Shane Oliver of AMP Capital has rung the bell on mortgage stress, warning that people who have recently taken out a home loan face escalating repayments as interest rates soar:

“Those who took fixed rate last year may not feel the pinch yet, but still it’s going to be really painful for those who got in recently”.

“I think there’s a group of around 25 per cent to 30 per cent of borrowers who will see a substantial rise in mortgage repayments, particularly recent borrowers, and they’re probably more at risk. They’re probably facing mortgage stress in the next three to six months”.

“It will take a little bit longer to show up through forced selling, depending on how quickly the Reserve Bank raises interest rates, but some will be starting to worry about it.”

RateCity research director Sally Tindall likewise warned that Tuesday’s 0.5% rate hike was merely “a taste of what’s to come”:

“The RBA wants to get the inflation genie back in the bottle and it’s prepared to do what it takes to get the job done, and quickly,” she said.

“While many borrowers have been preparing themselves for rising rates, they may not have expected the RBA would go this hard and fast.

“If you don’t think you can keep up with hikes of this magnitude, take action now. Start making cuts to your budget and consider refinancing to a lower rate while you can”…

Analysis from RateCity.com.au shows that if the cash rate hits 2.10 per cent by the end of this year, someone with a $500,000 mortgage today could see their monthly repayments rise by $542 in total.

For someone with a $1 million mortgage, repayments could soar by a total of $1083.

Before Tuesday’s interest rate decision, the median economists’ forecast was for the official cash rate (OCR) to peak at around 2.5% mid next year.

The futures market is even more hawkish, tipping the RBA will lift the OCR to around 3.5% by May 2023.

Rate hikes of this magnitude would engineer the biggest proportional rise in mortgage repayments in Australia’s history, adding to household’s cost of living pain.

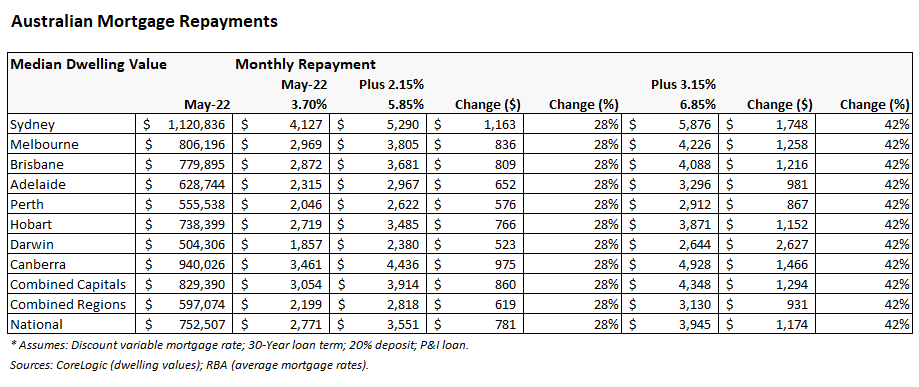

To illustrate why, consider the next table showing the average monthly repayment on the median priced dwelling across Australia, assuming a 30-year principal and interest variable rate mortgage and a 20 per cent deposit. The figures for May are before yesterday’s 0.5% OCR hike.

If the economists’ forecast comes true, and the OCR rises to 2.5%, then the average monthly mortgage repayment on the median priced Australian home would rise by $781, or 28%. Borrowers in Sydney would be most impacted, with monthly mortgage repayments on the median priced home jumping by $1,163.

If the futures market’s forecast comes true, and the OCR rises to 3.5%, then the average monthly mortgage repayment on the median priced Australian home would soar by $1,174 (42 %), with repayments across Sydney ballooning by $1,748 a month.

The impact would be even more severe for borrowers that took out a fixed rate mortgage during the height of the pandemic at rock bottom rates below 2.5%. These borrowers would face a doubling or tripling of mortgage rates when it comes to refinance in 2023 and 2024, depending on whether the economists’ or market’s OCR projection comes into play.

Given Australian house prices soared around 35% over the pandemic on the back of deep cuts to mortgage rates, heavy price falls would necessarily ensue from the sharpest lift in mortgage repayments in the nation’s history. Interest rates are a double-edged sword.

At the beginning of the Global Financial Crisis in 2008, the RBA mistakenly hiked the OCR by 1.0%. After the economy teetered and house prices began to fall, it was forced into a sharp reversal whereby the RBA slashed rates by 4.0% over just six months.

We see similar happening again after the RBA goes too hard on monetary tightening. Don’t be surprised to see the RBA once again cut rates aggressively in the second half of 2023 to counter deep falls in house prices and a recession.