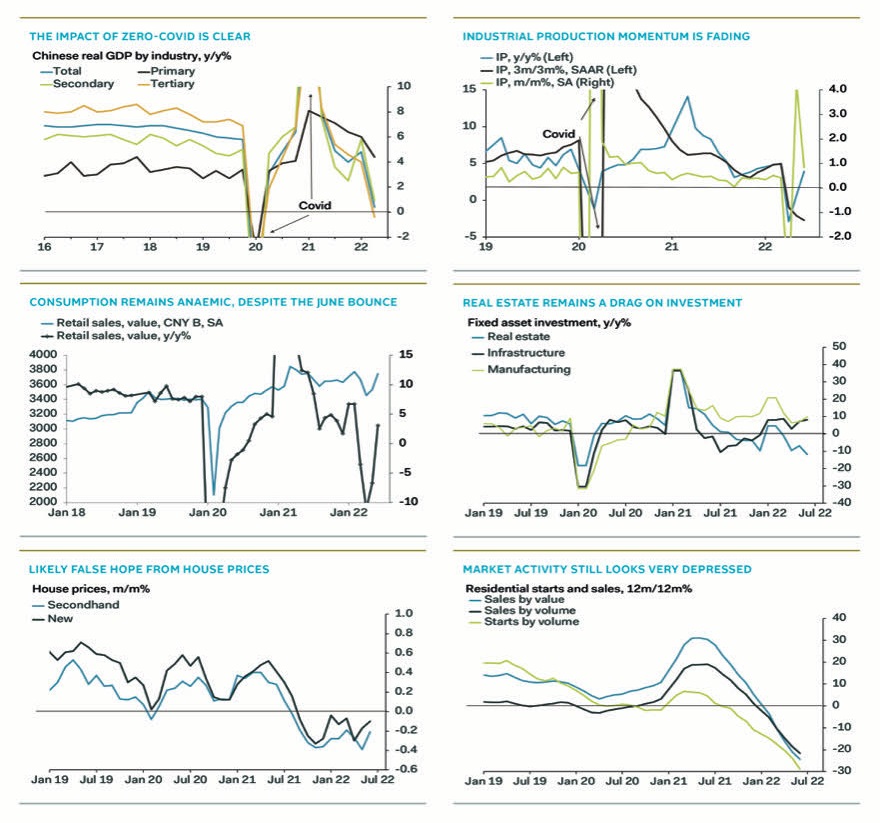

China: Real GDP grew 0.4% y/y in Q2, down sharply from 4.8% in Q1. Consensus was 1.2%.

Real GDP fell 2.6% q/q, after growing 1.3% in Q1. Consensus was -2.0%.

China: Industrial production rose 3.9% y/y in June, from 0.7% in May. Consensus was 4.0%.

China: Retail sales grew 3.1% y/y in June, after falling 6.7% in May. Consensus was 0.3%.

China: FAI growth was 6.1% ytd y/y in June, down from 6.2% in May. Consensus was 6.0%.

