The always excellent Michael Wilson at Morgan Stanley leads us off:

Oil, Rates, Rebalancing Lead to a Rally

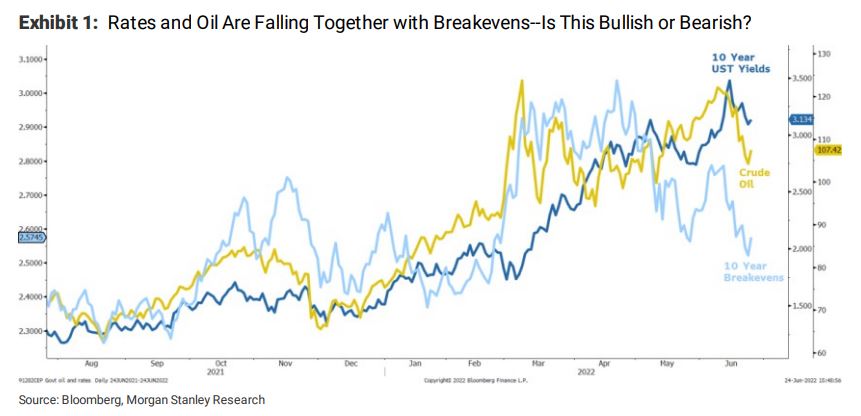

With talk of recession increasing sharply over the past few weeks and culminating with Fed Chair Powell’s 2-day Congressional testimony, markets decided enough bad news had been priced. We also think the sharp decline in both oil and interest rates (Exhibit 1) helped ease some of the concerns on inflation which still remains elevated and public enemy number one. In our view, both the fall in oil and rates are being driven more by the fears of an economic slowdown, or worse, rather than a real peak in inflation and, therefore, peak Fed hawkishness. However, with markets so oversold and bearishness so pervasive, equity investors have taken the bullish view and re-rated stocks higher via both the interest rate and Equity Risk Premium (ERP) channels.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.