Morgan Stanley’s Michael Wilson with more excellent analysis

—

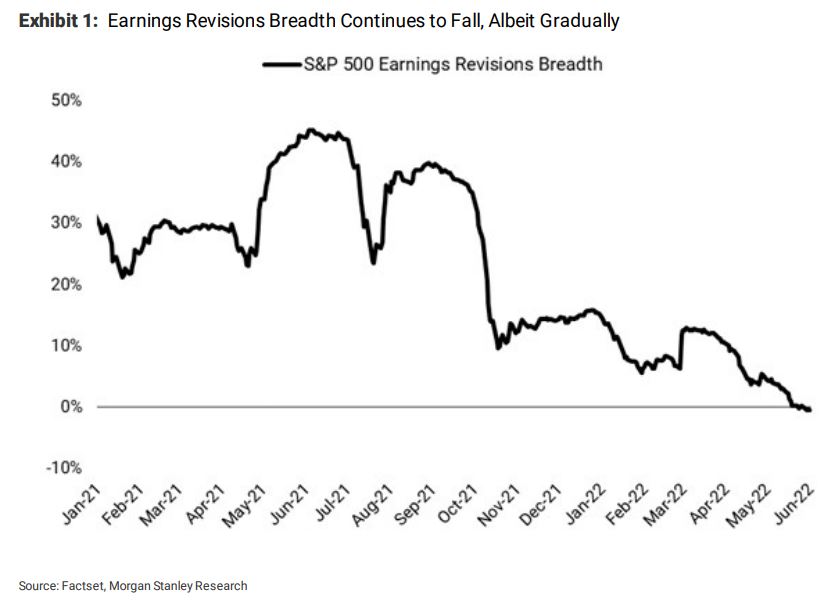

Over the past several months, we’ve been highlighting the declining trend in earnings revision breadth. We thought it would turn outright negative during Q1 earnings season and that’s where we are (Exhibit 1). However, it’s been a slow bleed toward 0%. This is why forward 12 month EPS estimates continue to grind higher for the S&P 500. That said, if we back out Energy and Materials, the NTM EPS forecasts are starting to consolidate (Exhibit 2and Exhibit 3). A key question for investors is whether they should pay a lower multiple for earnings growth derived to a notable extent from deeply cyclical sectors like Energy and Materials. We would argue the answer is ‘yes’, but with the equity risk premium back to 290bps, the market disagrees with that view or is clinging to the idea that earnings growth from the rest of the market will reaccelerate later this year. Time will tell, but we are still of the view that EPS forecasts will come down.