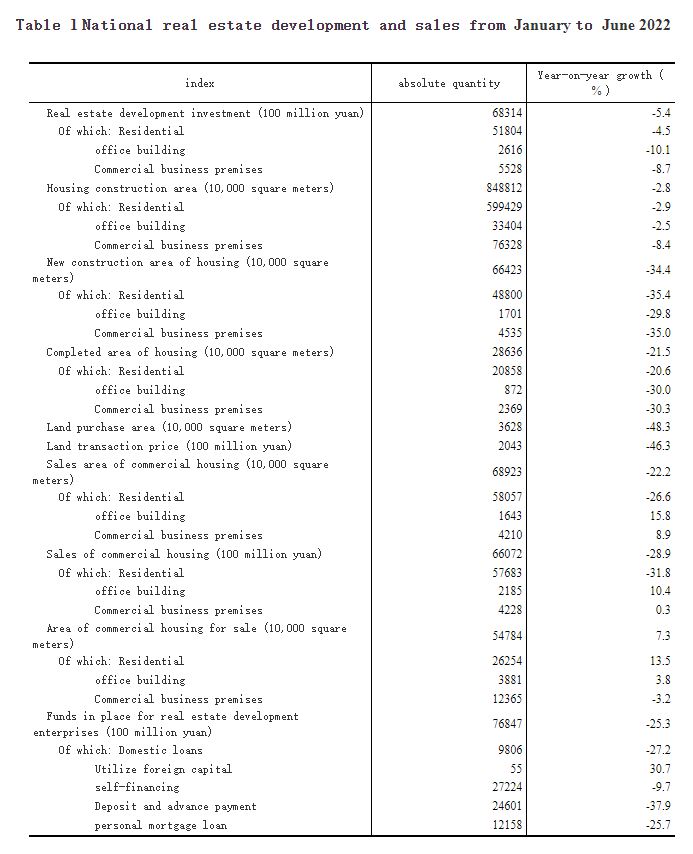

China: New home prices fell 0.10% m/m in June, after a 0.17% drop in May. Bloomberg reports no consensus

China: Residential property sales fell 31.8% ytd y/y in June, up from -34.5% in May. Bloomberg reports no consensus.

China: The PBoC left the 1-year MLF rate unchanged, at 2.85%, in line with consensus.

More of a slowdown for GDP than expected

Official real GDP narrowly avoided falling outright y/y in Q2, with strong headwinds from both the secondary and tertiary sectors. The latter – which includes real estate as well as other services – did fall into negative growth territory, at -0.4% y/y in Q1, from 4% in Q1, the weakest reading since the start of the pandemic. Secondary industry – largely a manufacturing measure – saw growth slow to 0.9% y/y, from 5.8% in Q1, again the weakest since Q1 2020. Growth was largely reliant on the primary sector, with a more modest slowdown to 4.4% y/y in Q2, from 6.0% in Q1, and “only” the weakest since Q3 2020, as high commodity prices provided some support to the extractive industries. The miss versus consensus largely reflects doubt over the willingness of China’s authorities to release bad economic data, rather than a conviction amongst economists that growth wasn’t so bad.

Zero-Covid is the key culprit for the quarterly weakness, shutting down a swathe of manufacturing for half the quarter, and scything down much of the service sector. The monthly data at least points to a rebound underway, which should see activity spring back in Q3. But the property drag is only getting worse, and without more aggressive policy support we think the Q3 rebound will prove short-lived. Covid cases are also edging higher once again, raising the risk of renewed lockdowns. Reaching the 5.5% growth target looks increasingly implausible.

A strong month for manufacturing, but momentum is fading

Industrial production saw improvement in all major components in June, but the recovery was led by manufacturing, which rose 3.4% y/y, from 0.1% in May. Mining grew 8.7% y/y from 7.0%, and utilities output increased 3.3% y/y, from 0.2%, both linked to rising energy consumption as the economy reopened more-or-less fully.

Preliminary volumes data suggest that the major manufacturing success story for June was motor vehicles, with output rising 26.5% y/y, after falling 5.2% in May, supported by heavy government subsidy. Other key manufacturing goods remained in negative growth territory, though with some improvement from May. Tellingly, volumes of steel saw a steeper drop in output for June than in May, while iron and caustic soda output also slowed, and cement production shrank, albeit at a more modest pace, despite the push on infrastructure investment. Property’s decline is proving difficult to offset.

While the headline y/y numbers look good, the monthly growth rate slowed significantly, after a strong rebound in May. IP grew 0.84% m/m, seasonally adjusted, down from 4.22% in May, suggesting the rebound energy is largely spent.

Subsidies pulled forward retail sales growth

Retail sales were much stronger than we had expected, supported by the tailwinds of society’s reopening and government support for specific sectors. Every subsector reported improved performance in June versus May, though not all returned to positive growth. The jump in the headline was unquestionably led by car sales, which rose 17.7% y/y in June, from -13.6% in May, supported by subsidies and tax cuts at the local and national levels. Consumer electronics also received some government support, helping sales to grow 9.8% y/y, from -3.9% in May. Catering services, however, continued to shrink, with sales falling 4.0% y/y, though this was much better than the 21.1% drop in May.

