One should never underestimate the power of CCP debt.

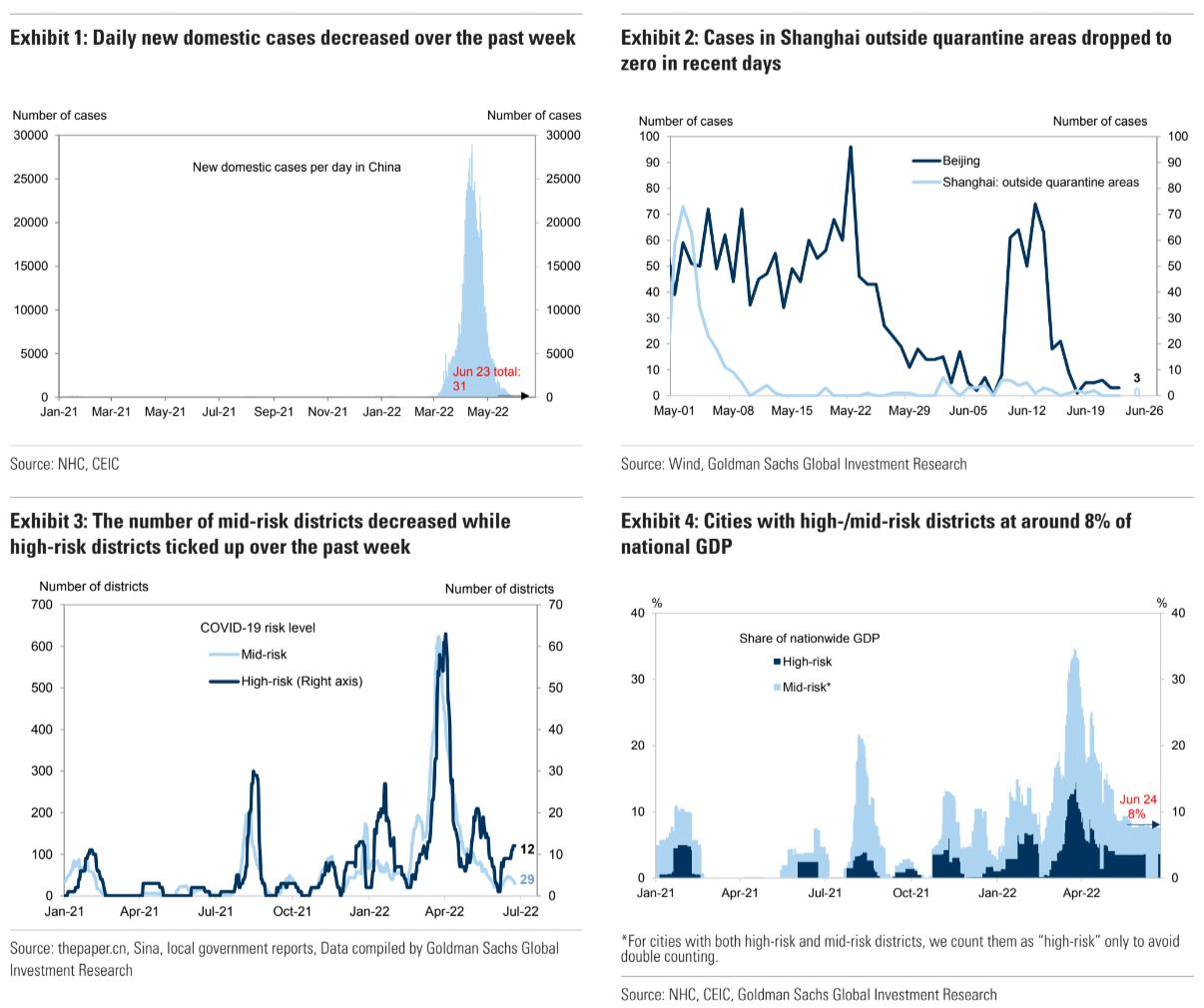

OMICRON is contained:

