Excellent stuff from The Market Ear today. The MB thesis is catching on.

—

| US 10 year update |

| So the 10 year reversed on the huge 3% level a few sessions ago, managed retracing around 50% of the move lower from highs and is now approaching the trend line that comes in at 3.10%. A close below 3.10% and things risk go very “dynamic”. Watch that trend line closely as well as the 50 day at 3%. |

Refinitiv Refinitiv | |

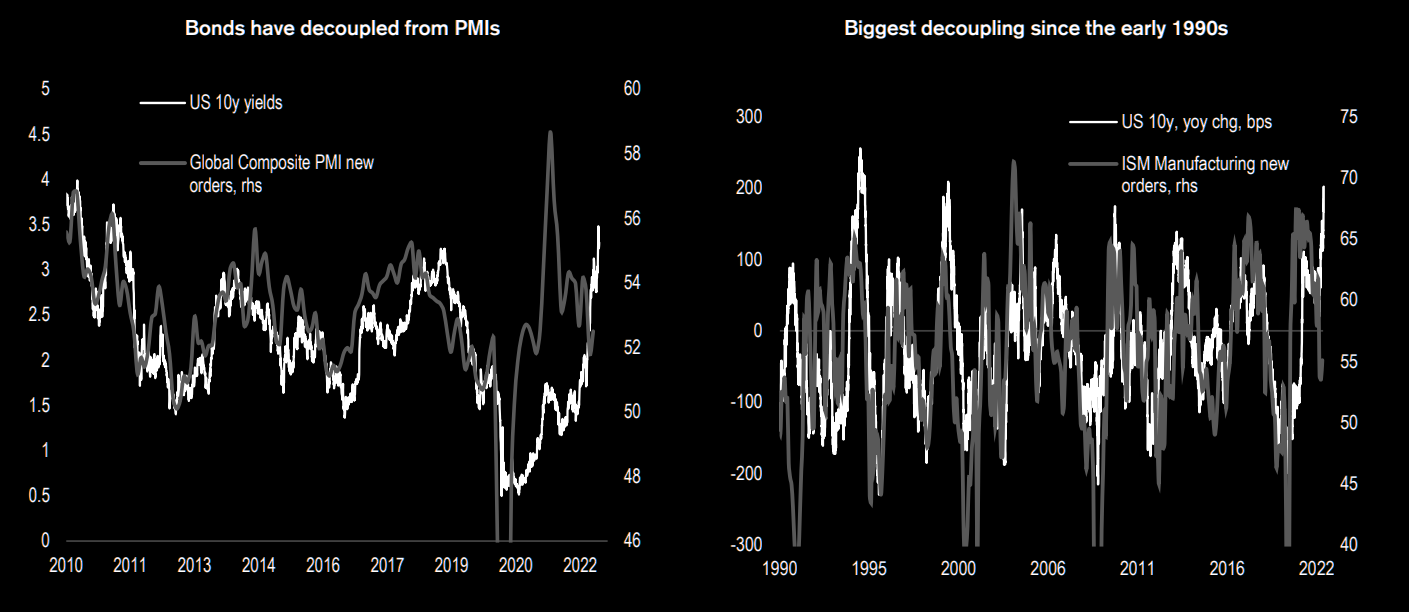

| Yields decoupling? |

| Are yields decoupling (permanently), or do we see some mean reversion take place from here? The gaps are rather wide… |

CS CS | |

| Recession cracks |

| TS Lombard says sell the latest rally in equities. Main bullets are: STIR markets have brought forward insurance cuts and increased their magnitude, while forward curves are sending a worrying signal | |