Momentum is yet to fade for retail sales. Headline growth was 6.0% m/m, up from 2.3% in May, seasonally adjusted. But June was the first fully “open” month for most of China, so we expect the reopening surge to fade noticeably in July, particularly with zero-Covid restrictions tightening once again. Subsidies should prop up some sectors for a while longer, but ultimately tend to pull forward sales from later periods, so towards year-end, at the latest, we would expect to see a notable slowdown in car and consumer electronics sales. That catering sales remain in negative y/y territory also suggests to us that “revenge spending” is fairly soft in China, compared to the experience in other economies post-Covid. Our third chart below shows that total sales remain below the pre-Omicron level.

Property continues to weigh on fixed asset investment

The slowdown in overall FAI came despite a high profile push from Beijing to boost infrastructure spending. The offsetting drag from real estate again proved hard to counter. Infrastructure FAI grew 7.1% ytd y/y in June, from 6.7% in May, while real estate FAI fell 5.4% ytd y/y, from -3.2% in May. Manufacturing also slowed slightly, growing 10.4% ytd y/y, from 10.6%.

The implied y/y growth numbers are slightly better for infrastructure and manufacturing, but much worse for property. We estimate that real estate FAI fell 11.8% y/y in June, after a 6.8% drop In May, while infrastructure rose 8.2% y/y, from 7.2%, and manufacturing investment surprisingly jumped to 9.9% y/y, from 7.1%, despite a challenging demand outlook. Supply side stimulus appears to be working in propping up manufacturing.

With more funds being poured into infrastructure, and supply side stimulus likely to be ramped up, this story should repeat in July, and indeed through Q3. Unfortunately, the drag from real estate seems set to grow, rather than moderate, given recent news of mortgage payment strikes, and spreading defaults amongst developers.

The reopening bounce for real estate proved underwhelming

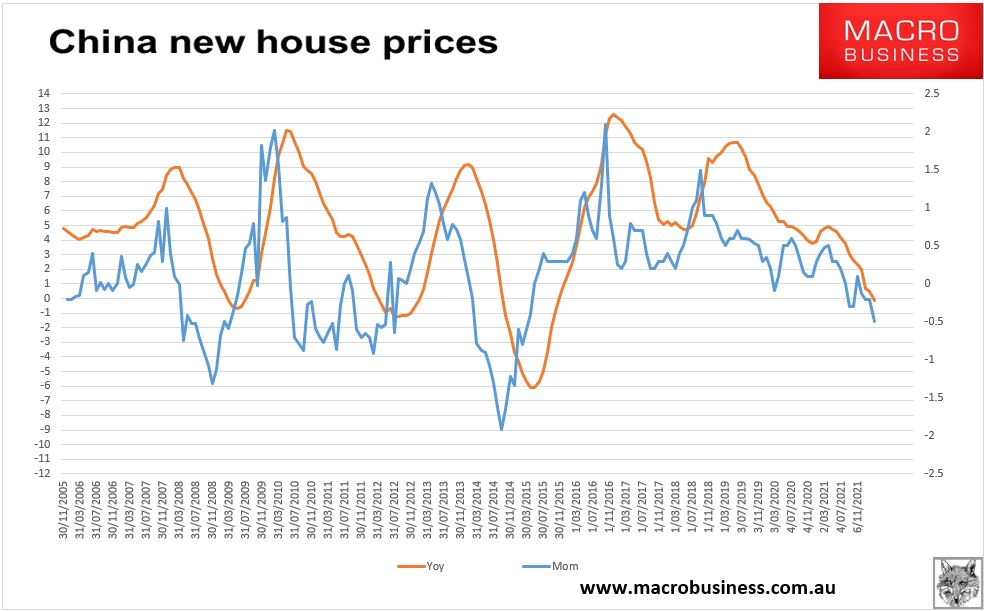

The pace of decline for house prices moderated slightly in June. New home prices fell 0.1% m/m, from -0.17% in May, while secondhand home prices fell 0.21% from -0.39%. Total sales also saw some improvement, falling 23.4% y/y after a 41.7% drop in May. But this is still terrible, and likely represents the unleashing of what little pent up demand formed during the lockdown period, alongside seasonal effects. The rolling 12 month growth rate for sales and starts continued to deteriorate in June, as shown in our final chart below. The immediate prospects look dim, given a mortgage payment strike, further offshore defaults by developers, the risk of an onshore default by Evergrande, and reports of tightening lending standards by some banks.