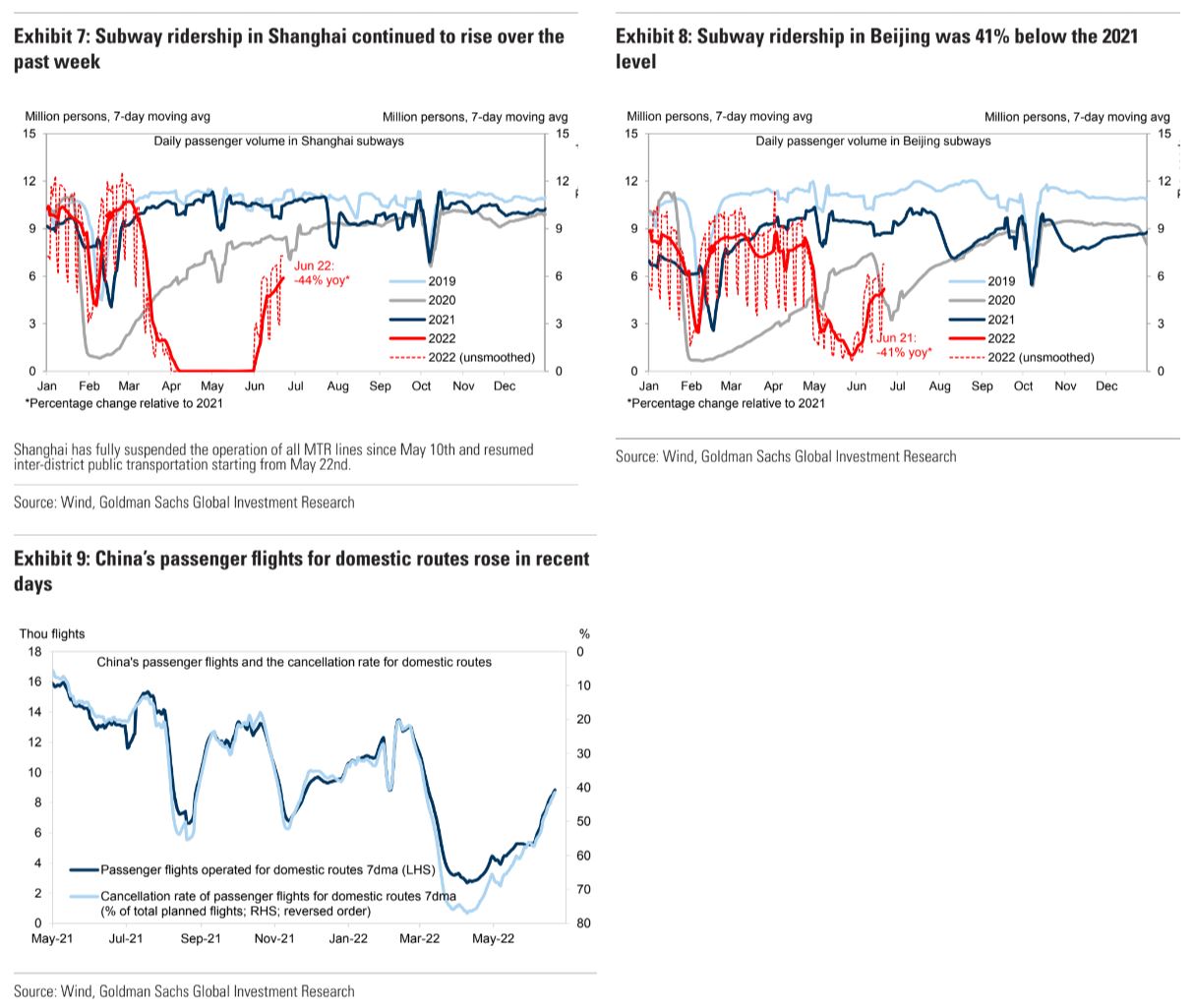

Mobility is lifting:

One should never underestimate the power of CCP debt.

OMICRON is contained:

Mobility is lifting:

The full text of this article is available to MacroBusiness subscribers