What other conclusion can we draw from Westpac’s latest survey? Expecting the consumer to keep spending on a run down in savings as sentiment collapses is ludicrous. 50bps next month and you can put a fork in households. They’re done.

—

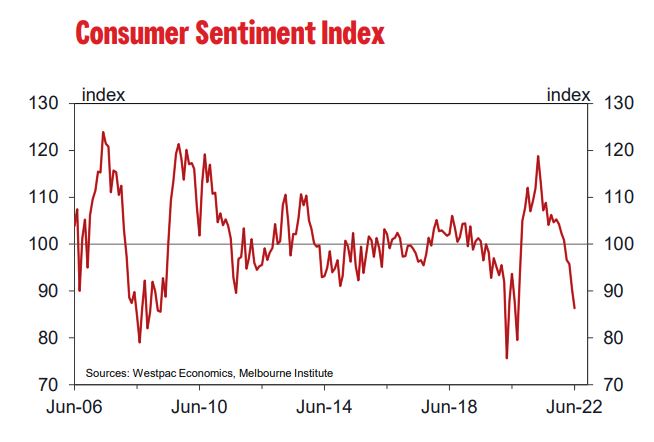

• Sentiment falls 4.5% to 86.4 in June, hit by inflation concerns and 50bp rate hike.

• Homebuyer sentiment nearing Global Financial Crisis lows.

• House Price Expectations cooling rapidly, especially in NSW and Victoria.

• Most consumers expect mortgage rates to rise more than 1% by June 2023.

• Labour market confidence holds at relatively strong levels.

The Westpac Melbourne Institute Consumer Sentiment fell 4.4% in June from 90.4 in May to 86.4 in June.

On June 7, the Reserve Bank announced a 50bp increase in the cash rate which was passed on in full by the banks.

This read is even weaker than we had expected.

Over the 46-year history of the survey, we have only seen Index reads at or below this level during major economic dislocations.

The record lows have been during COVID-19 (75.6); the Global Financial Crisis (79.0); early 1990s recession (64.6); the mid1980s slowdown (78.7) and the early 1980s recession (75.5).

Those last three episodes were associated with high inflation; rising interest rates; and a contracting economy – a mix that may be threatening to repeat.

The survey detail shows a clear picture of a slump in sentiment being driven by rising inflation; an associated lift in interest rates; and a loss of confidence around the economic outlook, both here and abroad.

Every three months we ask respondents about their news recall on specific topics. By far the highest recall in June was around news on inflation – nearly 60% of respondents noted news on this topic. This compares to 43% for ‘economic conditions’, 24% for ‘interest rates; and 23% for ‘international conditions’.

This is a particularly high level of recall for ‘inflation’ news – second only to a 62% read just prior to the Global Financial Crisis and compared to a long run average of just 12%. Not surprisingly, 84% of those recalling inflation news assessed it as unfavourable. This compares to 71% for ‘interest rate’ news; 85% for news on ‘international conditions’; and 78% for news on ‘economic conditions’.

There has been a steady increase in the proportion of consumers who expect significant increases in interest rates over the next 12 months. In June, 58% of respondents expected rates to increase by more than 1% over the next year. That compares with 50% in May, 36% in April and 30% in March. Notably, this share jumped to 65% amongst those surveyed following the RBA’s 50bp rate hike.

Inflation and interest rate concerns have taken a toll on the subindices that assess family finances and the near-term economic outlook.

The ‘finances compared to a year ago’ sub-index dropped 7% to 74.0 while the ‘finances, next 12 months’ sub-index fell 7.6% to 86.2.

The level of the ‘finances next 12 months’ sub-index is particularly noteworthy. Unlike other sub-indices this one is lower than during the 2008-09 Global Financial Crisis (GFC) – 18% below the average during that period. Enduring high inflation and rising interest rates appear to be a much more concerning prospect for finances than the credit market dislocations and global growth collapse seen during the GFC.

Around the economic outlook, moves were more mixed, the ‘economic outlook, next 12 months’ sub-index is down by 7.2% to 83.8 but the ‘economic outlook, next 5 years’ sub-index is holding up surprisingly well, edging 2.1% higher to 98.1.

Surging prices continue to take a heavy toll on spending intentions.

The ‘time to buy a major household item’ sub-index fell 3.3% to 89.5 – weaker reads have only ever been seen during the onset of the COVID pandemic, the GFC and the early 1990s recession.

Despite this collapse in consumer sentiment, Westpac is still constructive on the near-term outlook for consumer spending.

The main drivers are a continued post-COVID reopening and the freeing-up of savings, with important support coming from strong labour markets.

High confidence in the labour market is still very clear in our June survey. The Westpac-Melbourne Institute Unemployment Expectations Index remains at very low levels, falling marginally from 109.6 in May to 108.5 in June (a decline means more respondents expect the unemployment rate to fall – an improved outlook). The Index is still 16% below its long run average of 130.

The same cannot be said for confidence around housing which has seen a further significant deterioration.

The ‘time to buy a dwelling’ index fell 3.1% from 77.5 in May to 75.1 in June – a new post-GFC low. The index reflects deteriorating affordability which had been due to rising prices but is now being affected by actual and expected rises in interest rates.

A deep chasm has opened between males and females on this

topic, with index reads of 85.8 (up 1.1%) for males and 64.7 (down 8.6%) for females. This disharmony does not bode well given that house purchases are usually the most important single spending decision for many families.

House price expectations continue to cool rapidly. The Westpac Melbourne Institute Index of House Price Expectations fell by 8.4% from 121.4 to 111.1. The Index is still above 100, indicating that more respondents expect prices to rise than fall. However, the picture across states varies. In NSW the Index fell by 11.2% to 103.8 while in Victoria it fell by 9.9% to 101.50. It looks likely that pessimists will soon hold sway in both states. In contrast, optimism still abounds in Queensland where the state index rose 3.1% 124.5.

The wedge between males and females is also apparent on house price expectations, if not quite as severe (115.2 vs 107.2). Consumer risk aversion has also intensified. Our June survey included updates on our ‘wisest place for savings’ questions which is run every three months. Safe or defensive options are now heavily favoured with a further rise in the proportion of

consumers nominating ‘bank deposits’, and ‘pay down debt’.

Indeed, just over 64% of consumers nominated debt repayment or capital protected options, up from 59% in March and near the extreme high of 65.5% seen during the GFC. Conversely, very few consumers favour riskier options, only 8% nominating ‘real estate’ and 8% nominating shares.

The Reserve Bank Board next meets on July 5. The best policy in a tightening cycle is to move quickly in the early stages of the cycle when interest rates are clearly below neutral and the risk of over-tightening is moderate. It is also important to signal, as early as possible, to economic agents that the Bank is committed to containing inflation.

We saw a 50bp move in June from 0.35% to 0.85% and we expect another 50bp move in July. That would see not only the emergency cuts in 2020 being withdrawn but also most of the 75bp of cuts made in 2019, when the Board became frustrated with its inability to lift inflation back to within the 2-3% target band.

As we have seen with today’s survey, high inflation has become the major challenge for the Australian economy. The RBA needs to normalise policy quickly to begin to address this very disturbing challenge. Another 50bps in July will be a further decisive step in this process.