Sounds right to me. Let’s dig into the real estate data some more. The 70-city price data suggest ongoing stress with slightly improved price falls down 0.1% month-on-month and 0.5% year-on-year:

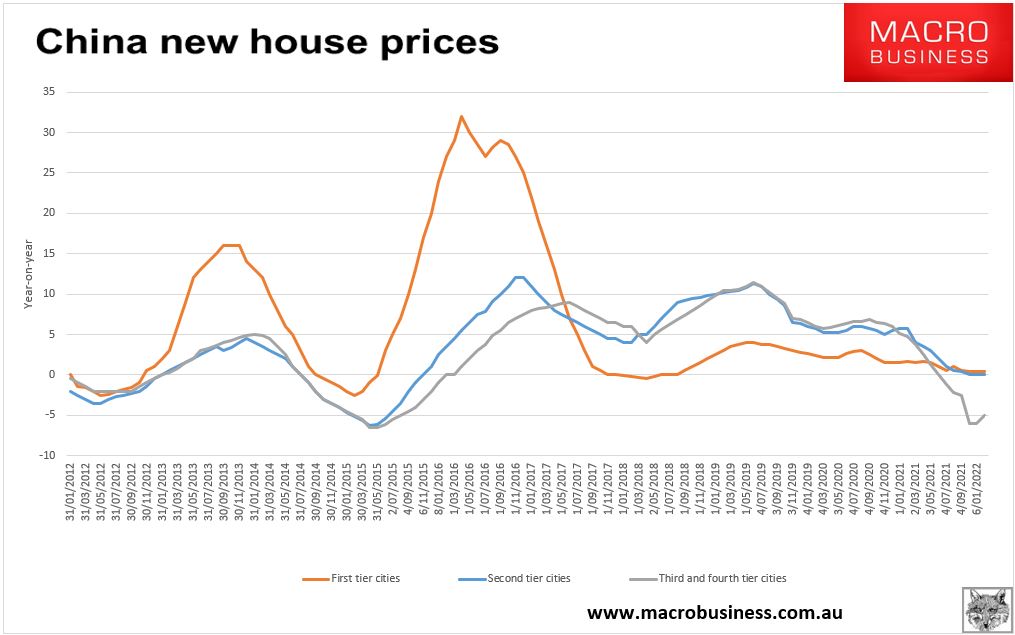

Prices are most troubled in the massively glutted lower-tier cities:

Advertisement

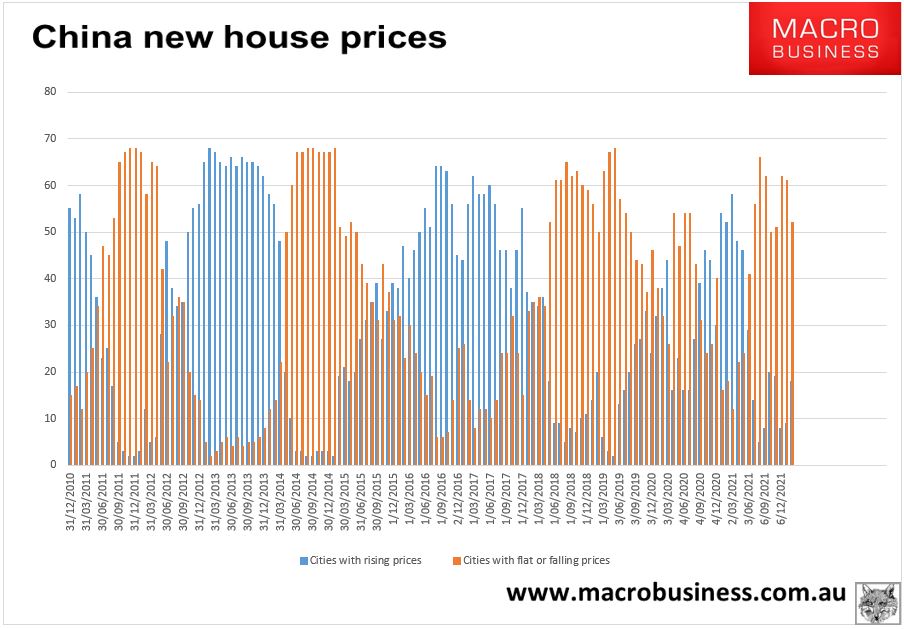

There was a slight improvement in breadth:

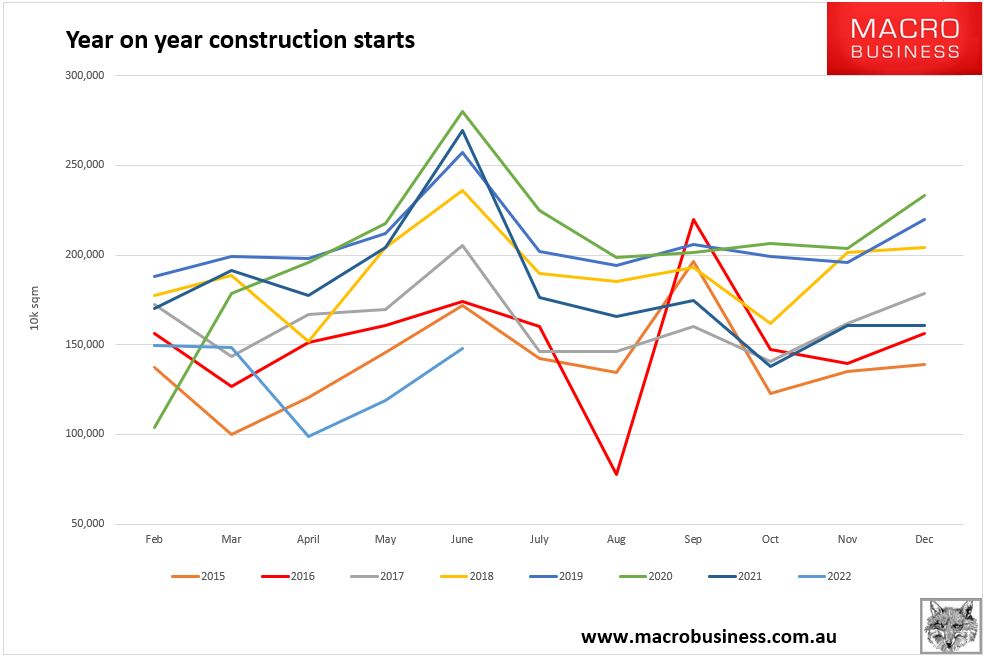

But this correction has been much more about volumes than price from the outset. June starts by floor were down a spectacular 45% year on year:

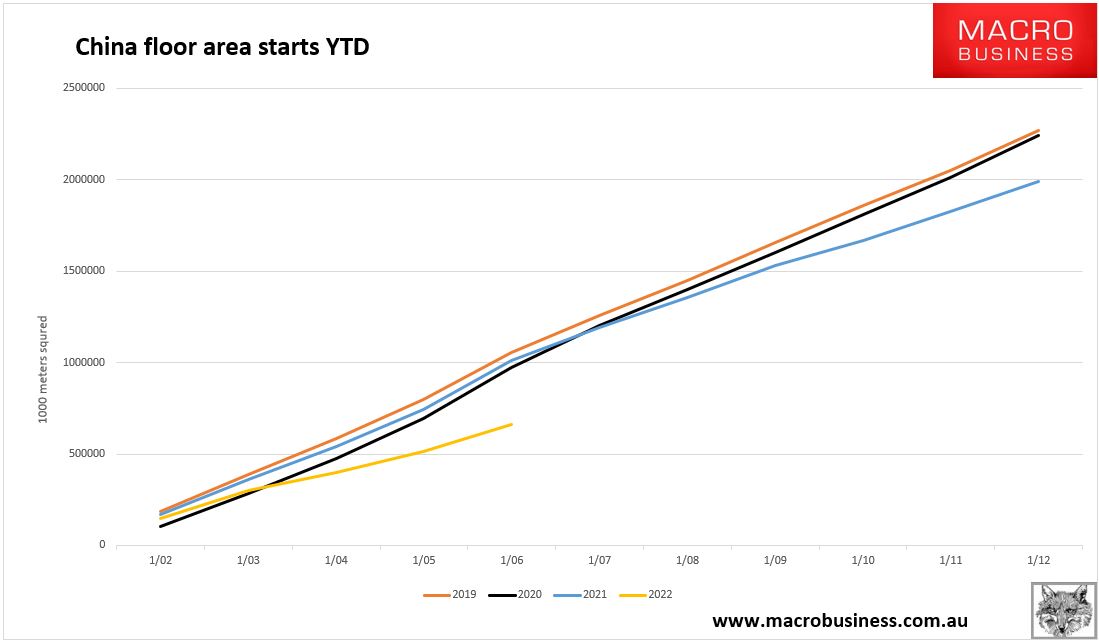

The year-to-date chart shows how calamitous is the trend:

I use rolling annual starts as a way of capturing the changes in demand for downstream commodity demand. It suggests that we are now roughly two-thirds of the way through the volume drop, assuming sales stabilise by year-end:

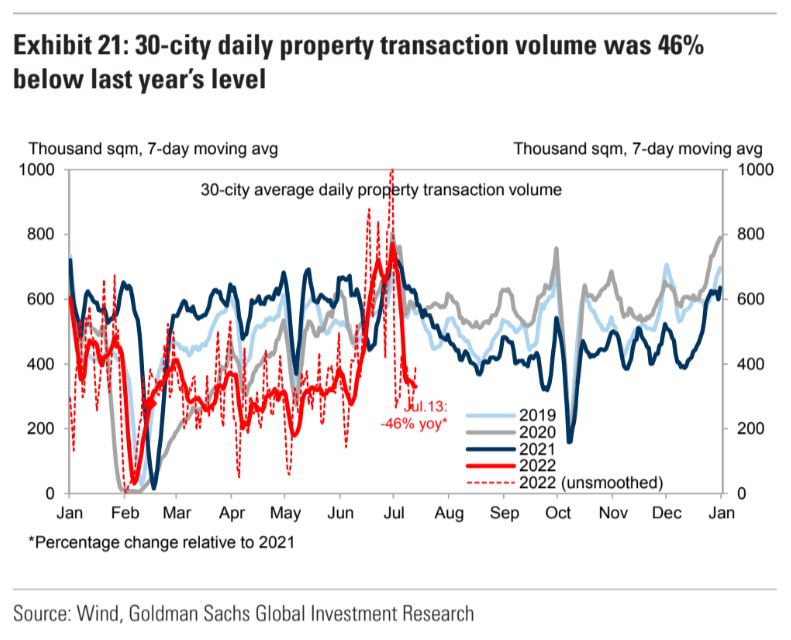

The latest sales cast doubt on that even happening. Sales were still down 46% last week:

China is censoring crowd-sourced documents tallying the number of mortgage boycotts spreading across the country, potentially hampering a key source of data for global investors and researchers tracking the property crisis.

Shared files managed on platforms including China’s Quora-equivalent Zhihu Inc. and on sites like Kdocs and Wolai have been banned following reports that the number of homebuyers refusing to pay mortgages surged in a span of days. GitHub, a popular file-sharing site for coders, remains as a source for people to post documents.

The file sharing has provided a key battleground for homeowners who are shunning mortgage payments for apartments that haven’t been built on time. The information also offered a gauge for global investors and banks from Nomura Holdings Inc. to Citigroup Inc. to measure the scale of the unfolding protests.

Lenders have said the bad housing loans are controllable. But the spike in incidents is fueling concerns that the property troubles — which have largely centered on developers following a government crackdown on excess leverage — will engulf big banks and China’s middle class, who have an estimated 70% of wealth stored in real estate.

“Manageable” in what sense? Reliant upon Big Brother’s attempted erasure of the strike? How will that fix the key problem of collapsed counterparty trust between buyers and developers? It will make it worse as nobody knows what’s going on.

