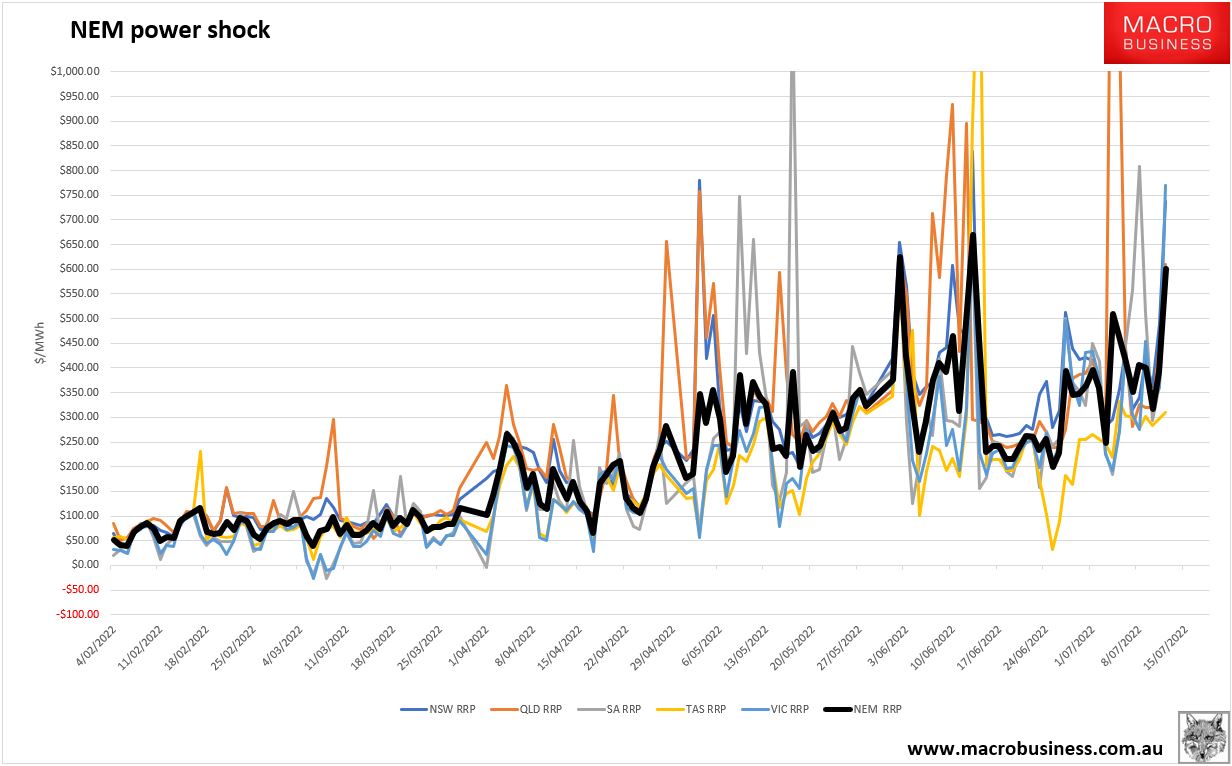

Yesterday saw the third-highest average price of electricity in Australian history:

A month ago these same prices led the Australian Energy Market Operator (AEMO) to suspend the National Electricity Market (NEM). Since then, everybody has fulsomely praised what a great job it is doing as prices spike back to 1200% up.

Is the AEMO going to suspend the power auction process again? Or is it too embarrassing? This is patently a failed market with a failed regulator. There are no “ifs” or “buts”.

Advertisement

This is probably going to get worse before it gets worserer. Deutsche:

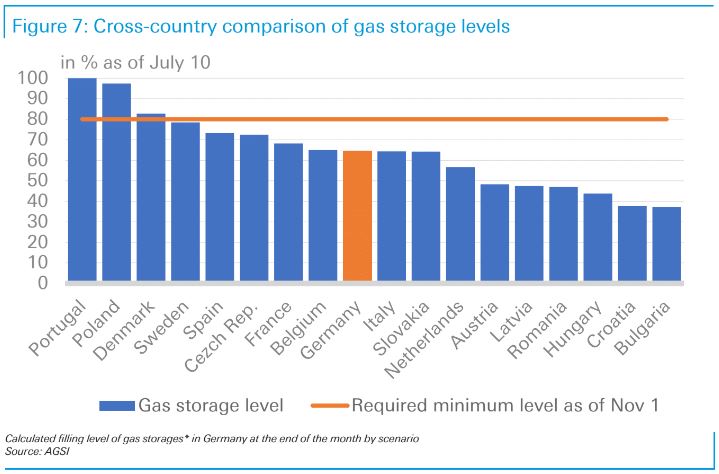

Yesterday marked the first day of a scheduled 10-day maintenance shutdown of the Nord Stream 1 pipeline. Germany entered this maintenance period with gas storage levels filled at 64.6% on average, with no (significant) net inflows expected during the maintenance period. By Sunday, overall dependence on Russian gas imports had fallen to around 25% from around 45% of total German gas imports in mid-May. While this looks like good news at first sight, this means 25% of an overall reduced level of gas imports, spelling potential problems towards the end of the heating period (March/April 2023). As chart 1 illustrates increased imports from Norway, the Netherlandsand Belgiumcould not make up for lower Russian imports. Thus, substitution (coal, etc.) and demand reduction will be important to prevent a significant gap in gas supply.

Status quo ante: No (severe) supply problems even in case of high re-exports

If Russian gas supplies return to the levels we had seen directly before the maintenance of Nord Stream 1, gas supply will be secured in Germany over the next winter. Even in case of a high re-export share of 45% over the next few months, German gas storages levels would be somewhere close to 10% in late April 2023. With a share of re-exports of 40%, storages levels could reach 90% by the end of October. That would comply with security of gas supply regulation foreseeing a 90% storage level as of November 1st. The most comfortable situation in scenario 1 ensues if the share of re-exports in gas imports remains at a low level of 35% only. In that case, the filling level of storages would be above 40% even at the end of the winter season, which is indeed another threshold required by law (40% by February1st).

Balanced on a knife-edge: Re-exports are the decisive factor

In the scenario of another halving of Russian gas supplies to Germany, the share ofre-exports is the decisive factor for security of supply in Germany. With a low share of 35%, gas supply would be secured even with reduced Russian deliveries. Storage levels would be at 15-20% at the end of April 2023. The picture is already very different in case of a re-export share of 40%. Gas storages would be fully depleted during April. Thus, a rationing of gas might become necessary at the end of the winter season. If the share of re-exports rose to 45%, storage capacities would already be depleted in March 2023.

Welcome to a winter of gas rationing: Russia turns off the gas taps

If Russia fully stopped gas supplies to Germany after the current maintenance period, a rationing of gas could not be prevented during the winter months. Even if re-exports reached a level of only 35% during the months ahead, the filling level of storage capacities would tend towards zero during March 2023. With a re-exports hare of 45% (much higher than the recent level), storages would already be depleted by the end of January 2023. Since critical infrastructure and private households would be treated with priority in case of physical shortages in gas supply, industrial consumers would be affected most. The government, large individual gas consumers, and industry associations are currently discussing which facilities could be switched off first.

Never fear, Albo’s cowards are busy furiously debating energy security in 2050!

Advertisement

Albanese said: “It is essential that the unprecedented levels of investment in clean energy technologies required over the coming decades unlocks more diverse and secure supply chains than we have today.

“Greater diversity and security of critical minerals extraction and processing, greater diversity of clean technology manufacturing, and security of clean energy supply are essential for managing supply and strategic risks.

“Together, we can ensure better access to affordable, reliable and secure clean energy right across the Indo-Pacific as we move to a net zero world.

“Australia is eager and ready to do our part.”

Albanese said that when he meets G20 leaders in Bali in November, he will draw on the forum’s discussions, “particularly your views on energy security and the transformative role of clean energy technologies”.

You may be wondering how Albo could be so impossibly stupid. Where is the consistency in worrying about a China-secure supply chain for renewable energy decades hence when China is today destroying the east coast economy by plundering 71% of its gas resulting directly in the failure of the entire power market?

There is one line of consistent thought in both and it is this. Ignoring the total collapse of the NEM today, and campaigning for less China in renewables tomorrow, both benefit miners.

Advertisement

This is the key insight into this government of poltroons. They will allow a 1200% power shock that sucks $95bn out of the east coast economy if prices stay this high, plus sends the cash rate to 5% and halves house prices, so long as it adds to mining profits.

Moreover, given this has the political potential to boil over completely and force Albo’s cowards to act mid-global gas crisis, how do we think that our European allies will react if domestically reserve gas in a panic then instead of now?

Albo’s cowards are the hideous abortive offspring of Keven Rudd’s failed prime ministership. They are governing directly from the black hole of fear that Rudd’s failed mining taxes opened. Never again will Labor be rolled by angry miners.

Advertisement

And the rest of you – every single business and household east of the WA border – can just fuck right off.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.