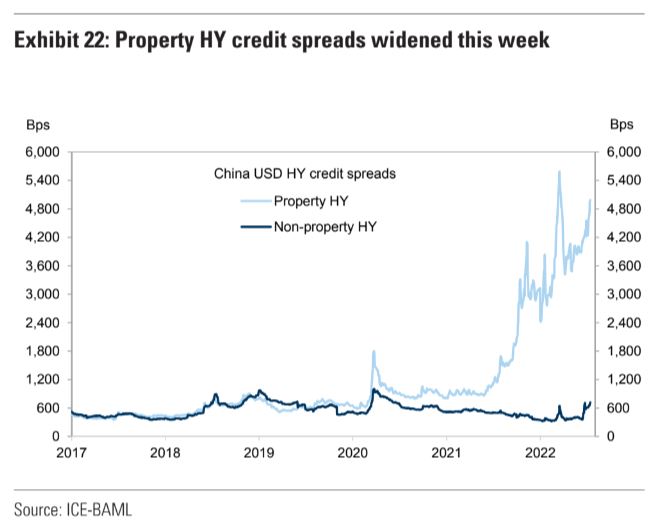

Developer funding markets are making this abundantly clear as spreads skyrocket:

Hence, land sales to developers remain disastrous, down by nearly half:

There is still the hope that infrastructure stimulus will help offset the construction downdraft:

But it must be remembered that this debt surge is only replacing lost land sales revenue. It is not stimulus at all:

And ahead there are still more lockdowns as well:

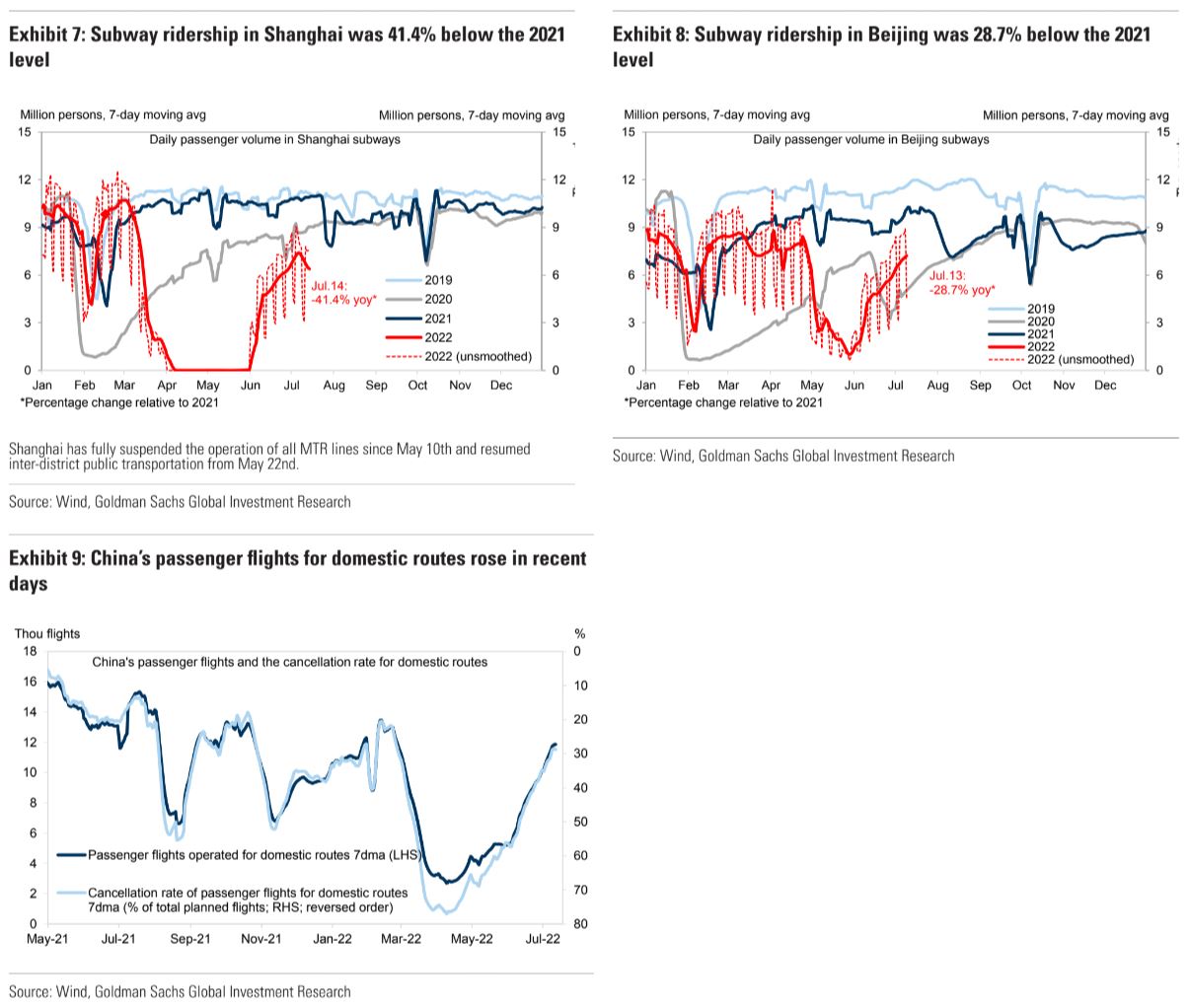

With the rebound in mobility already sputtering:

The Chinese economy remains in deep trouble. Very weak domestic demand is heading straight for an external trade shock from stalling US demand and inventory liquidation.

That will intensify capital outflow and may exacerbate the developing banking crisis leading to a classic EM currency shock.

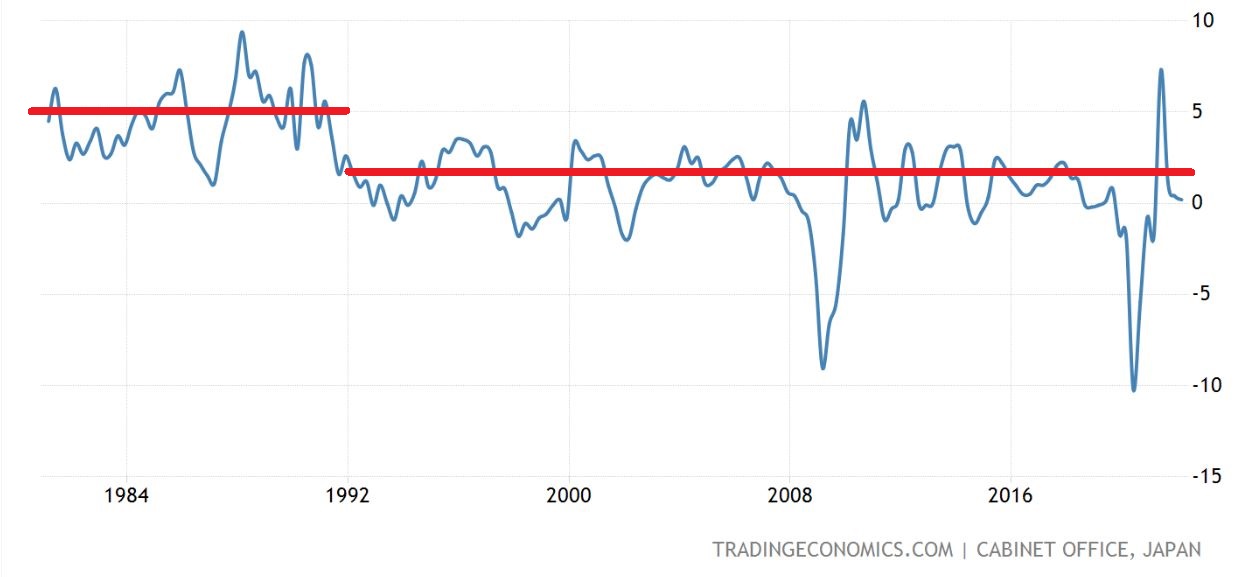

Placing this in the context of history, smarter Chinese commentary has long been concerned about its economy following the same path of Japan.

Before 1990, Japan enjoyed the demographic and property catch-up boom typical of emerging markets with average growth around 5%.

After 1990, these tailwinds reversed as demographics got blue-rinsed and the property market crashed. Endless growth stagnation and deflation followed as its economy transitioned ex-growth in a single mighty bust:

It looks like China is rerunning the script with remarkable accuracy. If the coming global recession transpires then it will reset Chinese growth lower as realty and banks are clogged with bad loans, partially offset by roads-to-nowhere, and a lower CNY driving the Asian merctantile model to ever greater extremes of deflation.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.